PNC Bank 2006 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

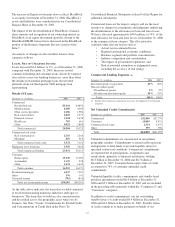

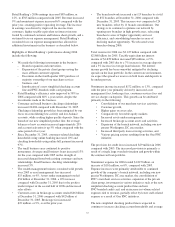

customers if specified future events occur. At December 31,

2006, the largest industry concentration was for general

medical and surgical hospitals, which accounted for

approximately 5% of the total letters of credit and bankers’

acceptances.

Leases and Related Tax and Accounting Matters

The equipment lease portfolio totaled $3.6 billion at

December 31, 2006. Aggregate residual value at risk on the

lease portfolio at December 31, 2006 was $1.1 billion. We

have taken steps to mitigate $.6 billion of this residual risk,

including residual value insurance coverage with third parties,

third party guarantees, and other actions. The portfolio

included approximately $1.7 billion of cross-border leases at

December 31, 2006. Cross-border leases are leveraged leases

of equipment located in foreign countries, primarily in western

Europe and Australia. We have not entered into cross-border

lease transactions since 2003.

Upon completing an examination of our 1998-2000 and 2001-

2003 consolidated federal income tax returns, the IRS

provided us with examination reports which propose increases

in our tax liability, principally arising from adjustments to the

timing of tax deductions from several of our cross-border

lease transactions.

While the situation with respect to these proposed adjustments

remains unresolved, we believe our reserves for these

exposures were appropriate at December 31, 2006.

In July 2006, the Financial Accounting Standards Board

(“FASB”) issued FASB Staff Position No. FAS 13-2,

Accounting for a Change or Projected Change in the Timing

of Cash Flows Relating to Income Taxes Generated by a

Leveraged Lease Transaction (“FSP 13-2”).FSP 13-2 became

effective January 1, 2007 and requires a recalculation of the

timing of income recognition and the reevaluation of lease

classification for actual or projected changes in the timing of

tax benefits for leveraged leases. Any cumulative adjustment

must be recognized through retained earnings upon adoption

of FSP 13-2. See Note 1 Accounting Policies in the Notes To

Consolidated Financial Statements in Item 8 of this Report for

additional information. Effective January 1, 2007, we

recorded a cumulative adjustment to beginning retained

earnings from the recalculations of $149 million, after-tax, as

required by FSP 13-2. This adjustment was based on our best

estimate as to the timing and amount of ultimate settlement of

this exposure. Any immediate or future reductions in earnings

from our adoption of FSP 13-2 would be recovered in

subsequent years.

The US Senate has passed a bill that, if it became law, would

have an adverse impact on the tax treatment for our cross-

border lease transactions. The US House of Representatives has

passed a different version of this legislation that does not

contain any provisions relating to the taxation of cross-border

lease transactions. The differences between the two versions of

this legislation will be resolved in conference. We cannot

predict whether or not any new law impacting the tax treatment

for our cross-border lease transactions will be enacted.

In addition to these transactions, three lease-to-service

contract transactions that we were party to were structured as

partnerships for tax purposes. However, we do not believe that

our exposure from these transactions is material to our

consolidated results of operations or financial position.

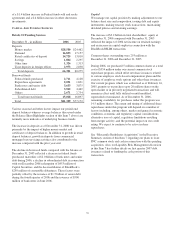

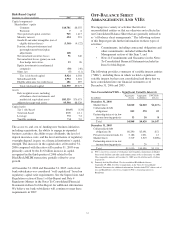

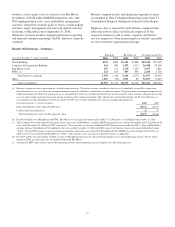

S

ECURITIES

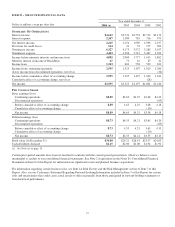

Details Of Securities (a)

Amortized Fair

In millions Cost Value

December 31, 2006

S

ECURITIES

A

VAILABLE FOR

S

ALE

Debt securities

U.S. Treasury and government agencies $611 $608

Mortgage-backed 17,325 17,208

Commercial mortgage-backed 3,231 3,219

Asset-backed 1,615 1,609

State and municipal 140 139

Other debt 90 87

Corporate stocks and other 321 321

Total securities available for sale $23,333 $23,191

December 31, 2005

S

ECURITIES

A

VAILABLE FOR

S

ALE

Debt securities

U.S. Treasury and government agencies $3,816 $3,744

Mortgage-backed 13,794 13,544

Commercial mortgage-backed 1,955 1,919

Asset-backed 1,073 1,063

State and municipal 159 158

Other debt 87 86

Corporate stocks and other 196 196

Total securities available for sale $21,080 $20,710

(a) Securities held to maturity at December 31, 2006 and 2005 were less than

$.5 million.

Securities represented 23% of total assets at both

December 31, 2006 and December 31, 2005. The increase in

total securities compared with December 31, 2005 was

primarily due to higher balances of mortgage-backed and

commercial mortgage-backed securities, which more than

offset the decline in US Treasury and government agencies

securities.

At December 31, 2006, the securities available for sale

balance included a net unrealized loss of $142 million, which

represented the difference between fair value and amortized

cost. The comparable amount at December 31, 2005 was a net

unrealized loss of $370 million. Net unrealized gains and

losses in the securities available for sale portfolio are included

in shareholders’ equity as accumulated other comprehensive

income or loss, net of tax.

The fair value of securities available for sale generally

decreases when interest rates increase and vice versa. Further

increases in interest rates in 2007, if sustained, will adversely

impact the fair value of securities available for sale going

forward compared with the fair value at December 31, 2006.

The expected weighted-average life of securities available for

sale was 3 years and 8 months at December 31, 2006 and 4

years and 1 month at December 31, 2005.

28