Nokia 2015 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2015 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

178 NOKIA IN 2015

Notes to consolidated nancial statements continued

Business-related credit risk

The Group aims to ensure the highest possible quality in accounts receivable and loans due from customers and other third parties. The Credit

Policy, approved by the Group President and CEO, and the related procedures approved by the Group CFO, lay out the framework for the

management of the business-related credit risks. The Credit Policy and related procedures set out that credit decisions are based on credit

evaluation in each business, including credit rating for larger exposures, according to dened rating principles. Material credit exposures require

Group-level approval. Credit risks are monitored in each business and, where appropriate, mitigated with the use of letters of credit, collateral,

insurance, and the sale of selected receivables.

Credit exposure is measured as the total of accounts receivable and loans outstanding due from customers and committed credits. Accounts

receivable do not include any major concentrations of credit risk by customer. The top three customers account for approximately 9.6%,

5.9%and 3.5% (3.5%, 2.9% and 2.8% in 2014) of the Group’s accounts receivable and loans due from customers and other third parties at

December 31, 2015. The top three credit exposures by country account for approximately 19.6%, 12.1% and 10.8% (18.0%, 7.4% and 5.6%

in2014) of the Group’s accounts receivable and loans due from customers and other third parties at December 31, 2015. The 19.6% credit

exposure relates to accounts receivable in China (18.0% in 2014).

The Group has provided allowances for doubtful accounts on accounts receivable and loans due from customers and other third parties not

past due based on an analysis of debtors’ credit ratings and credit histories. The Group establishes allowances for doubtful accounts that

represent an estimate of expected losses at the end of the reporting period. All receivables and loans due from customers are considered

onanindividual basis to determine the allowances for doubtful accounts. The total of accounts receivable and loans due from customers is

EUR3 946 million (EUR 3 432 million in 2014). The gross carrying amount of accounts receivable, related to customer balances for which

valuation allowances have been recognized, is EUR 1 150 million (EUR 1 200 million in 2014). The allowances for doubtful accounts for these

accounts receivable as well as amounts expected to be uncollectible for acquired receivables are EUR 62 million (EUR 103 million in 2014).

Referto Note 22, Allowances for doubtful accounts.

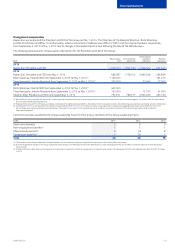

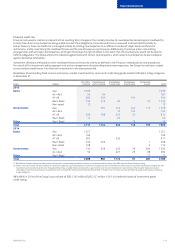

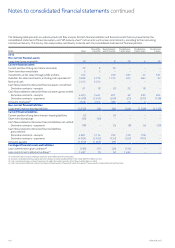

Aging of past due receivables not considered to be impaired at December 31:

EURm 2015 2014

Past due 1-30 days 25 68

Past due 31-180 days 53 42

More than 180 days 124 35

Total 202 145

Hazard risk

The Group strives to ensure that all nancial, reputation and other losses to the Group and its customers are managed through preventive

riskmanagement measures. Insurance is purchased for risks which cannot be internally managed eciently and where insurance markets oer

acceptable terms and conditions. The objective is to ensure that hazard risks, whether related to physical assets, such as buildings, intellectual

assets, such as the Nokia brand, or potential liabilities, such as product liabilities, are insured optimally taking into account both cost and

retention levels. The Group purchases both annual insurance policies for specic risks as well as multi-line and/or multi-year insurance policies

where available.