Reebok 2010 Annual Report Download - page 173

Download and view the complete annual report

Please find page 173 of the 2010 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

Group Management Report – Financial Review Risk and Opportunity Report 169

Nevertheless, our net US dollar cash flow

exposure after natural hedges calculated

for 2011 was roughly € 3.3 billion at

year-end 2010, which we hedged using

forward contracts, currency options and

currency swaps see 05. Our Group’s

Treasury Policy allows us to utilise

hedging instruments, such as currency

options or option combinations, which

provide protection while – at the same

time – retaining the potential to benefit

from future favourable exchange rate

developments in the financial markets.

As 2011 hedging has almost been

completed, it is clear that conversion

rates on major currencies will be slightly

less favourable compared to those of

2010. Volume forecast variances, greater

currency volatility and an increasing

portion of our business in emerging

markets will expose the adidas Group

to additional currency risks in 2011.

Furthermore, translation impacts from

the conversion of non-euro-denominated

results into our Group’s functional

currency, the euro, might lead to a

material negative impact on our Group’s

financial performance. As a consequence,

the assessment of currency risks has

increased. We now believe the likelihood

of currency risks is highly probable and

we regard the possible financial impact of

currency risks as major.

Interest rate risks

Changes in global market interest rates

affect future interest payments for

variable-interest liabilities. As a result,

significant interest rate increases can

have an adverse effect on the Group’s

profitability, liquidity and financial

position.

In line with IFRS 7 requirements, we

have analysed the impact of changes

in the Group’s most important interest

rates on net income and shareholders’

equity. The effect of interest rate changes

on future cash flows is excluded from

this analysis. Nevertheless, accrued

interest, which is recognised as a liability,

has been re-calculated based on the

hypothetical market interest rates as

at December 31, 2010. Fair values for

derivative interest rate instruments

accounted for as cash flow hedges

were then re-evaluated based on the

hypothetical market interest rates with

the resulting effects on net income and

equity included in the sensitivity analysis.

The fair value interest rate risk from

private placements that are hedged with

fair value hedges was also taken into

consideration.

However, the effect on the income

statement from changes in the fair values

of hedged items and hedging instruments

attributable to interest rate changes

was not material. Exclusions from this

analysis are as follows:

− Some fixed-rate financial instruments,

such as certificates of deposit, which

our Group values at “fair value through

profit or loss” due to the short-term

maturity of these instruments. Potential

effects due to changes in interest rates

are considered immaterial and are not

recognised in the sensitivity analysis.

− Other fixed-rate financial instruments

are measured at amortised cost. Since

a change in interest rates would not

change the carrying amount of this

category of instruments, there is no net

income impact and they are excluded

from this analysis.

The interest rate sensitivity analysis

assumes a parallel shift of the interest

yield curve for all currencies and

was performed on the same basis for

both 2009 and 2010. A 100 basis point

increase in interest rates at December

31, 2010 would have increased share-

holders’ equity by € 0.04 million (2009:

€ 0.50 million) and decreased net income

by € 0.22 million (2009: € 0.65 million). A

100 basis point decrease of the interest

rates at December 31, 2010 would have

resulted in a € 0.04 million decrease in

shareholders’ equity (2009: € 0.05 million)

and a € 0.22 million increase in net

income (2009: € 0.63 million).

