PNC Bank 2006 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

We estimate that at December 31, 2006 the effective duration

of securities available for sale is 2.6 years for an immediate

50 basis points parallel increase in interest rates and 2.2 years

for an immediate 50 basis points parallel decrease in interest

rates. Comparable amounts at December 31, 2005 were

2.7 years and 2.4 years, respectively.

We evaluate our portfolio of securities available for sale in

light of changing market conditions and other factors and,

where appropriate, take steps intended to improve our overall

positioning.

During mid-August through early September 2006, we

performed a comprehensive review of our securities available

for sale portfolio and, by the end of September 2006,

completed the process of executing portfolio rebalancing

actions in response to the changing economic landscape,

recent statements and actions by the Federal Open Market

Committee (in particular, the decision not to raise the Fed

funds target rate), and our desire to position the securities

portfolio to optimize total return performance over the long

term.

As a result, we repositioned our securities portfolio according

to our market views. This included reallocating exposure to

certain sectors, selling securities holdings we believed would

likely underperform on a relative value basis, and retaining

certain existing securities and purchasing incremental

securities all of which we believe will outperform the market

going forward as further discussed below.

As part of the rebalancing, we assessed the entire securities

available for sale portfolio of which, for the majority of

positions, fair value was less than amortized cost. We

executed a strategy to reduce our US government agency and

mortgage-backed security sector allocations and increase our

interest rate swap sector allocation. We sold substantially all

of our US government agency securities to reduce our interest

rate spread exposure to that asset class. The US government

agency securities that we retained are characterized by

relatively short terms to maturity and smaller individual

security balances. We also sold specific securities in the

mortgage-backed portfolio (i.e., all of our holdings of specific

coupon US government agency pass-through securities and

collateralized mortgage obligations having specific collateral

characteristics), and in the commercial mortgage-backed

portfolio (i.e., all of our holdings of specific vintage

securities) that we believe, given the underlying collateral,

will underperform on a relative value basis. We retained the

remaining holdings in our mortgage-backed portfolio

including all of our holdings of mortgage-backed securities

collateralized by hybrid adjustable rate mortgage loans, our

commercial mortgage-backed portfolio and our asset-backed

portfolio. Our objective was to reduce the portfolio credit

spread and interest rate volatility exposures, to position the

portfolio for a steeper yield curve and to optimize the relative

value performance of the portfolio. We assessed the securities

retained relative to the same portfolio objectives, our market

view and outlook, our desired sector allocations and our

expectation of performance relative to market benchmarks,

and, given our assessment, we confirmed our intent to hold

these remaining securities until either recovery of fair value or

maturity.

The portfolio rebalancing resulted in the sale during the third

quarter of 2006 of $6.0 billion of securities available for sale

at an aggregate pretax loss of $196 million, or $127 million

after-tax. In connection with this rebalancing, we purchased

approximately $1.8 billion of securities and added

approximately $4.0 billion of interest rate swaps to maintain

our interest rate risk position. We also reduced wholesale

funding as a result of the actions taken.

The resulting net realized losses on the sale of the securities

during the third quarter of 2006 were previously reflected as

net unrealized securities losses within accumulated other

comprehensive loss in the shareholders’ equity section of

PNC’s Consolidated Balance Sheet. Accordingly, total

shareholders’ equity did not change as a result of these

actions.

See the Consolidated Income Statement Review portion of the

2005 Versus 2004 section of this Item 7 for details of steps

taken in the second quarter of 2005 regarding the sale of

securities available for sale and related actions.

L

OANS

H

ELD

F

OR

S

ALE

During the third quarter of 2006, we announced our plan to

sell or securitize approximately $2.1 billion of loans from our

residential mortgage portfolio. These transactions were

substantially consummated during the fourth quarter of 2006.

In accordance with GAAP, these loans were transferred to

loans held for sale as of September 30, 2006. We recognized a

pretax loss in the third quarter of 2006 of $48 million as a

reduction of noninterest income, representing the mark to

market valuation of these loans upon transfer to held for sale

status. This loss, which is reported in the “Other” business

segment, represented the decline in value of the loans almost

entirely from the impact of increases in interest rates over the

holding period.

Education loans held for sale totaled $1.3 billion at

December 31, 2006 and $1.9 billion at December 31, 2005

and represented the majority of our loans held for sale at each

date. We classify substantially all of our education loans as

loans held for sale. Generally, we sell education loans when

the loans are placed into repayment status. Gains on sales of

education loans totaled $33 million for 2006, $19 million for

2005 and $30 million for 2004. These gains are reflected in

the other noninterest income line item in our Consolidated

Income Statement and in the results of the Retail Banking

business segment.

O

THER

A

SSETS

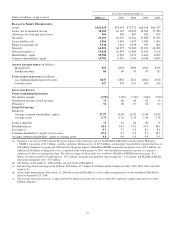

The increase of $2.5 billion in “Assets-Other” in the preceding

“Summarized Balance Sheet Data” table includes the impact

29