PNC Bank 2006 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

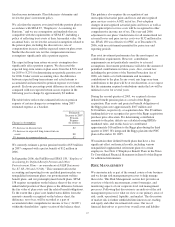

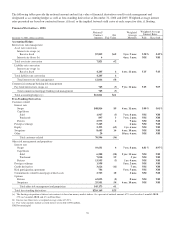

In addition to measuring the effect on net interest income

assuming parallel changes in current interest rates, we

routinely simulate the effects of a number of nonparallel

interest rate environments. The following Net Interest Income

Sensitivity To Alternative Rate Scenarios table reflects the

percentage change in net interest income over the next two

12-month periods assuming (i) the PNC Economist’s most

likely rate forecast, (ii) implied market forward rates, and

(iii) a Two-Ten Inversion (a 200 basis point inversion between

two-year and ten-year rates superimposed on current base

rates) scenario. We are inherently sensitive to a flatter or

inverted yield curve.

Net Interest Income Sensitivity To Alternative Rate

Scenarios (as of December 31, 2006)

PNC

Economist

Market

Forward

Two-Ten

Inversion

First year sensitivity 2.3% 1.6% (6.6)%

Second year sensitivity 8.4% 4.9% (6.1)%

All changes in forecasted net interest income are relative to

results in a base rate scenario where current market rates are

assumed to remain unchanged over the forecast horizon.

When forecasting net interest income, we make assumptions

about interest rates and the shape of the yield curve, the

volume and characteristics of new business, and the behavior

of existing positions. These assumptions determine the future

level of simulated net interest income in the base interest rate

scenario and the other interest rate scenarios presented in the

following table. These simulations assume that as assets and

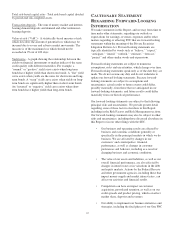

liabilities mature, they are replaced or repriced at market rates.

