Reebok 2010 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2010 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

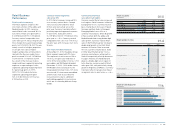

Group Management Report – Financial Review Risk and Opportunity Report 163

The Group reduces this risk by only

entering into lease contracts with

durations of less than ten years.

Store performance is measured by

a retail scorecard consisting of nine

quantitative key performance indicators.

Underperforming stores are reorganised,

remodelled or closed as appropriate.

Our increased focus on improving our

sophistication as a retailer by investing

in management expertise as well as in IT

systems remains a key priority for 2011

see Global Sales Strategy, p. 82. Despite

the projected improvement in the global

macroeconomic environment in 2011,

risks to consumer spending due to rising

inflation are high see Economic and Sector

Development, p. 130. Therefore, we view the

risk of underperformance of some of our

own-retail stores as likely. The potential

financial impact from own-retail under-

performance, which may also involve

impairment charges and store closures,

is moderate.

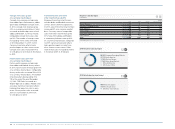

Risks from rising input costs

Raw material and labour costs account

for approximately 70% of the Group’s

cost of sales. Prices of materials such

as rubber, cotton, polyester and those

which closely correlate with the oil price

are especially subject to the risk of

price changes. As our ordering process

and price negotiations usually take

place around six months in advance of

production, our sourcing function has

visibility and reaction time to plan for

sharp increases in input costs.

To reduce the financial impact on our

product margins from higher sourcing

costs, we are implementing further lean

manufacturing techniques at our partner

factories, reducing time and cost in the

procurement process, re-engineering

our products and selectively increasing

prices where possible. In addition, within

our end-to-end profitability initiatives,

we have implemented a dedicated team

which is responsible for elaborating

mitigation measures against rising input

costs throughout the supply chain see

Global Operations, p. 106. In the medium

term, we also have the ability to adapt

our sourcing structure to take advantage

of more competitive pricing in other

locations.

As a result of the considerable

turnaround in global economic activity,

raw material prices have increased

significantly compared to the prior

year. This development is forecasted to

negatively impact our sourcing costs in

2011. As we begin planning for 2012,

further increases cannot be ruled out.

Therefore, the risks from rising input

costs have increased significantly

compared to the end of 2009 and are now

assessed as having a highly probable

likelihood of occurrence and a major

potential financial impact.

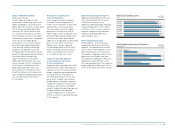

Supplier default risks

Over 95% of our product offering is

sourced through independent suppliers,

mainly located in Asia see Global

Operations, p. 106. To reduce the risk

of business interruptions following a

potential supplier default, we work with

vendors who demonstrate reliability,

quality, innovation and continuous

improvement.

In addition, we have bought insurance

coverage for the risk of business inter-

ruptions caused by physical damage to

supplier premises.

Therefore, we assess supplier default

risks as having a possible likelihood of

occurrence and a moderate potential

financial impact.

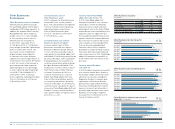

Inventory risks

As we place initial production orders

around six months in advance of

delivery, the adidas Group is exposed to

inventory risks relating to misjudging

consumer demand at the time of

production planning. A sudden decline

in demand has the potential to cause

excess inventories. This can have

negative implications for our financial

performance, including higher levels

of clearance activity and inventory

obsolescence as well as reduced liquidity

due to higher operating working capital

requirements.

On the other hand, a sudden increase

in demand can lead to product short-

falls at the point of sale. In this situation,

our Group faces the risk of missed

sales opportunities and/or customer

and consumer disappointment, which

could lead to a reduction in brand loyalty

and our reputation as an on-time, in-full

supplier. In addition, the Group faces

potential profitability impacts from costs

such as air freight in efforts to speed up

replenishment.

In order to mitigate these risks, we

continuously strive to improve our fore-

casting and material planning processes.

Our replenishment programmes are

another example of how we are striving

to shorten production lead times,

ensuring availability of products while

avoiding excess inventories see Global

Operations, p. 106.

Although the expected over-

proportionate growth of the Retail

segment will increase the exposure

towards swings in consumer demand,

our demand and inventory planning

accuracy for 2011 will benefit from the

improved macroeconomic climate versus

2010. Therefore, the associated inventory

risks have decreased slightly and are now

assessed as having a possible likelihood

of occurrence and a moderate potential

financial impact on our Group.

Customer risks

Customer risks arise from our depend-

ence on key customers who have the

ability to exert bargaining power and can

therefore cause considerable margin

pressure or cancel orders. These risks

exist not only due to the relative size

of some of our major customers, but

also as a result of our limited ability to

influence how they conduct business. In

addition, over recent years, several large

customers have been expanding their

own private brand and private label busi-

nesses, which can negatively impact our

efforts to increase shelf space.