Reebok 2009 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2009 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

|

|

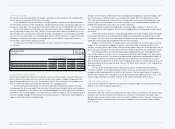

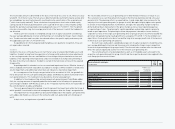

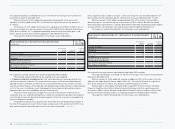

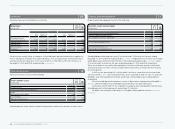

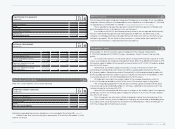

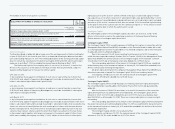

180 CONSOLIDATED FINANCIAL STATEMENTS Notes

The acquisition had the following effect on the Group’s assets and liabilities:

N

°-

04

ASHWORTH, INC.’S NET ASSETS AT THE ACQUISITION DATE

€ IN MILLIONS

Pre-acquisition

carrying

amounts Fair value

adjustments

Recognised

values on

acquisition

Cash and cash equivalents 2 — 2

Accounts receivable 20 — 20

Inventories 27 3 30

Other current assets 2 — 2

Property, plant and equipment, net 21 2 23

Trademarks and other intangible assets, net 3 34 37

Deferred tax assets 1 4 5

Borrowings (37) — (37)

Accounts payable (15) — (15)

Income taxes (0) — (0)

Accrued liabilities and provisions (6) (1) (7)

Other current liabilities (2) — (2)

Deferred tax liabilities 0 (14) (14)

Net assets 16 28 44

Negative goodwill arising on acquisition

(recognised in the income statement) 21

Purchase price settled in cash 23

Cash and cash equivalents acquired 2

Cash outflow on acquisition 21

Pre-acquisition carrying amounts were based on applicable IFRS standards.

The following valuation methods for the acquired assets were applied:

Inventories: The “pro rata basis valuation” was applied for estimating the fair value of acquired

inventories. Realised margins were added to the book values of acquired inventories. Subse-

quently, the costs for completion for selling, advertising and general administration as well as a

reasonable profit allowance were deducted.

Property, plant and equipment: The “indirect cost method” was applied for the valuation of

property, plant and equipment. The “comparison method” was exclusively applied to the valuation

of embroidery machines. In the “indirect cost method”, the cost of “as new” reproduction for each

asset or group of assets was determined by indexing the original capitalised cost. If necessary,

allowances have been taken into account for physical depreciation, functional and economic obso-

lescence. The “comparison method” was applied by estimating prices of comparable embroidery

machines in terms of age, make and model. Indirect cost estimates such as freight, installation

and set-up were also included in the valuation.

Trademarks and other intangible assets: The “relief-from-royalty method” was applied for

trademarks/trade names. The fair value was determined by discounting the royalty savings after

tax and adding a tax amortisation benefit, resulting from the amortisation of the acquired asset.

For the valuation of customer relationships, the “multi-period-excess-earnings method” was

used. The respective future excess cash flows were identified and adjusted in order to eliminate all

elements not associated with these assets. Future cash flows were measured on the basis of the

expected sales by deducting variable and sales-related imputed costs for the use of contributory

assets. Subsequently, the outcome was discounted using the appropriate discount rate and adding

a tax amortisation benefit. The “cost approach” was applied for apparel designs. These were val-

ued as the cost to recreate the current design plus the opportunity cost measured as the cash flow

impact between having pre-existing designs versus having to recreate the designs plus amortisa-

tion tax benefit. The “discounted cash flow method” was applied for covenants not-to-compete by

comparing the estimated prospective cash flows with and without the subject agreements in place.

The value of the covenants not-to-compete is the difference between these discounted cash flows

being discounted to present value at the appropriate discount rate. For the valuation of backlogs,

the “income approach” was used. The corresponding cash flows were based on the estimated

exhaustion of the backlog, and discounted with an appropriate discount rate. Charges for the use

of contributory assets and an amortisation tax benefit were also included in the calculation.

The negative goodwill resulted from the excess of net assets (fair values assigned to all

assets acquired less liabilities assumed) versus the acquisition cost paid, due to a massive

decrease in the share price of the company acquired, also taking the respective deferred taxes into

consideration.

If this acquisition had occurred on January 1, 2008, total Group net sales would have been

€ 10.9 billion and net income would have been € 611 million for the year ending December 31, 2008.

Mainly due to restructuring costs and other one-time expenses, the acquired subsidiary

contributed losses of € 13 million to the Group’s total operating result in the fiscal year 2008. Con-

tribution to net income in 2008 could not be disclosed due to the integration of financing and tax

activities.