HSBC 2010 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

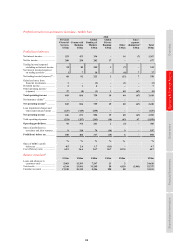

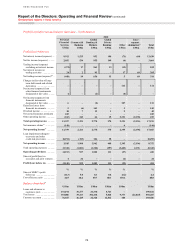

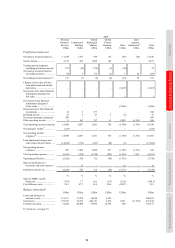

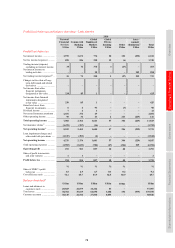

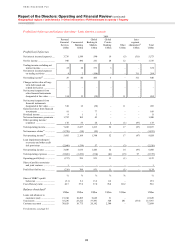

Geographical regions > Latin America

78

changes. In Mexico and Argentina, sales and

marketing initiatives supported by product and

channel enhancements resulted in an increase in

current and savings account balances. However,

the benefit was partly offset by tighter spreads on

customer accounts as a result of decreased market

interest rates in Mexico and Argentina.

Fee income fell by 7% to US$1.7bn, driven by

lower transaction volumes in credit cards and

account services in Mexico and reduced account

services income in Brazil. Regulatory restrictions in

Brazil and Mexico also reduced the fees that could

be charged for certain banking services.

Net trading income of US$733m was 23% lower

than in 2009. A decline in market volatility which

resulted in fewer trading opportunities meant that the

strong performances in Foreign Exchange and Rates

in 2009 were not repeated.

Net income on financial instruments designated

at fair value declined by 21% to US$425m,

primarily due to lower investment returns

experienced on assets held in support of the pension-

linked portfolio in Brazil and annuity products in

Argentina. An offsetting decrease was recorded in

‘Net insurance claims incurred and movement in

liabilities to policyholders’.

Gains less losses from financial investments

declined by US$93m, largely because the gains on

the sale of Visa Inc. shares in 2009 did not recur.

Net earned insurance premiums increased

marginally to US$2.1bn, driven by improved

economic conditions which resulted in higher sales

of policies in Brazil and Argentina through the

branch network and a rise in premiums in Mexico.

This, combined with repricing initiatives in

Argentina and higher contributions in the pension-

linked product in Brazil from PFS and CMB

customers, resulted in increased premiums.

Net insurance claims incurred and movement in

liabilities to policyholders of US$1.8bn declined by

9%, mainly in pension-linked products in Brazil as

lower investment gains were allocated to

policyholders. This was partly offset by an increase

related to higher premiums in Argentina and Mexico.

Loan impairment charges and other credit risk

provisions declined by 44% in 2010 to US$1.5bn. In

PFS, the reduction in loan impairment charges

reflected a significant decline in the size of the credit

card portfolio in Mexico and an improvement in its

quality as a result of repositioning the portfolio

towards higher quality customers, tighter origination

criteria and improved collection practices. Loan

impairment charges also declined in Brazil,

primarily in consumer finance portfolios including

motor vehicle finance and payroll loans, as economic

conditions improved and these portfolios were

managed down. In CMB, loan impairment charges

fell, largely in Brazil, as improved economic

conditions and better credit quality resulted in lower

specific impairment charges, while in Mexico loan

impairment charges remained broadly unchanged.

Operating expenses increased by 10% to

US$6.4bn, driven largely by inflationary pressures

and investment in infrastructure and technology

projects across the region in support of improved

operational efficiency and business growth. Staff

costs increased in Brazil and Argentina due to

union-agreed wage increases, although this was

partly offset by a decline in average headcount as

costs continued to be managed carefully. Non-staff

expenditure also rose, driven mainly by higher

marketing and advertising costs in Brazil as we

positioned ourselves in this key growth market,

and transactional taxes increased as sales grew.