PNC Bank 2006 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

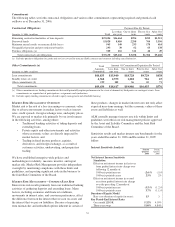

2006. The comparable percentages at December 31, 2005

were 314% and 1.21%.

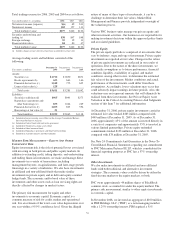

C

REDIT

D

EFAULT

S

WAPS

Credit default swaps provide, for a fee, an assumption by a

third party of a portion of the credit risk related to the

underlying financial instruments. We use the contracts to

mitigate credit risk associated with commercial lending

activities as well as proprietary derivative and convertible

bond trading. Credit default swaps are included in the Free-

Standing Derivatives table in the Financial Derivatives section

of this Risk Management discussion. Net losses from credit

default swaps are reflected in the Trading line item on our

Consolidated Income Statement and were not significant in

2006 or 2005.

O

PERATIONAL

R

ISK

M

ANAGEMENT

Operational risk is defined as the risk of financial loss or other

damage to us resulting from inadequate or failed internal

processes or systems, human factors, or from external events.

Operational risk may occur in any of our business activities

and manifests itself in various ways, including but not limited

to the following:

• Errors related to transaction processing and systems,

• Breaches of the system of internal controls and

compliance requirements, and

• Business interruptions and execution of unauthorized

transactions and fraud by employees or third parties.

Operational losses may arise from legal actions due to

operating deficiencies or noncompliance with contracts, laws

or regulations.

To monitor and control operational risk, we maintain a

comprehensive framework including policies and a system of

internal controls that is designed to manage risk and to

provide management with timely and accurate information

about the operations of PNC. Management at each business

unit is primarily responsible for its operational risk

management program, given that operational risk management

is integral to direct business management and most easily

effected at the business unit level. Corporate Operational Risk

Management, reporting to the Chief Risk Officer, oversees

day-to-day operational risk management activities.

Technology Risk

The technology risk management program is a significant

component of the operational risk framework. We have an

integrated security and technology risk management

framework designed to help ensure a secure, sound, and

compliant infrastructure for information management. The

technology risk management process is aligned with the

strategic direction of the businesses and is integrated into the

technology management culture, structure and practices. The

application of this framework across the enterprise helps to

support comprehensive and reliable internal controls.

Our business resiliency program manages the organization’s

capabilities to provide services in the case of an event that

results in material disruption of business activities.

Prioritization of investments in people, processes, technology

and facilities are based on different types of events, business

risk and criticality. Comprehensive testing validates our

resiliency capabilities on an ongoing basis, and an integrated

governance model is designed to help assure transparent

management reporting.

Insurance

As a component of our risk management practices, we

purchase insurance designed to protect us against accidental

loss or losses which, in the aggregate, may significantly affect

personnel, property, financial objectives, or our ability to

continue to meet our responsibilities to our various

stakeholder groups.

PNC, through subsidiary companies, Alpine Indemnity

Limited and PNC Insurance Corp., participates as a direct

writer for its general liability, automobile liability, workers’

compensation, property and terrorism programs. PNC’s risks

associated with its participation as a direct writer for these

programs are mitigated through policy limits and annual

aggregate limits. Risks in excess of Alpine and PNC Insurance

Corp. policy limits and annual aggregates are mitigated

through the purchase of direct coverage provided by various

insurers up to limits established by PNC’s Corporate

Insurance Committee.

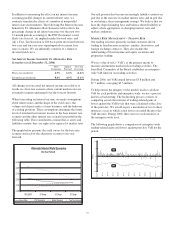

L

IQUIDITY

R

ISK

M

ANAGEMENT

Liquidity risk is the risk of potential loss if we were unable to

meet our funding requirements at a reasonable cost. We

manage liquidity risk to help ensure that we can obtain cost-

effective funding to meet current and future obligations under

both normal “business as usual” and stressful circumstances.

Asset and Liability Management (“ALM”) is accountable for

managing the liquidity position within the limits and

guidelines set forth in our risk management policies. Market

Risk Management provides independent oversight for the

measurement, monitoring and reporting of PNC’s liquidity

risk.

We typically maintain our liquidity position through:

• A large and stable deposit base derived from our

retail and wholesale banking activities,

• A portfolio of liquid investment securities,

• Diversified sources of short-term and long-term

wholesale funding, and

• Significant unused borrowing capacity at both the

Federal Home Loan Bank of Pittsburgh (“FHLB-

Pittsburgh”) and the Federal Reserve discount

window.

Our largest source of liquidity on a consolidated basis is the

deposit base that comes from our retail and wholesale banking

51