HSBC 2010 Annual Report Download - page 315

Download and view the complete annual report

Please find page 315 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

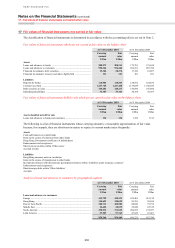

313

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

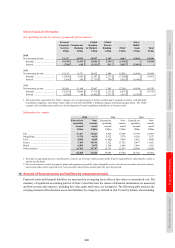

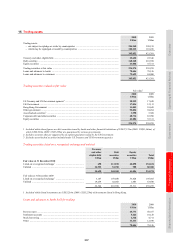

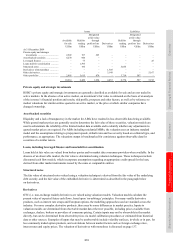

Assets Liabilities

Available

for sale

Held for

trading

Designated

at fair value

through

profit or loss Derivatives

Held for

trading

Designated

at fair value

through

profit or loss

Derivatives

US$m US$m US$m US$m US$m US$m US$m

At 31 December 2009

Private equity and strategic

investments ................................... 2,949 197 345 – – – –

Asset-backed securities .................... 4,270 944 – – – – –

Leveraged finance ............................. – 73 – – – – 25

Loans held for securitisation ............ – 1,395 – – – – –

Structured notes ................................ – 196 – – 5,055 – –

Derivatives with monolines .............. – – – 1,305 – – –

Other derivatives ............................... – – – 3,148 – – 5,167

Other portfolios ................................. 2,995 3,615 879 – 3,719 507 –

10,214 6,420 1,224 4,453 8,774 507 5,192

Private equity and strategic investments

HSBC’s private equity and strategic investments are generally classified as available for sale and are not traded in

active markets. In the absence of an active market, an investment’s fair value is estimated on the basis of an analysis

of the investee’s financial position and results, risk profile, prospects and other factors, as well as by reference to

market valuations for similar entities quoted in an active market, or the price at which similar companies have

changed ownership.

Asset-backed securities

Illiquidity and a lack of transparency in the market for ABSs have resulted in less observable data being available.

While quoted market prices are generally used to determine the fair value of these securities, valuation models are

used to substantiate the reliability of the limited market data available and to identify whether any adjustments to

quoted market prices are required. For ABSs including residential MBSs, the valuation uses an industry standard

model and the assumptions relating to prepayment speeds, default rates and loss severity based on collateral type, and

performance, as appropriate. The valuations output is benchmarked for consistency against observable data for

securities of a similar nature.

Loans, including leveraged finance and loans held for securitisation

Loans held at fair value are valued from broker quotes and/or market data consensus providers when available. In the

absence of an observable market, the fair value is determined using valuation techniques. These techniques include

discounted cash flow models, which incorporate assumptions regarding an appropriate credit spread for the loan,

derived from other market instruments issued by the same or comparable entities.

Structured notes

The fair value of structured notes valued using a valuation technique is derived from the fair value of the underlying

debt security, and the fair value of the embedded derivative is determined as described in the paragraph below

on derivatives.

Derivatives

OTC (i.e. non-exchange traded) derivatives are valued using valuation models. Valuation models calculate the

present value of expected future cash flows, based upon ‘no-arbitrage’ principles. For many vanilla derivative

products, such as interest rate swaps and European options, the modelling approaches used are standard across the

industry. For more complex derivative products, there may be some differences in market practice. Inputs to

valuation models are determined from observable market data wherever possible, including prices available from

exchanges, dealers, brokers or providers of consensus pricing. Certain inputs may not be observable in the market

directly, but can be determined from observable prices via model calibration procedures or estimated from historical

data or other sources. Examples of inputs that may be unobservable include volatility surfaces, in whole or in part, for

less commonly traded option products, and correlations between market factors such as foreign exchange rates,

interest rates and equity prices. The valuation of derivatives with monolines is discussed on page 137.