Rogers 2005 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2005 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154

|

|

141 ROGERS 2005 ANNUAL REPORT . NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Under United States GAAP, the fair value of the conversion feature was not permitted to be separately recorded.

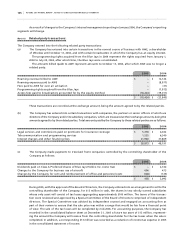

The fair value of the liability component of $576.0 million at issuance was recorded outside of shareholders’ equity and

was being accreted up to the $600.0 million face value of the Convertible Preferred Securities over the term to maturity.

This accretion was charged to interest expense.

During 2005, the Convertible Preferred Securities were converted to Class B Non-Voting shares (note 11(a)(iii)).

(e ) C AP I T AL I ZE D I N T ER E ST :

United States GAAP requires capitalization of interest costs as part of the historical cost of acquiring certain qualifying

assets that require a period of time to prepare for their intended use. This is not required under Canadian GAAP.

(f ) UN R EA L I ZE D H O LD I N G G AI N S A N D L OS S ES O N I NV E ST M E NT S :

United States GAAP requires that certain investments in equity securities that have readily determinable fair values

be stated in the consolidated balance sheets at their fair values. The unrealized holding gains and losses from these

investments, which are considered to be “available-for-sale securities” under United States GAAP, are included as a

separate component of shareholders’ equity and comprehensive income, net of related future income taxes.

(g ) AC Q UI S I TI O N O F C A BL E A T LAN T IC :

United States GAAP requires that shares issued in connection with a purchase business combination be valued based on the

market price at the announcement date of the acquisition, whereas Canadian GAAP had required such shares be valued

based on the market price at the consummation date of the acquisition. Accordingly, the Class B Non-Voting shares

issued in respect of the acquisition of Cable Atlantic in 2001 were recorded at $35.4 million more under United States

GAAP than under Canadian GAAP. This resulted in an increase to goodwill in this amount, with a corresponding increase

to contributed surplus in the amount of $35.4 million.

(h ) FI N AN C I AL IN S TRU M EN T S:

Under Canadian GAAP, the Company accounts for certain of its cross-currency interest rate exchange agreements as

hedges of specific debt instruments. Under United States GAAP, these instruments are not accounted for as hedges, but

instead changes in the fair value of the derivative instruments, reflecting primarily market changes in foreign exchange

rates, interest rates, as well as the level of short-term variable versus long-term fixed interest rates, are recognized in

income immediately. Foreign exchange translation gains and losses arising from change in period-end foreign exchange

rates on the respective long-term debt are also recognized in income.

Under United States GAAP, as a result of the adoption of United States Financial Accounting Standard Board’s

(“FASB”) Statement (“SFAS”) No. 133, Accounting for Derivative Instruments and Hedging Activities (“SFAS 133”) effective

January 1, 2001, the Company recorded a cumulative transition adjustment representing the adjustment necessary

to reflect the derivatives at their fair values at that date, net of the offsetting gains/losses on the associated hedged

long-term debt. In March 2004, $11.4 million of this cumulative transition adjustment was written off as a result of the

repayment of the long-term debt to which it relates (note 23(m)).

(i ) ST O CK - BA S ED C OM P EN S ATI O N:

Under Canadian GAAP, effective January 1, 2004, the Company adopted the fair value method of recognizing stock-based

compensation expense. For United States GAAP purposes, the intrinsic value method is used to account for stock-based

compensation of employees. Compensation expense of $34.7 million (2004 – $15.1 million) recognized under Canadian

GAAP would not be recognized under United States GAAP for the year ended December 31, 2004. The exercise price of

stock options is equal to the market value of the underlying shares at the date of grant; therefore, there is no expense

under the intrinsic value method for United States GAAP purposes for the years ended December 31, 2005 and 2004.

Effective January 1, 2004, the Blue Jays were determined to be a variable interest entity for United States GAAP

purposes and, as a result, their results were consolidated from that date (note 23(o)). As such, the employees of the Blue

Jays were considered employees of the Company effective January 1, 2004 for United States GAAP purposes. The intrin-

sic value of the options of Blue Jays’ employees was calculated as at January 1, 2004 as nil. Prior to 2004, the Blue Jays’

employees were not considered employees of the Company.