Reebok 2010 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2010 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

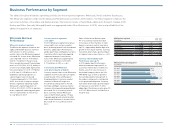

148 Group Management Report – Financial Review Group Business Performance Treasury

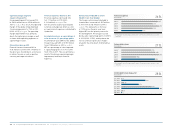

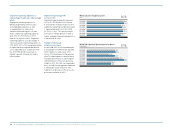

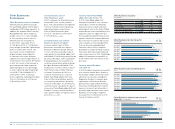

Net borrowings

€ in millions

1) Including Reebok, Rockport and Reebok-CCM Hockey from February 1, 2006

onwards.

Interest rate development 1 )

in %

1) Weighted average interest rate of gross borrowings.

47

49

2006 1 )

2007

2008

2009

2010

2006

2007

2008

2009

2010

2,231

1,766

2,189

917

221

4.8

5.3

5.2

5.2

5.1

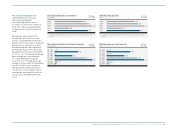

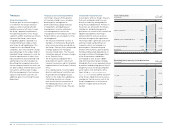

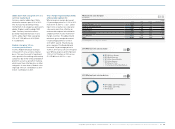

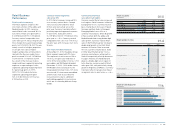

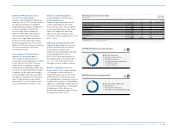

Net borrowings by quarter 1 )

€ in millions

1) At end of period.

48

Q1 2009

Q1 2010

Q2 2009

Q2 2010

Q3 2009

Q3 2010

Q4 2009

Q4 2010

2,883

1,359

2,732

1,090

2,294

903

917

221

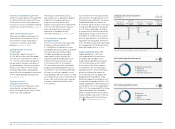

Stable debt maturity profile

Over the course of 2010, the Group’s

financing maturity profile remained

stable with the term structure of debt

evenly spread see 53. At the end of

2010, total refinancing needs in the next

12 months amounted to € 273 million

(2009: € 198 million).

Interest rate slightly improved

The weighted average interest rate on

the Group’s gross borrowings improved

slightly to 5.1% in 2010 (2009: 5.2%)

see 49. Positive effects from lower

interest rates on short-term borrowings

were partly offset by the higher share of

longer-term borrowings in the Group’s

financing mix, which carry a higher

average interest rate. Long-term fixed-

rate financing amounted to 76% of the

Group’s total financing at the end of 2010

(2009: 68%). Variable financing amounted

to 24% of total financing at the end of the

year (2009: 32%).

Net debt position decreases

by € 696 million

Net borrowings at December 31, 2010

amounted to € 221 million, which

represents a decrease of € 696 million,

or 76%, versus € 917 million in the

prior year see 47. This development

was fully in line with our original target

of net debt to be below the prior year

level communicated at the beginning

of 2010. Strong operating cash flow

and lower capital expenditure than

originally planned positively influenced

this development. Currency effects had

a positive impact of € 43 million on net

borrowings development. On a net debt

basis, the utilisation of credit facilities

available to the Group at the end of 2010

was 4% versus 16% in the prior year.

The Group’s financial leverage declined

to 4.8% at the end of 2010 versus 24.3%

in the prior year see 51. At the end

of 2010, the ratio of net borrowings

over EBITDA was 0.2 (ratio in 2009:

1.2) and thus well within the Group’s

medium-term guideline of less than

two times. Efficient management of our

capital structure continues to be a top

management priority see Subsequent

Events and Outlook, p. 174.