PNC Bank 2006 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

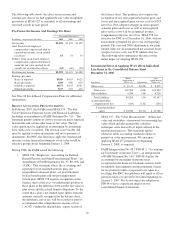

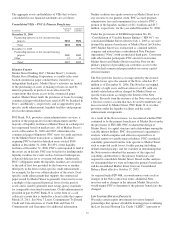

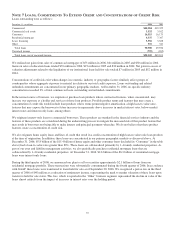

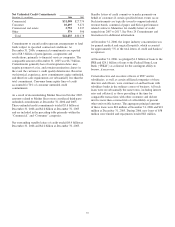

The following table sets forth regulatory capital ratios for

PNC and its only significant bank subsidiary, PNC Bank, N.A.

Regulatory Capital

Amount Ratios

December 31

Dollars in millions 2006 2005 2006 2005

Risk-based capital

Tier 1

PNC $ 8,924 $6,364 10.4% 8.3%

PNC Bank, N.A. 6,159 5,694 8.0 8.0

Total

PNC 11,559 9,277 13.5 12.1

PNC Bank, N.A. 8,541 8,189 11.1 11.5

Leverage

PNC NM NM 9.3 7.2

PNC Bank, N.A. NM NM 7.2 7.0

NM - Not Meaningful

The principal source of parent company cash flow is the

dividends it receives from PNC Bank, N.A., which may be

impacted by the following:

• Capital needs,

• Laws and regulations,

• Corporate policies,

• Contractual restrictions, and

• Other factors.

Also, there are statutory and regulatory limitations on the

ability of national banks to pay dividends or make other

capital distributions. The amount available for dividend

payments to the parent company by PNC Bank, N.A. without

prior regulatory approval was approximately $625 million at

December 31, 2006.

Under federal law, bank subsidiaries generally may not extend

credit to the parent company or its non-bank subsidiaries on

terms and under circumstances that are not substantially the

same as comparable extensions of credit to nonaffiliates. No

extension of credit may be made to the parent company or a

non-bank subsidiary which is in excess of 10% of the capital

stock and surplus of such bank subsidiary or in excess of 20%

of the capital and surplus of such bank subsidiary as to

aggregate extensions of credit to the parent company and its

non-bank subsidiaries. Such extensions of credit, with limited

exceptions, must be fully collateralized by certain specified

assets. In certain circumstances, federal regulatory authorities

may impose more restrictive limitations.

Federal Reserve Board regulations require depository

institutions to maintain cash reserves with the Federal Reserve

Bank (“FRB”). During 2006, subsidiary banks maintained

reserves which averaged $203 million.

N

OTE

5L

EGAL

P

ROCEEDINGS

Some of our subsidiaries are defendants (or have potential

contractual contribution obligations to other defendants) in

several pending lawsuits brought during late 2002 and 2003

arising out of the bankruptcy of Adelphia Communications

Corporation and its subsidiaries. There also are threatened

additional proceedings arising out of the same matters. One of

the lawsuits was brought on Adelphia’s behalf by the

unsecured creditors’ committee and equity committee in

Adelphia’s consolidated bankruptcy proceeding and was

removed to the United States District Court for the Southern

District of New York by order dated February 9, 2006. The

other lawsuits, one of which is a putative consolidated class

action, were brought by holders of debt and equity securities

of Adelphia and have been consolidated for pretrial purposes

in that district court. These lawsuits arise out of lending and

securities underwriting activities engaged in by these PNC

subsidiaries together with other financial services companies.

In the aggregate, more than 400 other financial services

companies and numerous other companies and individuals

have been named as defendants in one or more of the lawsuits.

Collectively, with respect to some or all of the defendants, the

lawsuits allege federal law claims, including violations of

federal securities and other federal laws, violations of

common law duties, aiding and abetting such violations,

voidable preference payments, and fraudulent transfers,

among other matters. The lawsuits seek unquantified

monetary damages, interest, attorneys’ fees and other

expenses, and a return of the alleged voidable preference and

fraudulent transfer payments, among other remedies. The bank

defendants, including the PNC defendants, have entered into a

settlement of the consolidated class action referred to above.

This settlement was approved by the district court in

November 2006. In December 2006, a group of class members

appealed the order approving the settlement agreement to the

United States Court of Appeals for the Second Circuit. The

amount for which we would be responsible under this

settlement is insignificant. We believe that we have defenses

to the claims against us in these lawsuits, as well as potential

claims against third parties, and intend to defend the

remaining lawsuits vigorously. These lawsuits involve

complex issues of law and fact, presenting complicated

relationships among the many financial and other participants

in the events giving rise to these lawsuits, and have not

progressed to the point where we can predict the outcome of

the remaining lawsuits other than the one for which a

settlement is pending. It is not possible to determine what the

likely aggregate recoveries on the part of the plaintiffs in these

remaining matters might be or the portion of any such

recoveries for which we would ultimately be responsible, but

the final consequences to PNC could be material.

In April 2005, an amended complaint was filed in the putative

class action against PNC, PNC Bank, N.A., our Pension Plan

and its Pension Committee in the United States District Court

for the Eastern District of Pennsylvania (originally filed in

December 2004). The complaint claims violations of the

Employee Retirement Income Security Act of 1974, as

amended (“ERISA”), arising out of the January 1, 1999

conversion of our Pension Plan from a traditional defined

benefit formula into a “cash balance” formula, the design and

continued operation of the Plan, and other related matters.

Plaintiffs seek to represent a class of all current and former

85