PNC Bank 2006 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2006 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

|

|

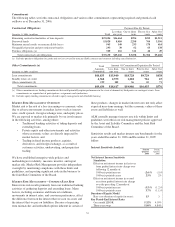

ownership position in GMAC LLC from General Motors

Corporation (“GM”) and purchased redeemable preferred

stock from GMAC LLC.

I

MPACT OF

I

NFLATION

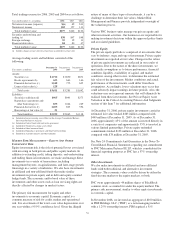

Our assets and liabilities are primarily monetary in nature.

Accordingly, future changes in prices do not affect the

obligations to pay or receive fixed and determinable amounts

of money. During periods of inflation, monetary assets lose

value in terms of purchasing power and monetary liabilities

have corresponding purchasing power gains. The concept of

purchasing power, however, is not an adequate indicator of the

effect of inflation on banks because it does not take into

account changes in interest rates, which are an important

determinant of our earnings.

F

INANCIAL

D

ERIVATIVES

We use a variety of financial derivatives as part of the overall

asset and liability risk management process to help manage

interest rate, market and credit risk inherent in our business

activities. Substantially all such instruments are used to

manage risk related to changes in interest rates. Interest rate

and total return swaps, interest rate caps and floors and futures

contracts are the primary instruments we use for interest rate

risk management.

Financial derivatives involve, to varying degrees, interest rate,

market and credit risk. For interest rate swaps and total return

swaps, options and futures contracts, only periodic cash

payments and, with respect to options, premiums, are

exchanged. Therefore, cash requirements and exposure to

credit risk are significantly less than the notional amount on

these instruments. Further information on our financial

derivatives as of December 31, 2006 and December 31, 2005,

is presented in Note 1 Accounting Policies and Note 16

Financial Derivatives in the Notes To Consolidated Financial

Statements in Part I, Item 1 of this Report.

Not all elements of interest rate, market and credit risk are

addressed through the use of financial or other derivatives,

and such instruments may be ineffective for their intended

purposes due to unanticipated market characteristics, among

other reasons.

57