PNC Bank 2006 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

N

OTE

7L

OANS

,C

OMMITMENTS

T

O

E

XTEND

C

REDIT AND

C

ONCENTRATIONS OF

C

REDIT

R

ISK

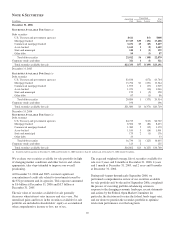

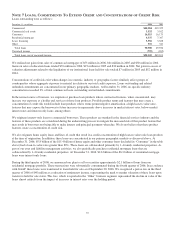

Loans outstanding were as follows:

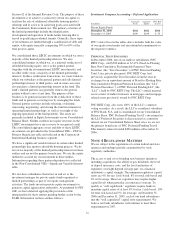

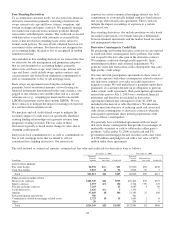

December 31 - in millions 2006 2005

Commercial $20,584 $19,325

Commercial real estate 3,532 3,162

Consumer 16,515 16,173

Residential mortgage 6,337 7,307

Lease financing 3,556 3,628

Other 376 341

Total loans 50,900 49,936

Unearned income (795) (835)

Total loans, net of unearned income $50,105 $49,101

We realized net gains from sales of commercial mortgages of $55 million in 2006, $61 million in 2005 and $50 million in 2004.

Gains on sales of education loans totaled $33 million in 2006, $19 million in 2005 and $30 million in 2004. Net gains in excess of

valuation adjustments related to the liquidation of our institutional loans held for sale totaled $7 million in 2005 and $52 million in

2004.

Concentrations of credit risk exist when changes in economic, industry or geographic factors similarly affect groups of

counterparties whose aggregate exposure is material in relation to our total credit exposure. Loans outstanding and related

unfunded commitments are concentrated in our primary geographic markets. At December 31, 2006, no specific industry

concentration exceeded 3% of total commercial loans outstanding and unfunded commitments.

In the normal course of business, we originate or purchase loan products whose contractual features, when concentrated, may

increase our exposure as a holder and servicer of those loan products. Possible product terms and features that may create a

concentration of credit risk would include loan products whose terms permit negative amortization, a high loan-to-value ratio,

features that may expose the borrower to future increases in repayments above increases in market interest rates, below-market

interest rates and interest-only loans, among others.

We originate interest-only loans to commercial borrowers. These products are standard in the financial services industry and the

features of these products are considered during the underwriting process to mitigate the increased risk of this product feature that

may result in borrowers not being able to make interest and principal payments when due. We do not believe that these product

features create a concentration of credit risk.

We also originate home equity loans and lines of credit that result in a credit concentration of high loan-to-value ratio loan products

at the time of origination. In addition, these loans are concentrated in our primary geographic markets as discussed above. At

December 31, 2006, $5.8 billion of the $15.4 billion of home equity and other consumer loans (included in “Consumer” in the table

above) had a loan-to-value ratio greater than 80%. These loans are collateralized primarily by 1-4 family residential properties. As

part of our asset and liability management activities, we also periodically purchase residential mortgage loans that are

collateralized by 1-4 family residential properties. At December 31, 2006, $2.6 billion of the $6.3 billion of residential mortgage

loans were interest-only loans.

During the third quarter of 2006, we announced our plan to sell or securitize approximately $2.1 billion of loans from our

residential mortgage portfolio. These transactions were substantially consummated during the fourth quarter of 2006. In accordance

with GAAP, these loans were transferred to loans held for sale as of September 30, 2006. We recognized a pretax loss in the third

quarter of 2006 of $48 million as a reduction of noninterest income, representing the mark to market valuation of these loans upon

transfer to held for sale status. This loss, which is reported in the “Other” business segment, represented the decline in value of the

loans almost entirely from the impact of increases in interest rates over the holding period.

92