Reebok 2009 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2009 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

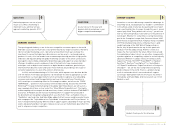

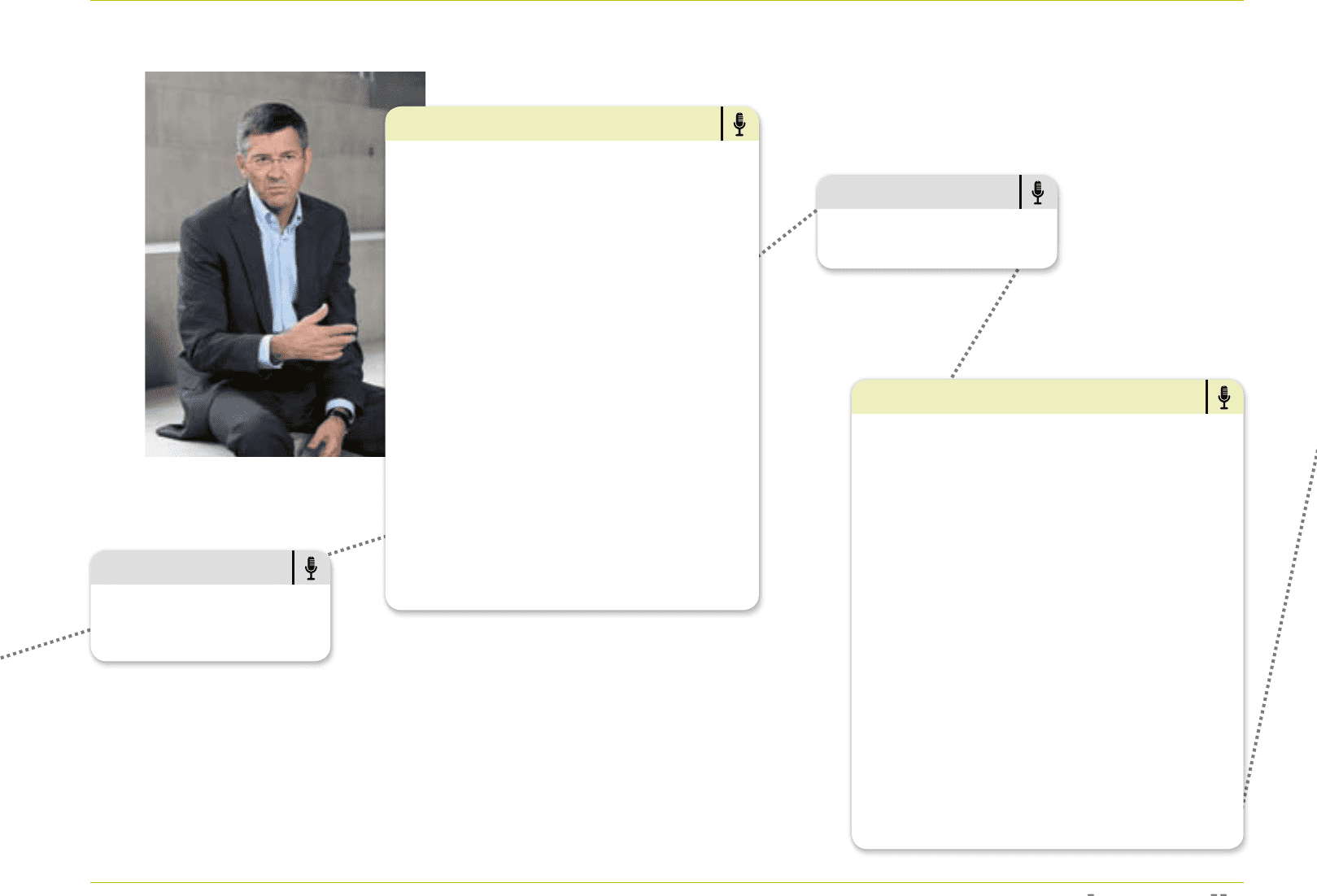

TO OUR SHAREHOLDERS Interview with the CEO 19

HERBERT HAINER

A decline in gross margin of over three percentage points to

45.4% was the primary reason for the bottom-line decrease

we suffered in 2009. There were three main reasons for

this. Firstly, input costs increased sharply versus the

prior year as a consequence of record-high raw material

prices and significant wage cost pressures in 2008 which

affected our product costs for 2009. Equally important was

the devaluation of the Russian rouble, which depreciated

considerably versus the US dollar, our functional currency

for the Russian market. As we were not able to compensate

the top-line effect with price increases, this development

squeezed gross profit by over € 200 million. Thirdly, excess

inventories at the beginning of the year meant we had to

take extra measures to clear stock at lower margins. This

was due to our commitment to product orders prior to a full

understanding of the magnitude of the economic downturn

in late 2008.

The decisive steps we started to take in late 2008 and

during 2009 to increase operational efficiency have certainly

helped us mitigate some of these effects. But at the same

time, we had to get the balance right between cutting costs

and maintaining investments in areas such as controlled

space, promotion partnerships and product innovation to

support future growth. I believe we definitely found the right

balance in 2009, and we will see material benefits from our

actions in 2010 and beyond.

HERBERT HAINER

Although our Group revenues declined 6% currency-neutral

in 2009, I believe all of our brands have made the most out of

the difficult environment, with each in some way enhancing

its market position. For adidas, in the year we celebrated the

60th anniversary of the brand, the key highlight was achieving

9% currency-neutral revenue growth in our adidas Sport Style

division to a new record sales level of € 1.65 billion. In addition,

we again showed our prowess in football as we successfully

launched many of our FIFA World Cup™ initiatives in the fourth

quarter, which had an immediate impact driving football sales

up 27% currency-neutral for the quarter. At Reebok, after

four years of hard work, we are finally seeing the first real

commercial successes from our product and creative efforts

to reposition the brand. We are leading the industry in the

emerging toning category which experts are tipping as the

next billion dollar category. Reebok has made a big statement

here with the introduction of the EasyTone™. In 2009 we over-

achieved our sales target three-fold, and we expect to sell

several million pairs of toning footwear in 2010. At TaylorMade,

our unrivalled innovation pipeline has again paid off to

tremendous success. We have extended our market share lead

in metalwoods and taken significant market share from our

major competitors in a host of categories, most notably in irons

where we are now the market leader in the United States.

QUESTION

Profitability declined significantly

in 2009. Can you outline the main

reasons for this?

QUESTION

What were the key highlights at your

major brands in 2009?