PNC Bank 2006 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

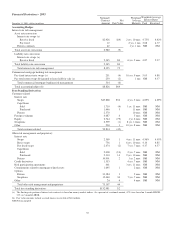

Total risk-based capital ratio - Total risk-based capital divided

by period-end risk-weighted assets.

Transaction deposits - The sum of money market and interest-

bearing demand deposits and demand and other noninterest-

bearing deposits.

Value-at-risk (“VaR”) - A statistically-based measure of risk

which describes the amount of potential loss which may be

incurred due to severe and adverse market movements. The

measure is of the maximum loss which should not be

exceeded on 99 out of 100 days.

Yield curve - A graph showing the relationship between the

yields on financial instruments or market indices of the same

credit quality with different maturities. For example, a

“normal” or “positive” yield curve exists when long-term

bonds have higher yields than short-term bonds. A “flat” yield

curve exists when yields are the same for short-term and long-

term bonds. A “steep” yield curve exists when yields on long-

term bonds are significantly higher than on short-term bonds.

An “inverted” or “negative” yield curve exists when short-

term bonds have higher yields than long-term bonds.

C

AUTIONARY

S

TATEMENT

R

EGARDING

F

ORWARD

-L

OOKING

I

NFORMATION

We make statements in this Report, and we may from time to

time make other statements, regarding our outlook or

expectations for earnings, revenues, expenses and/or other

matters regarding or affecting PNC that are forward-looking

statements within the meaning of the Private Securities

Litigation Reform Act. Forward-looking statements are

typically identified by words such as “believe,” “expect,”

“anticipate,” “intend,” “outlook,” “estimate,” “forecast,”

“project” and other similar words and expressions.

Forward-looking statements are subject to numerous

assumptions, risks and uncertainties, which change over time.

Forward-looking statements speak only as of the date they are

made. We do not assume any duty and do not undertake to

update our forward-looking statements. Because forward-

looking statements are subject to assumptions and

uncertainties, actual results or future events could differ,

possibly materially, from those that we anticipated in our

forward-looking statements, and future results could differ

materially from our historical performance.

Our forward-looking statements are subject to the following

principal risks and uncertainties. We provide greater detail

regarding some of these factors elsewhere in this Report,

including in the Risk Factors and Risk Management sections.

Our forward-looking statements may also be subject to other

risks and uncertainties, including those discussed elsewhere in

this Report or in our other filings with the SEC.

• Our business and operating results are affected by

business and economic conditions generally or

specifically in the principal markets in which we do

business. We are affected by changes in our

customers’ and counterparties’ financial

performance, as well as changes in customer

preferences and behavior, including as a result of

changing business and economic conditions.

• The value of our assets and liabilities, as well as our

overall financial performance, are also affected by

changes in interest rates or in valuations in the debt

and equity markets. Actions by the Federal Reserve

and other government agencies, including those that

impact money supply and market interest rates, can

affect our activities and financial results.

• Competition can have an impact on customer

acquisition, growth and retention, as well as on our

credit spreads and product pricing, which can affect

market share, deposits and revenues.

• Our ability to implement our business initiatives and

strategies, including the final phases of our One PNC

65