Rogers 2005 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2005 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154

|

|

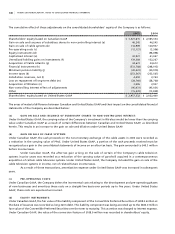

143 ROGERS 2005 ANNUAL REPORT . NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(o ) BL U E J A YS :

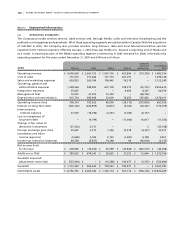

Under United States GAAP, FASB Interpretation No. 46, Consolidation of Variable Interest Entities, requires the Company

to consolidate the results of the Blue Jays effective January 1, 2004. Under Canadian GAAP, the Company consolidated

the Blue Jays effective July 31, 2004. Therefore, the United States GAAP consolidated balance sheet as at December 31,

2004 and net income of the Company for the year then ended would be unchanged from that of Canadian GAAP as the

Company recorded 100% of the losses of the Blue Jays. Under United States GAAP, consolidation from January 1, 2004

to July 31, 2004 would result in an increase in revenues of $75.0 million, cost of sales would increase by $70.1 million,

sales and marketing costs would increase by $3.8 million, operating general and administrative expenses would increase

by $17.8 million, depreciation and amortization would increase by $5.8 million, operating income would be reduced by

$22.6 million and losses from equity method investments would decrease by $22.6 million.

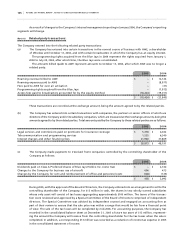

(p ) ST A TE M E NT S O F CA S H F LO W S:

(i) Canadian GAAP permits the disclosure of a subtotal of the amount of funds provided by operations before

change in non-cash operating items in the consolidated statements of cash flows. United States GAAP does not

permit this subtotal to be included.

(ii) Canadian GAAP permits bank advances to be included in the determination of cash and cash equivalents in the

consolidated statements of cash flows. United States GAAP requires that bank advances be reported as financing

cash flows. As a result, under United States GAAP, the total increase in cash and cash equivalents in 2004 in

the amount of $254.3 million reflected in the consolidated statements of cash flows would be decreased by

$10.3 million and financing activities cash flows would decrease by $10.3 million. The total decrease in cash and

cash equivalents in 2005 in the amount of $347.9 million reflected in the consolidated statements of cash flows

would be decreased by $104.0 million and financing activities cash flows would be increased by $104.0 million.

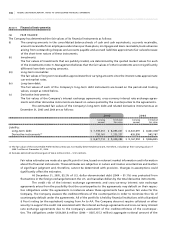

(q ) ST A TE M E NT OF COM P RE H EN S IVE IN C OM E :

United States GAAP requires the disclosure of a statement of comprehensive income. Comprehensive income generally

encompasses all changes in shareholders’ equity, except those arising from transactions with shareholders.

2005 2004

Net loss based on United States GAAP $ (312,596) $ (270,625)

Other comprehensive income, net of income taxes:

Unrealized holding gains (losses) arising during the year, net of income taxes (1,138) 69,586

Realized gains included in income, net of income tax (9,463) (10,567)

Realized losses included in income – 1,650

Minimum pension liability, net of income taxes 354 (8,483)

Comprehensive loss based on United States GAAP $ (322,843) $ (218,439)

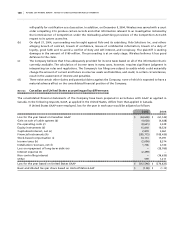

(r ) OT H ER D IS C LO S UR E S :

United States GAAP requires the Company to disclose accrued liabilities, which is not required under Canadian GAAP.

Accrued liabilities included in accounts payable and accrued liabilities as at December 31, 2005 were $1,068.6 million

(2004 – $1,100.9 million). At December 31, 2005, accrued liabilities in respect of PP&E totalled $104.0 million (2004 –

$116.0 million), accrued interest payable totalled $113.1 million (2004 – $117.6 million), accrued liabilities related to payroll

totalled $176.6 million (2004 – $173.3 million), and CRTC commitments totalled $40.4 million (2004 – $56.5 million).