HSBC 2010 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

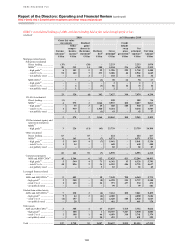

Report of the Directors: Operating and Financial Review (continued)

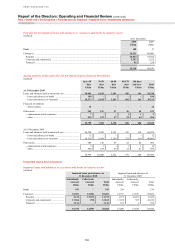

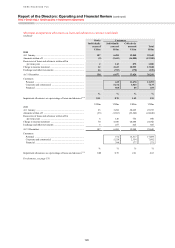

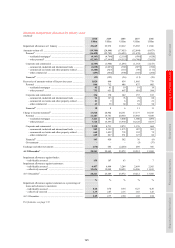

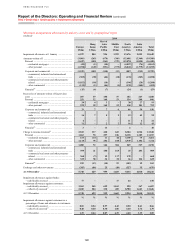

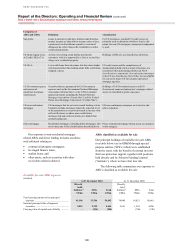

Risk > Credit risk > Securitisation exposures and other structured products

128

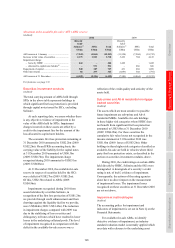

All of the derivative transactions are with HSBC

undertakings which are banking counterparties

(2009: 100%).

The credit quality of the loans and advances to

HSBC undertakings is assessed as strong/good, with

100% of the exposure being neither past due nor

impaired (2009: 100%).

The credit ratings of the financial investments

held by HSBC Holdings are within the Standard and

Poor’s (‘S&P’) ratings range of A to BBB+ (2009:

A+ to A–).

Securitisation exposures and other

structured products

(Audited)

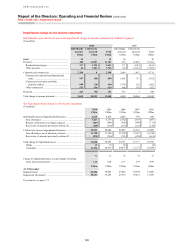

The financial impact of the recent market disruption

is lessening with net write-downs to the income

statement of nil (2009: US$1.9bn net write-downs)

and a reduction in the available-for-sale ABSs

reserve deficit by US$5.8bn to US$6.4bn.

Following the dislocation in markets which

began in 2007, there was a modest recovery in the

risk appetite of investors in 2009. However, the first

half of 2010 saw renewed uncertainty and concerns

over sovereign credit risk. As a result, the prices of

many assets perceived to be of higher risk fell. In

addition, the widespread downgrading of securitised

assets continued in the first half of 2010 as rating

agencies changed their methodologies, reducing the

appetite for securitised assets among institutions

subject to the Basel II framework.

Increased stability returned in the second half of

2010 following the interventions of the EU and the

International Monetary Fund. A modest increase in

house prices in some areas and the continued low

interest rate environment contributed to a rise in the

price of some securitised assets. As a result, the

levels of write-downs and losses on our holdings of

structured assets remained modest. Unrealised losses

in our available-for-sale reserve continued to reduce

due to increases in fair value and the principal

amortisation of ABSs as repayments were received

at par. Expectations of cash losses on available-for-

sale ABSs remained consistent with our previous

estimates.

Overview of exposure

(Audited)

Accounting policies

Our accounting policies for the classification and valuation of

financial instruments are in accordance with the requirements

of IAS 32 ‘Financial Instruments: Presentation’ and IAS 39

‘Financial Instruments: Recognition and Measurement’, as

described in Note 2 on the Financial Statements, and the use of

assumptions and estimates in respect of valuation of financial

instruments as described in Note 16 on the Financial

Statements.

This section contains information about our exposure

to the following:

• ABSs, including mortgage-backed securities

(‘MBS’s) and related collateralised debt

obligations (‘CDO’s);

• direct lending held at fair value through profit or

loss;

• monolines;

• credit derivative product companies (‘CDPC’s);

• leveraged finance transactions; and

• representations and warranties related to

mortgage sales and securitisation activities.

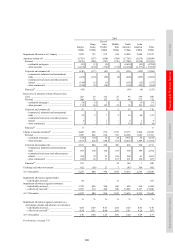

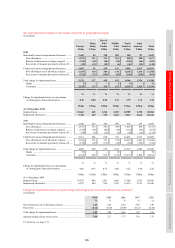

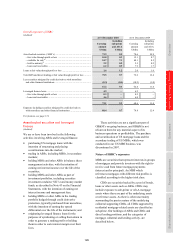

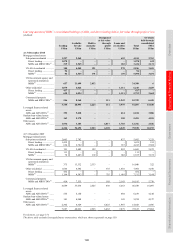

The following table summarises our exposure to

these products.