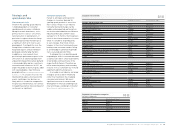

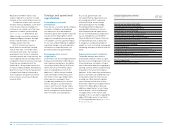

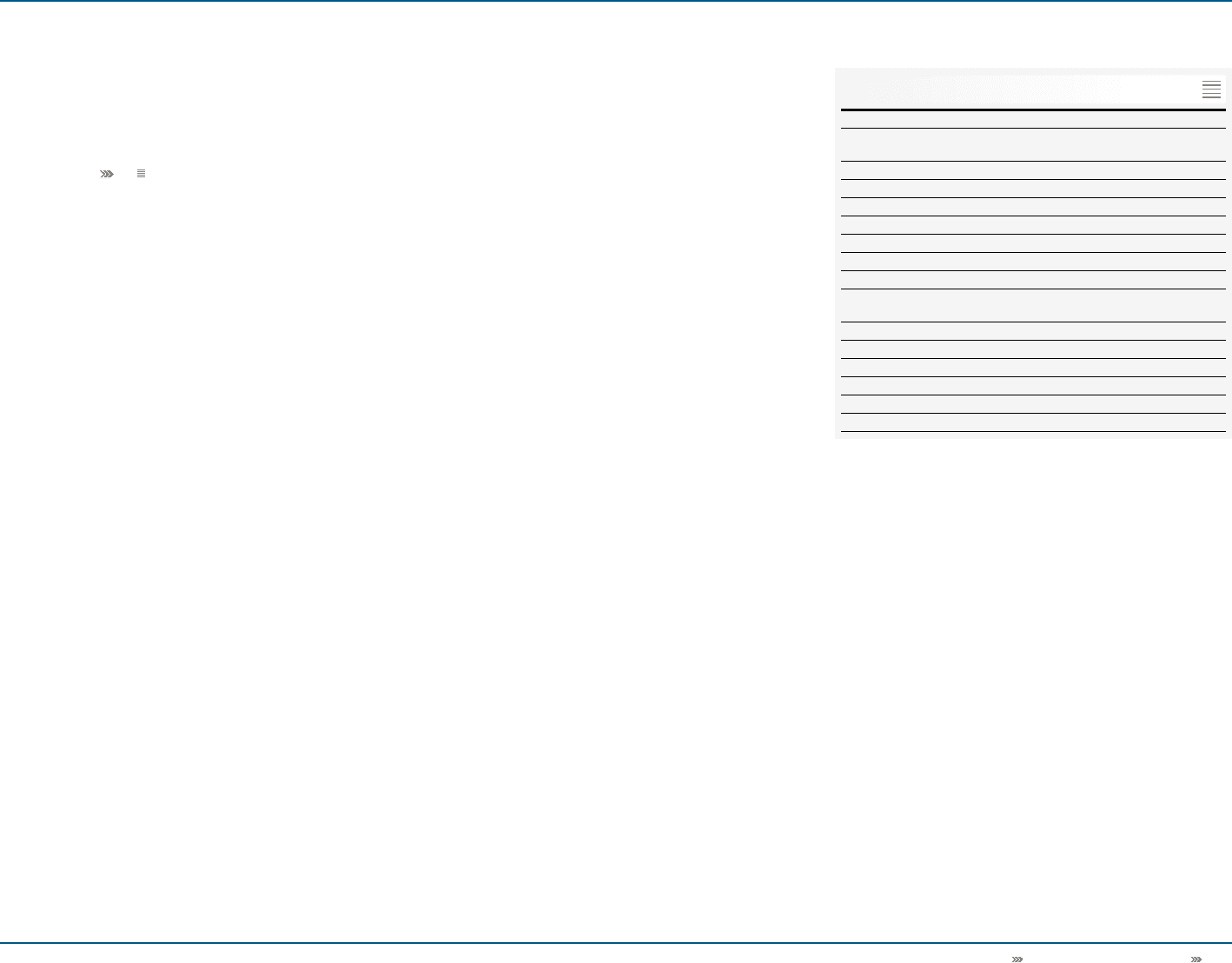

Sensitivity analysis of foreign exchange rate changes

€ in millions

USD RUB GBP JPY

As at December 31,

2010

EUR +10% USD +10% EUR +10% EUR +10%

Equity (157) — 21 20

Net income 3 (1) 1 (3)

EUR –10% USD –10% EUR –10% EUR –10%

Equity 193 — (25) (24)

Net income (4) 1 (1) 4

As at December 31,

2009

EUR +10% USD +10% EUR +10% USD +10%

Equity (144) — 21 13

Net income 1 0 (1) 0

EUR –10% USD –10% EUR –10% USD –10%

Equity 176 — (25) (13)

Net income (1) 0 1 (1)

06