Reebok 2010 Annual Report Download - page 182

Download and view the complete annual report

Please find page 182 of the 2010 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

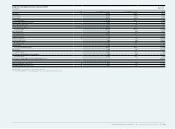

178 Group Management Report – Financial Review Subsequent Events and Outlook

Group other operating expenses to

decrease as a percentage of sales

In 2011, the Group’s other operating

expenses as a percentage of sales are

expected to decrease modestly (2010:

42.1%). Sales and marketing working

budget expenses as a percentage of

sales are projected to decline modestly

compared to the prior year. Marketing

investments to support Reebok’s growth

strategy in the men’s and women’s

fitness category, as well as investments

to support growth in our key attack

markets North America, Greater China

and Russia/CIS will be offset by the

non-recurrence of expenses in relation to

adidas’ presence at the 2010 FIFA World

Cup. Operating overhead expenditures

as a percentage of sales are forecasted

to decline slightly in 2011. Higher

administrative and personnel expenses

in the Retail segment due to the planned

expansion of the Group’s store base will

be offset by leverage and efficiency gains

in the Group’s non-allocated central

costs.

We expect the number of employees

within the adidas Group to increase

versus the prior year level. Additional

hires will be mainly related to own-retail

expansion. The majority of new hires will

be employed on a part-time basis and

will be located in emerging markets.

The adidas Group will continue to spend

around 1% of Group sales on research

and development in 2011. Areas of

particular focus include customisation

and digital sports products at adidas,

as well as supporting the expansion of

Reebok’s fitness and training positioning

see Research and Development, p. 110.

Operating margin to continue to expand

In 2011, we expect the operating margin

for the adidas Group to increase to a level

between 7.5% and 8.0% (2010: 7.5%).

Lower other operating expenses as a

percentage of sales are expected to be

the primary driver of the improvement.

Earnings per share to increase to a

level between € 2.98 and € 3.12

Earnings per share are expected to

increase at a rate of 10% to 15% to a level

between € 2.98 and € 3.12 (2010 diluted

earnings per share: € 2.71). Top-line

improvement and an increased operating

margin will be the primary drivers of

this positive development. In addition,

we expect lower interest rate expenses

in 2011 as a result of a lower average

level of net borrowings. The Group tax

rate is expected to be at a similar level

compared to the prior year level (2010:

29.5%).

Operating working capital as a

percentage of sales to increase

In 2011, average operating working

capital as a percentage of sales is

expected to increase compared to the

prior year level (2010: 20.8%). This is

mainly due to working capital increases

to support the growth of our business.

Investment level to be between

€ 350 million and € 400 million

In 2011, investments in tangible and

intangible assets are expected to amount

to € 350 million to € 400 million (2010:

€ 269 million). Investments will focus

on adidas and Reebok controlled space

initiatives, in particular in emerging

markets. These investments will account

for almost one-third of total investments

in 2011. Other areas of investment

include the further development of

the adidas Group Headquarters in

Herzogenaurach, Germany, and the

increased deployment of SAP and other

IT systems in major subsidiaries within

the Group. All investments within the

adidas Group in 2011 are expected to be

fully financed through cash generated

from operations.

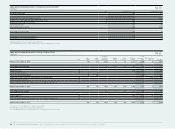

Excess cash to be used to support

growth initiatives

In 2011, we expect continued positive

cash flows from operating activities. Cash

will be used to finance working capital

needs, investment activities, as well as

dividend payments. We intend to largely

use excess cash to invest in our Route

2015 growth initiatives and to further

reduce net borrowings. Over the long

term, we aim to maintain a ratio of net

borrowings over EBITDA of less than two

times as measured at year-end (2010

ratio: 0.2).

Efficient liquidity management in

place for 2011 and beyond

Efficient liquidity management continues

to be a priority for the adidas Group

in 2011. We focus on continuously

anticipating the cash inflows from

the operating activities of our Group

segments, as this represents the main

source of liquidity within the Group. On

a quarterly basis, liquidity is forecasted

on a multi-year financial and liquidity

plan. Long-term liquidity is ensured

by continued positive free cash flows

and sufficient unused committed and

uncommitted credit facilities. In 2011, we

do not expect any financing activities in

order to replace maturing credit facilities

see Treasury, p. 146.

Management to propose

dividend of € 0.80

In light of the strong cash flow generation

in 2010 and the significantly reduced

level of net borrowings, Management

will recommend paying a dividend of

€ 0.80 to shareholders at the Annual

General Meeting (AGM) on May 12,

2011, representing an increase of 129%

compared to 2009 (2009: € 0.35). Subject

to shareholder approval, the dividend will

be paid on May 13, 2011. The proposal

represents a payout ratio of 30% of net

income as in the prior year and complies

with our dividend policy, according to

which we intend to pay out between 20%

and 40% of net income attributable to

shareholders annually. Based on the

number of shares outstanding at the end

of 2010, the dividend payout will increase

to € 167 million compared to € 73 million

in the prior year.