PNC Bank 2006 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

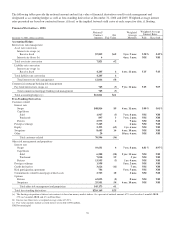

activities. Other borrowed funds come from a diverse mix of

short and long-term funding sources. Liquid assets and unused

borrowing capacity from a number of sources are also

available to maintain our liquidity position. Liquid assets

consist of short-term investments (federal funds sold, resale

agreements and other short-term investments, including

trading securities) and securities available for sale. At

December 31, 2006, our liquid assets totaled $28.1 billion,

with $10.6 billion pledged as collateral for borrowings, trust,

and other commitments.

Bank Level Liquidity

PNC Bank, N.A. is a member of FHLB-Pittsburgh and as such

has access to advances from FHLB-Pittsburgh secured

generally by residential mortgages, other real estate related

loans, and mortgage-backed securities. At December 31, 2006,

we maintained significant unused borrowing capacity from the

FHLB-Pittsburgh under current collateral requirements.

We can also obtain funding through alternative forms of

borrowing, including federal funds purchased, repurchase

agreements, and short and long-term debt issuances. In July

2004, PNC Bank, N.A. established a program to offer up to

$20 billion in senior and subordinated unsecured debt

obligations with maturities of more than nine months.

Through December 31, 2006, PNC Bank, N.A. had issued

$2.9 billion of debt under this program, including

$500 million of 18-month floating rate notes, due January

2008, issued during the second quarter of 2006. None of the

2006 issuances outlined above is redeemable or subject to

repayment at the option of the holder prior to maturity.

In December 2004, PNC Bank, N.A. established a program to

offer up to $3.0 billion of its commercial paper. As of

December 31, 2006, there were no issuances outstanding

under this program.

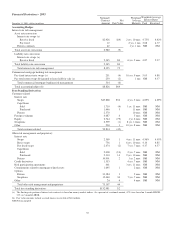

Parent Company Liquidity

Our parent company’s routine funding needs consist primarily

of dividends to PNC shareholders, share repurchases, debt

service, the funding of non-bank affiliates, and acquisitions.

Parent company liquidity guidelines are designed to help

ensure that sufficient liquidity is available to meet these

requirements over the succeeding 12-month period. In

managing parent company liquidity we consider funding

sources, such as expected dividends to be received from PNC

Bank, N.A. and potential debt issuance, and discretionary

funding uses, the most significant of which is the external

dividend to be paid on PNC’s stock.

The principal source of parent company cash flow is the

dividends it receives from PNC Bank, N.A., which may be

impacted by the following:

• Capital needs,

• Laws and regulations,

• Corporate policies,

• Contractual restrictions, and

• Other factors.

Also, there are statutory and regulatory limitations on the

ability of national banks to pay dividends or make other

capital distributions or to extend credit to the parent company

or its non-bank subsidiaries. We provide additional

information on these limitations in Note 4 Regulatory Matters

in the Notes To Consolidated Financial Statements included in

Item 8 of this Report and include such information here by

reference. Dividends may also be impacted by the bank’s

capital needs and by contractual restrictions. The amount

available for dividend payments to the parent company by

PNC Bank, N.A. without prior regulatory approval was

approximately $625 million at December 31, 2006.

In addition to dividends from PNC Bank, N.A., other sources

of parent company liquidity include cash and short-term

investments, as well as dividends and loan repayments from

other subsidiaries and dividends or distributions from equity

investments. As of December 31, 2006, the parent company

had approximately $1.4 billion in funds available from its cash

and short-term investments. During 2006, BlackRock

dividends of approximately $74 million were paid to our

intermediate bank holding company and were available for

payment to the parent company.

We can also generate liquidity for the parent company and

PNC’s non-bank subsidiaries through the issuance of

securities in public or private markets.

• In October 2006, we issued $450 million of floating

rate senior notes that mature in October 2008.

Interest will be reset monthly to 1-month LIBOR plus

2 basis points and will be paid monthly.

• In December 2006, we issued $1 billion of floating-

rate exchangeable senior notes due December 2036

through a private placement. Interest is reset

quarterly to 3-month LIBOR less 40 basis points and

is paid quarterly. See Note 13 Borrowed Funds in the

Notes To Consolidated Financial Statements in

Item 8 of this Report for further information on this

issuance.

During 2006, $1.1 billion of parent company senior debt

matured, all during the third quarter. As of December 31,

2006, there were $566 million of parent company obligations

with maturities of less than one year.

In December 2006, we elected to redeem all of the underlying

Capital Securities related to the following trusts, totaling

$453 million:

• PNC Capital Trust A ($350 million),

• Riggs Trust I ($73 million), and

• UNB Trust II ($30 million).

At December 31, 2006, we had unused capacity under

effective shelf registration statements of approximately

52