HSBC 2010 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

145

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

Market risk

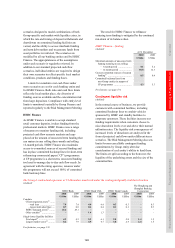

(Audited)

Market risk is the risk that movements in market

factors, including foreign exchange rates and

commodity prices, interest rates, credit spreads and

equity prices, will reduce our income or the value of

our portfolios.

We separate exposures to market risk into

trading and non-trading portfolios. Trading portfolios

include positions arising from market-making,

position-taking and others designated as marked

to market.

Non-trading portfolios include positions that

primarily arise from the interest rate management

of our retail and commercial banking assets and

liabilities, financial investments designated as

available for sale and held to maturity, and exposures

arising from our insurance operations.

Market risk arising in our insurance businesses

is discussed in ‘Risk management of insurance

operations’ on pages 155 to 171.

Monitoring and limiting market risk

exposure

(Audited)

Our objective is to manage and control market risk

exposures in order to optimise return on risk while

maintaining a market profile consistent with our

status as one of the world’s largest banking and

financial services organisations.

The management of market risk is principally

undertaken in Global Markets using risk limits

approved by the GMB. Limits are set for portfolios,

products and risk types, with market liquidity being

a primary factor in determining the level of limits

set. Group Risk, an independent unit within GMO, is

responsible for our market risk management policies

and measurement techniques. Each major operating

entity has an independent market risk management

and control function which is responsible for

measuring market risk exposures in accordance with

the policies defined by Group Risk, and monitoring

and reporting these exposures against the prescribed

limits on a daily basis.

Each operating entity is required to assess the

market risks arising on each product in its business

and to transfer them to either its local Global

Markets unit for management, or to separate books

managed under the supervision of the local Asset and

Liability Management Committee (‘ALCO’). Our

aim is to ensure that all market risks are consolidated

within operations that have the necessary skills,

tools, management and governance to manage them

professionally. In certain cases where the market

risks cannot be fully transferred, we use simulation

modelling to identify the impact of varying scenarios

on valuations and net interest income.

We employ a range of tools to monitor and limit

market risk exposures. These include sensitivity

analysis, value at risk (‘VAR’) and stress testing.

Sensitivity analysis

(Unaudited)

We use sensitivity measures to monitor the market

risk positions within each risk type, for example, the

present value of a basis point movement in interest

rates for interest rate risk. Sensitivity limits are set

for portfolios, products and risk types, with the depth

of the market being one of the principal factors in

determining the level of limits set.

Value at risk

(Audited)

VAR is a technique that estimates the potential losses

on risk positions as a result of movements in market

rates and prices over a specified time horizon and to

a given level of confidence.

The VAR models we use are based

predominantly on historical simulation. These

models derive plausible future scenarios from past

series of recorded market rates and prices, taking

into account inter-relationships between different

markets and rates such as interest rates and foreign

exchange rates. The models also incorporate the

effect of option features on the underlying

exposures.

Our historical simulation models assess

potential market movements with reference to data

from the past two years and calculate VAR to a 99%

confidence level and for a one-day holding period.

Although a valuable guide to risk, VAR should always be

viewed in the context of its limitations:

• the use of historical data as a proxy for estimating future

events may not encompass all potential events, particularly

those which are extreme in nature;

• the use of a one-day holding period assumes that all

positions can be liquidated or the risk offset in one day. This

may not fully reflect the market risk arising at times of

severe illiquidity, when a one-day holding period may be

insufficient to liquidate or hedge all positions fully;

• the use of a 99% confidence level, by definition, does not

take into account losses that might occur beyond this level

of confidence;

• VAR is calculated on the basis of exposures outstanding at

the close of business and therefore does not necessarily

reflect intra-day exposures; and

• VAR is unlikely to reflect loss potential on exposures that

only arise under significant market moves.