Rogers 2005 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2005 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

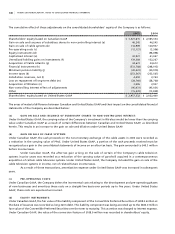

132 ROGERS 2005 ANNUAL REPORT . NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

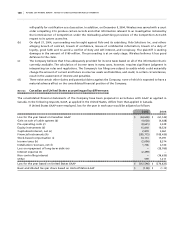

Expected return on assets represents management’s best estimate of the long-term rate of return on plan

assets applied to the fair value of the plan assets. The Company establishes its estimate of the expected rate of return on

plan assets based on the fund’s target asset allocation and estimated rate of return for each asset class. Estimated rates

of return are based on expected returns from fixed income securities which take into account bond yields. An equity

risk premium is then applied to estimate equity returns. Differences between expected and actual return are included in

actuarial gains and losses.

The estimated average remaining service periods for the plans range from 9 to 13 years. The Company does not

have any curtailment gains or losses.

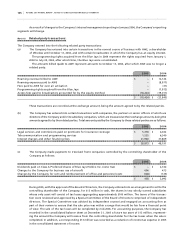

(b ) AL L OC A T IO N O F PL A N A SS E TS:

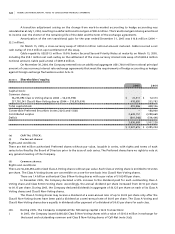

Percentage of Percentage of

plan assets, plan assets, Target asset

December 31, December 31, allocation

Asset category 2005 2004 percentage

Equity securities 59.5% 58.9% 50% to 65%

Debt securities 39.9% 40.2% 35% to 50%

Other (cash) 0.6% 0.9% 0% to 1%

100.0% 100.0%

Plan assets are comprised primarily of pooled funds that invest in common stocks and bonds. The pooled Canadian

equity fund has investments in the Company’s equity securities comprising approximately 1% of the pooled fund. This

results in approximately $0.8 million (2004 – $0.7 million) of the plans’ assets being indirectly invested in the Company’s

equity securities.

The Company makes contributions to the plans to secure the benefits of plan members and invests in permit-

ted investments using the target ranges established by the Pension Committee of the Company. The Pension Committee

reviews actuarial assumptions on an annual basis.

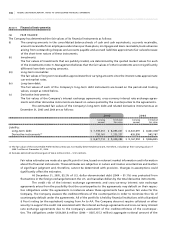

(c ) A C TUA L C O NT R IBU T IO N S T O T H E P LA N S A R E A S F O LL O WS :

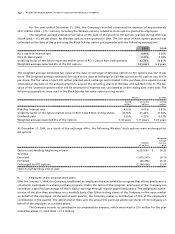

Employer Employee Total

2004 $ 19,423 $ 13,238 $ 32,661

2005

21,466 14,088 35,554

Expected contributions by the Company in 2006 are estimated to be $31.7 million.

Employee contributions for 2006 are assumed to be at levels similar to 2004 and 2005 on the assumption staff-

ing levels in the Company will remain the same on a year-over-year basis.

(d ) EX P EC T E D C AS H FL O WS :

Expected benefit payments for fiscal year ending:

2006 $ 24,600

2007 24,300

2008 24,200

2009

24,000

2010 23,900

121,000

Next 5 years 124,800

$ 245,800

Blue Jays and Fido each have defined contribution plans with total pension expense of $5.3 million in 2005 (2004 – $0.9 million).