Rogers 2005 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2005 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

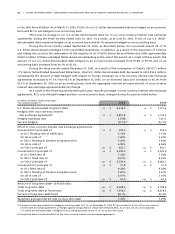

57 ROGERS 2005 ANNUAL REPORT . MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

in 2003, 1.1% in 2004, 1.03% in 2005 and 1.03% (interim rate) for 2006. Refer to the section below entitled “Risks and

Uncertainties – Contribution Rate Increases Could Adversely Affect Wireless’ Results of Operations” for further informa-

tion on the CRTC contribution levy.

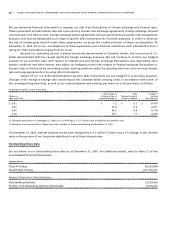

NE W SP E CT R UM F EE RE G IM E

Late in 2002, Industry Canada released a consultation paper proposing a new methodology for calculating spectrum fee

assessments (excluding auction spectrum). Prior to April 1, 2004, spectrum fees were assessed on a per radio channel basis

in the case of 850 MHz spectrum, and a per site basis for 1900 MHz spectrum. In a decision released by Industry Canada

in December 2003, effective April 1, 2004, the new regime implemented an annual cost per MHz per population for

both frequency ranges, and, as a result, fees are based on the amount of spectrum held by the carrier, regardless of the

degree of deployment or the number of sites. As a result of the new methodology, there is a nominal increase in annual

spectrum fees that will be phased in over a seven year period to 2011 for spectrum held only by Wireless. In the case of

Fido spectrum, there is a larger increase of close to $1 million per annum.

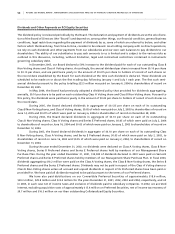

SP E C TR U M L IC E N CE IS S UE S

Late in 2003, Industry Canada released a policy document regarding a number of spectrum issues, including a discus-

sion on the existing spectrum cap, spectrum allocations for 3G networks and possible timing of a 3G spectrum auction.

Industry Canada proposed a possible 3G spectrum auction date of 2005 to 2006 for this spectrum, but to date, a final

determination on most of these matters has not yet been made. Wireless currently expects a spectrum auction either late

in 2007 or early 2008. The U.S. Federal Communications Commission (“FCC”) was expected to auction similar spectrum in

2005, but it announced on December 29, 2004 that it will conduct its auction no earlier than June 2006. Specifically, the FCC

will auction 45 MHz in each of the 1.7 gigahertz (“GHz”) and 2.1 GHz bands, which have been allocated for 3G in the U.S.

commencing June 29, 2006. In October 2004, the FCC released a plan to relocate incumbent federal government sys-

tems from the 1.7 GHz band. The proceeds of the 3G auction will be used to fund this relocation. Wireless expects that

Industry Canada will follow the spectrum allocation made by the FCC in the U.S. and that it will not proceed with a 3G

spectrum auction before the U.S. 3G spectrum auction has been concluded.

On August 27, 2004, Industry Canada rescinded the cap on ownership of mobile spectrum. Up to that time,

Canadian carriers were limited to a maximum of 55 MHz of mobile spectrum. After a public consultation earlier in 2004

as to whether the cap should be maintained, removed or increased, Industry Canada advised that the cap would be

removed, effective immediately. Industry Canada concluded that the wireless industry will require access to more spec-

trum through a future 3G wireless services auction and further stated that they will continue to monitor the wireless

industry for spectrum concentration, and manage the licensing of spectrum resources through other mechanisms at

their disposal.

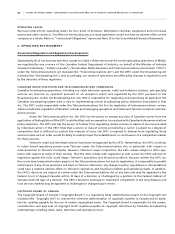

FI X E D W IR E LE S S S P EC T RU M AU C TI O N

On February 9, 2004, Industry Canada commenced an auction for one block of 30 MHz of spectrum in the 2300 MHz band

as well as three blocks of 50 MHz of spectrum and one block of 25 MHz of spectrum in the 3500 MHz band. The auction

was completed on February 16, 2004. There were over 172 geographic licence areas in Canada for each available block.

Licencees have flexibility in determining the services to be offered and the technologies to be deployed in the spectrum.

Industry Canada expected that the spectrum will be used for point-to-point or point-to-multi-point broadband services.

Wireless participated in this spectrum auction and, as a result, has acquired 33 blocks of spectrum in various licence areas

for an aggregate bid price of $5.9 million.

Industry Canada initiated another auction process to make available the blocks of spectrum that did not sell in

the February 2004 process. Parties were able to identify those blocks that they were interested in, and if there were no other

parties expressing interest in those blocks, they were the successful party. In this process, Wireless obtained an additional

nine licences for a cost of $0.2 million. The remaining licences were auctioned commencing January 10, 2005, and Wireless

was successful in supplementing its spectrum holdings from 2004 with a further 40 licences at a cost of $4.8 million. See

also below under “Wireless’ Expansion and Investment in the Inukshuk Business May Have Considerable Risks”.