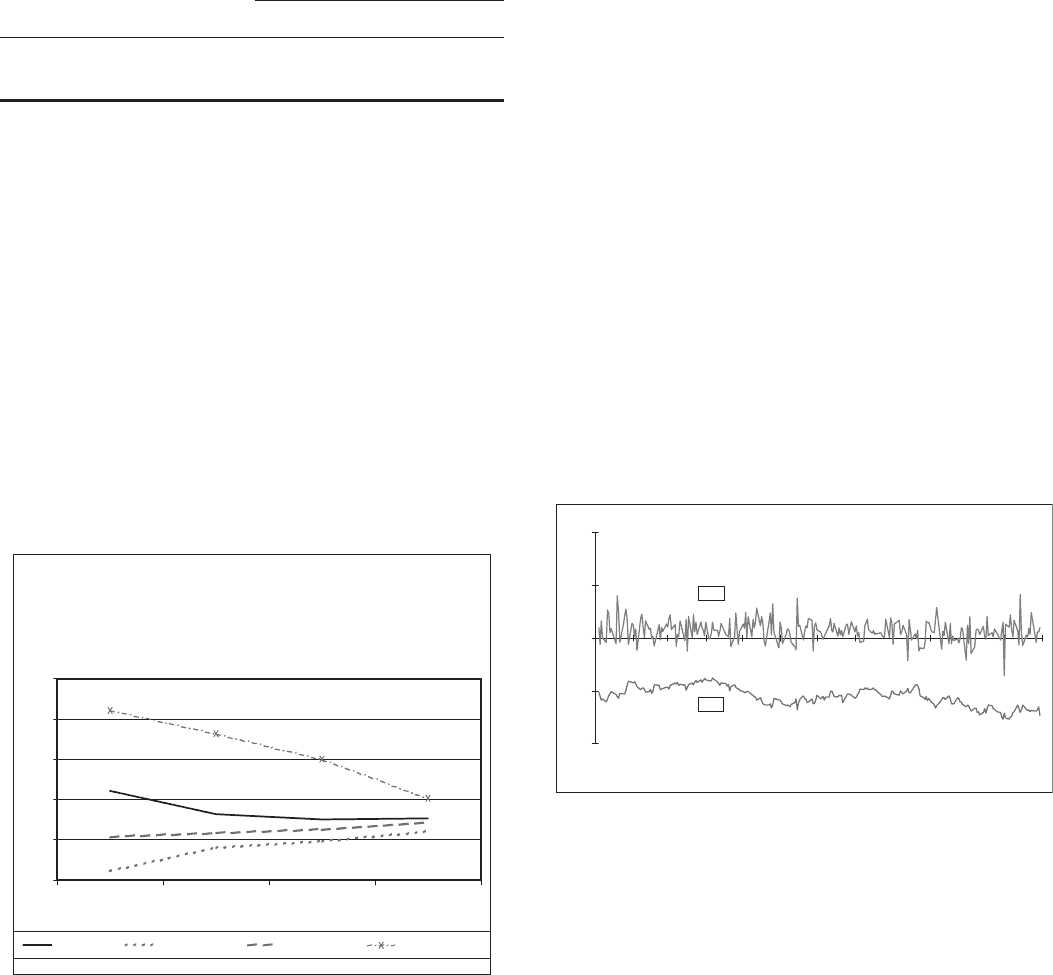

The graph below presents the yield curves for the base rate

scenario and each of the alternative scenarios one year

forward.

Alternate Interest Rate Scenarios

One Year Forward

4.25

4.75

5.25

5.75

6.25

6.75

1M LIBOR

Base Rates PNC Economist Market Forward Two-Ten Inversion

2Y Swap 3Y Swap 5Y Swap

Our risk position has become increasingly liability sensitive in

part due to the increase in market interest rates and in part due

to our balance sheet management strategy. We believe that we

have the deposit funding base and balance sheet flexibility to

adjust, where appropriate, to changing interest rates and

market conditions.

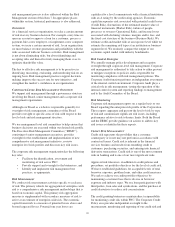

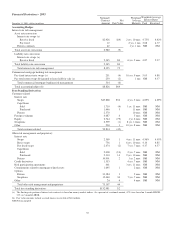

M

ARKET

R

ISK

M

ANAGEMENT

–T

RADING

R

ISK

Our trading activities primarily include customer-driven

trading in fixed income securities, equities, derivatives, and

foreign exchange contracts. They also include the

underwriting of fixed income and equity securities and

proprietary trading.

We use value-at-risk (“VaR”) as the primary means to

measure and monitor market risk in trading activities. The

Joint Risk Committee of the Board establishes an enterprise-

wide VaR limit on our trading activities.

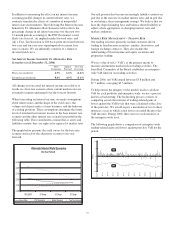

During 2006, our VaR ranged between $3.8 million and

$7.7 million, averaging $5.5 million.

To help ensure the integrity of the models used to calculate

VaR for each portfolio and enterprise-wide, we use a process

known as backtesting. The backtesting process consists of

comparing actual observations of trading-related gains or

losses against the VaR levels that were calculated at the close

of the prior day. We would expect a maximum of two to three

instances a year in which actual losses exceeded the prior day

VaR measure. During 2006, there were no such instances at

the enterprise-wide level.

The following graph shows a comparison of enterprise-wide

trading-related gains and losses against prior day VaR for the

period.

Enterprise-Wide Trading-Related Gains/Losses Versus Value at Risk YTD 2006

(10)

(5)

0

5

10

12/31/05

1/31/06

2/28/06

3/31/06

4/30/06

5/31/06

6/30/06

7/31/06

8/31/06

9/30/06

10/31/06

11/30/06

12/31/06

Millions

VaR

P&L

55