PNC Bank 2006 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

N

OTE

17 E

MPLOYEE

B

ENEFIT

P

LANS

P

ENSION

A

ND

P

OSTRETIREMENT

P

LANS

We have a noncontributory, qualified defined benefit pension

plan covering eligible employees. Benefits are derived from a

cash balance formula based on compensation levels, age and

length of service. Pension contributions are based on an

actuarially determined amount necessary to fund total benefits

payable to plan participants.

We also maintain nonqualified supplemental retirement plans

for certain employees. We also provide certain health care and

life insurance benefits for qualifying retired employees

(“postretirement benefits”) through various plans. The

nonqualified pension and postretirement benefit plans are

unfunded.

During the second quarter of 2005, we acquired a frozen

defined benefit pension plan as a result of the Riggs

acquisition. Plan assets and projected benefit obligations of

the Riggs plan were approximately $107 million and $116

million, respectively, at acquisition date. The $9 million

funding deficit was recognized as part of the Riggs acquisition

purchase price allocation. For determining contribution

amounts to the plan, deficits are calculated using ERISA-

mandated rules, and on this basis we contributed

approximately $16 million to the Riggs plan during the third

quarter of 2005. We integrated the Riggs plan into the PNC

plan on December 30, 2005.

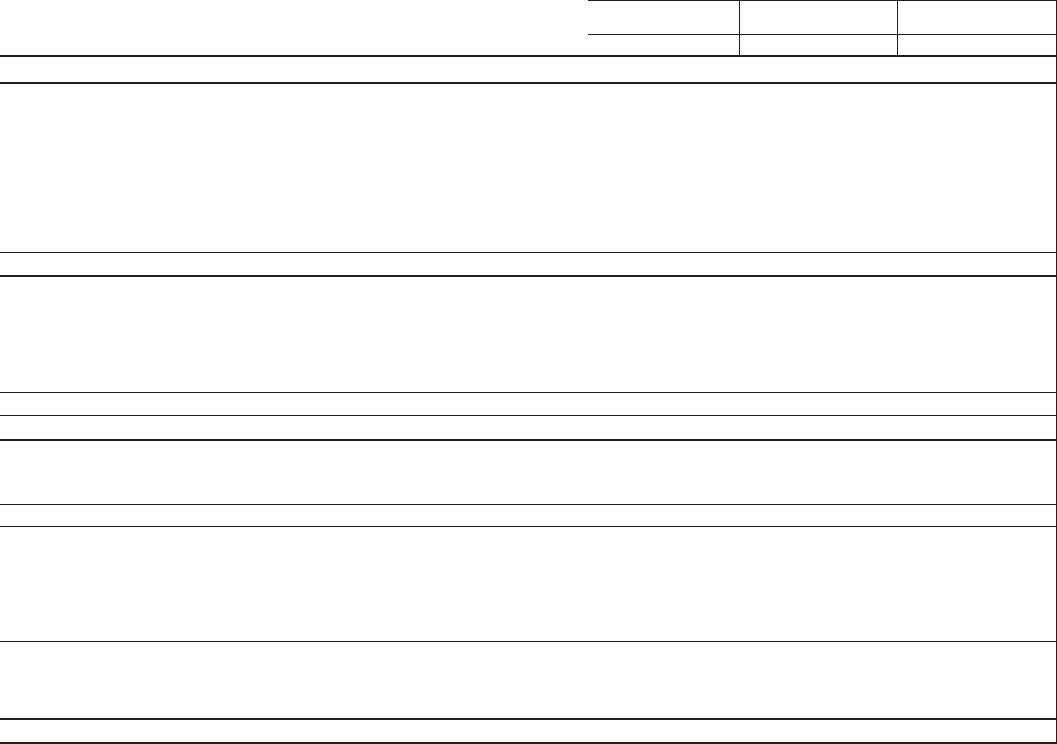

We use a measurement date of December 31 for plan assets and benefit obligations. A reconciliation of the changes in the

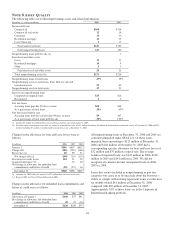

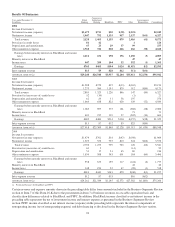

projected benefit obligation for qualified and nonqualified pension plans and postretirement benefit plans as well as the change in

plan assets for the qualified pension plan is as follows:

Qualified

Pension

Nonqualified

Pension

Postretirement

Benefits

December 31 (Measurement Date) – in millions 2006 2005 2006 2005 2006 2005

Accumulated benefit obligation at end of year $1,186 $1,232 $73 $69

Projected benefit obligation at beginning of year $1,290 $1,166 $73 $72 $270 $276

Riggs acquisition 116 1 26

Service cost 34 33 1122

Interest cost 68 65 4413 14

Amendments 21

Actuarial loss (gain) (including changes in assumptions) (47) 3 2(30) (28)

Participant contributions 77

Federal Medicare subsidy on benefits paid 2

Benefits paid (102) (90) (5) (7) (29) (28)

Projected benefit obligation at end of year $1,245 $1,290 $76 $73 $235 $270

Fair value of plan assets at beginning of year $1,627 $1,492

Riggs acquisition 107

Actual return on plan assets 221 102

Employer contribution 16 $5 $7 $20 $21

Participant contributions 77

Federal Medicare subsidy on benefits paid 2

Benefits paid (102) (90) (5) (7) (29) (28)

Fair value of plan assets at end of year $1,746 $1,627

Funded status $501 $337 $(76) $(73) $(235) $(270)

Unrecognized net actuarial loss 340 26 64

Unrecognized prior service cost (credit) (1) 1 (38)

Net amount recognized on the balance sheet $501 $676 $(76) $(46) $(235) $(244)

Amounts recognized in the Consolidated Balance Sheet consist of:

Other assets (Other liabilities) $501 $(76) $(235)

Prepaid (accrued) pension cost $676 $(46) $(244)

Additional minimum liability (23)

Intangible asset 1

Accumulated other comprehensive loss 22

Net amount recognized in the Consolidated Balance Sheet $501 $676 $(76) $(46) $(235) $(244)

Amounts recognized in accumulated other comprehensive income consist of:

Prior service cost (credit) 2 (31)

Net actuarial loss 184 28 33

Amount recognized in AOCI $186 $28 $2

The fair value of the qualified pension plan assets exceeds both the accumulated benefit obligation and the projected benefit

obligation. The nonqualified pension plan, which contains several individual plans that are accounted for together, is unfunded.

Contributions from us and, in the case of postretirement benefit plans, participant contributions cover all benefits paid under the

nonqualified pension plan and postretirement benefit plans. The benefit obligations, asset values, funded status and balance sheet

impacts are shown in the above table.

101