PNC Bank 2006 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

Specifically, a yield curve was produced for a universe

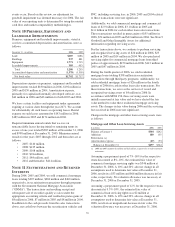

containing the majority of US-issued Aa grade corporate

bonds, all of which were non-callable (or callable with make-

whole provisions).

Excluded from this yield curve were the 10% of the bonds

with the highest yields and the 10% with the lowest yields.

For each plan, the discount rate was determined as the level

equivalent rate that would produce the same present value

obligation as that using spot rates aligned with the projected

benefit payments.

The health care cost trend rate assumptions shown in the

preceding tables relate only to the postretirement benefit

plans. A one-percentage-point change in assumed health care

cost trend rates would have the following effects:

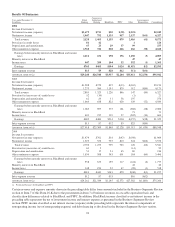

Year ended December 31, 2006

In millions Increase Decrease

Effect on total service and interest cost $1 $(1)

Effect on year-end benefit obligation 11 (9)

As discussed in Note 1 Accounting Policies, we adopted

SFAS 158 at December 31, 2006. Under SFAS 158, beginning

December 31, 2006, unamortized actuarial gains and losses

and prior service costs and credits are recognized in AOCI

each December 31, while amortization of these amounts

through net periodic benefit cost will occur in accordance with

FAS 87 and 106. The estimated amounts that will be

amortized in 2007 are as follows:

2007 Estimate

Year ended December 31

In millions

Qualified

Pension

Nonqualified

Pension

Postretirement

Benefits

Prior service cost (credit) $(7)

Net actuarial loss (gain) $1 $2 1

Total $1 $2 $(6)

M

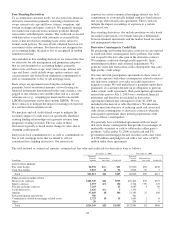

EDICARE

R

EFORM

In December 2003, the Medicare Prescription Drug

Improvement and Modernization Act of 2003 (the “Act”) was

enacted. The Act established a prescription drug benefit under

Medicare, known as “Medicare Part D,” and a federal subsidy

to sponsors of postretirement plans that provide a benefit that

is at least actuarially equivalent to Medicare Part D. Our

actuaries have attested that the benefits we provide to certain

participants are at least actuarially equivalent to Medicare

Part D, and, accordingly, we will be entitled to a subsidy.

D

EFINED

C

ONTRIBUTION

P

LANS

We have a contributory, qualified defined contribution plan

that covers substantially all employees except those covered

by other plans as identified below. Under this plan, employee

contributions up to 6% of eligible compensation as defined by

the plan are matched 100%, subject to Code limitations. The

plan is a 401(k) plan and includes an employee stock

ownership (“ESOP”) feature. Employee contributions are

invested in a number of investment options available under the

plan, including a PNC common stock fund and several

BlackRock mutual funds, at the direction of the employee. All

shares of PNC common stock held by the plan are part of the

ESOP. Employee contributions to the plan for 2006, 2005 and

2004 were matched primarily by shares of PNC common

stock held in treasury, except in the case of those participants

who have exercised their diversification election rights to have

their matching portion in other investments available within

the plan. Effective November 22, 2005, we amended the plan

to provide all participants the ability to diversify the matching

portion of their plan account invested in shares of PNC

common stock into other investments available within the

plan. Prior to this amendment, only participants age 50 or

older were permitted to exercise this diversification option.

Employee benefits expense related to this plan was $52

million in 2006, $47 million in 2005 and $48 million in 2004.

We measured employee benefits expense as the fair value of

the shares and cash contributed to the plan by PNC.

In conjunction with the BlackRock deconsolidation,

BlackRock employees ceased participating in the plan

September 30, 2006. On October 3, 2006, approximately $127

million in plan assets were transferred from the plan.

Additionally, Hilliard Lyons sponsors a contributory, qualified

defined contribution plan that covers substantially all of its

employees who are not covered by the plan described above.

Contributions to this plan are made in cash and include a base

contribution for those participants employed at December 31,

a matching of employee contributions, and a discretionary

profit sharing contribution as determined by Hilliard Lyons’

Executive Compensation Committee. Employee benefits

expense for this plan was $5 million in 2006, $6 million in

2005 and $5 million in 2004.

Effective July 1, 2004, we adopted a separate qualified

defined contribution plan that covers substantially all

US-based PFPC employees not covered by our plan. The plan

is a 401(k) plan and includes an ESOP feature. Under this

plan, employee contributions of up to 6% of eligible

compensation as defined by the plan may be matched annually

based on PFPC performance levels. Participants must be

employed as of December 31 of each year to receive this

annual contribution. The performance-based employer

matching contribution will be made primarily in shares of

PNC common stock held in treasury, except in the case of

those participants who have exercised their diversification

election rights to have their matching portion in other

investments available within the plan. Mandatory employer

contributions to this plan are made in cash and include

employer basic and transitional contributions. Employee-

directed contributions are invested in a number of investment

options available under the plan, including a PNC common

stock fund and several BlackRock mutual funds, at the

direction of the employee. Effective November 22, 2005, we

amended the plan to provide all participants the ability to

104