PNC Bank 2006 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

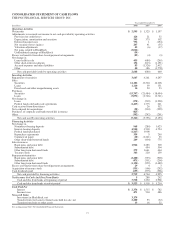

• Demand for commercial loans, including commercial

real estate loans grew during the year, reflected in the

$3.1 billion increase in these loan categories.

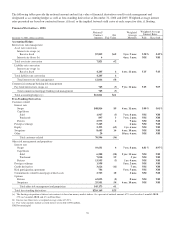

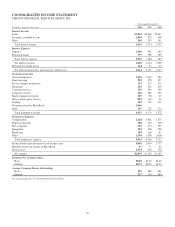

Securities

Total securities at December 31, 2005 were $20.7 billion

compared with $16.8 billion at December 31, 2004. Securities

represented 23% of total assets at December 31, 2005

compared with 21% at December 31, 2004. The increase in

total securities compared with December 31, 2004 was

primarily due to increases in mortgage-backed securities and

commercial mortgage-backed securities, partially offset by

declines in US Treasury and government agencies and asset-

backed securities. The increase in 2005 also reflected the

impact of Riggs.

At December 31, 2005, the securities available for sale

balance included a net unrealized loss of $370 million, which

represented the difference between fair value and amortized

cost. The comparable amount at December 31, 2004 was a net

unrealized loss of $102 million. The impact on bond prices of

increases in interest rates during 2005 was reflected in the net

unrealized loss position at December 31, 2005. The expected

weighted-average life of securities available for sale was 4

years and 1 month at December 31, 2005 compared with 2

years and 8 months at December 31, 2004.

Loans Held For Sale

Education loans held for sale totaled $1.9 billion at

December 31, 2005, and $1.1 billion at December 31, 2004

and represented the majority of our loans held for sale at each

date. Gains on sales of education loans totaled $19 million for

2005 and $30 million for 2004. These gains are reflected in

the other noninterest income line item in our Consolidated

Income Statement.

Asset Quality

Nonperforming assets were $216 million at December 31,

2005, an increase of $41 million from December 31, 2004.

The increase in nonperforming assets was primarily due to an

increase in nonaccrual asset-based loans. The ratio of

nonperforming assets to total loans, loans held for sale and

foreclosed assets was .42% at December 31, 2005 compared

with .39% at December 31, 2004. The allowance for loan and

lease losses was $596 million and represented 1.21% of total

loans and 314% of nonperforming loans at December 31,

2005. The comparable amounts were $607 million, 1.40% and

424%, respectively, at December 31, 2004.

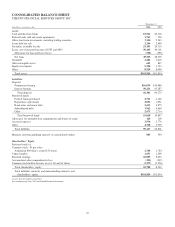

Funding Sources

Total funding sources were $77.2 billion at December 31,

2005 and $65.2 billion at December 31, 2004. The increase of

$12 billion in funding sources was comprised of a $7 billion

increase in total deposits and a $5 billion increase in total

borrowed funds. The increase in deposits reflected sales and

retention efforts related to core deposits as well as the impact

of our expansion into the greater Washington, DC area.

Higher borrowed funds at December 31, 2005 were driven in

part by the following 2005 transactions:

• Senior bank note issuances totaling $925 million,

• Senior debt issuances of $1.1 billion and

BlackRock’s issuance of $250 million of convertible

debentures,

• Subordinated bank debt issuance of $500 million and

the assumption of $345 million of subordinated debt

related to the Riggs transaction,

• $1 billion of FHLB advances, and

• Higher short-term borrowings to fund asset growth.

These increases were partially offset by maturities of $750

million of senior bank notes and $350 million of subordinated

debt during 2005.

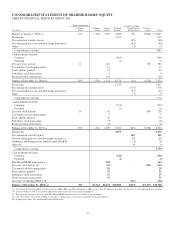

Shareholders’ Equity

The increase of $1.1 billion, to $8.6 billion, in total

shareholders’ equity at December 31, 2005 compared with the

prior year-end was primarily attributable to the impact of

retained earnings of $750 million and the issuance of

$356 million of shares in connection with the Riggs

acquisition.

Regulatory capital ratios at December 31, 2005 were 7.2% for

leverage, 8.3% for tier 1 risk-based and 12.1% for total risk-

based capital. At December 31, 2004, the regulatory capital

ratios were 7.6% for leverage, 9.0% for tier 1 risk-based and

13.0% for total risk-based capital.

Glossary of Terms

Accounting/administration net fund assets - Net domestic and

foreign fund investment assets for which we provide

accounting and administration services. We do not include

these assets on our Consolidated Balance Sheet.

Adjusted average total assets - Primarily comprised of total

average quarterly (or annual) assets plus (less) unrealized

losses (gains) on available-for-sale debt securities, less

goodwill and certain other intangible assets (net of eligible

deferred taxes).

Annualized - Adjusted to reflect a full year of activity.

Assets under management - Assets over which we have sole or

shared investment authority for our customers/clients. We do

not include these assets on our Consolidated Balance Sheet.

Basis point - One hundredth of a percentage point.

Charge-off - Process of removing a loan or portion of a loan

from our balance sheet because it is considered uncollectible.

We also record a charge-off when a loan is transferred to held

for sale by reducing the loan’s carrying amount by the

allowance for loan losses associated with such loan or if the

loan’s market value is less than its carrying amount.

62