HSBC 2010 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

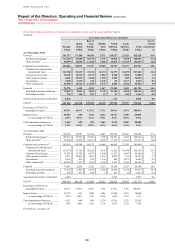

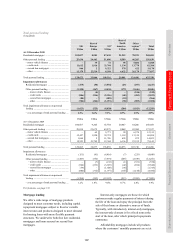

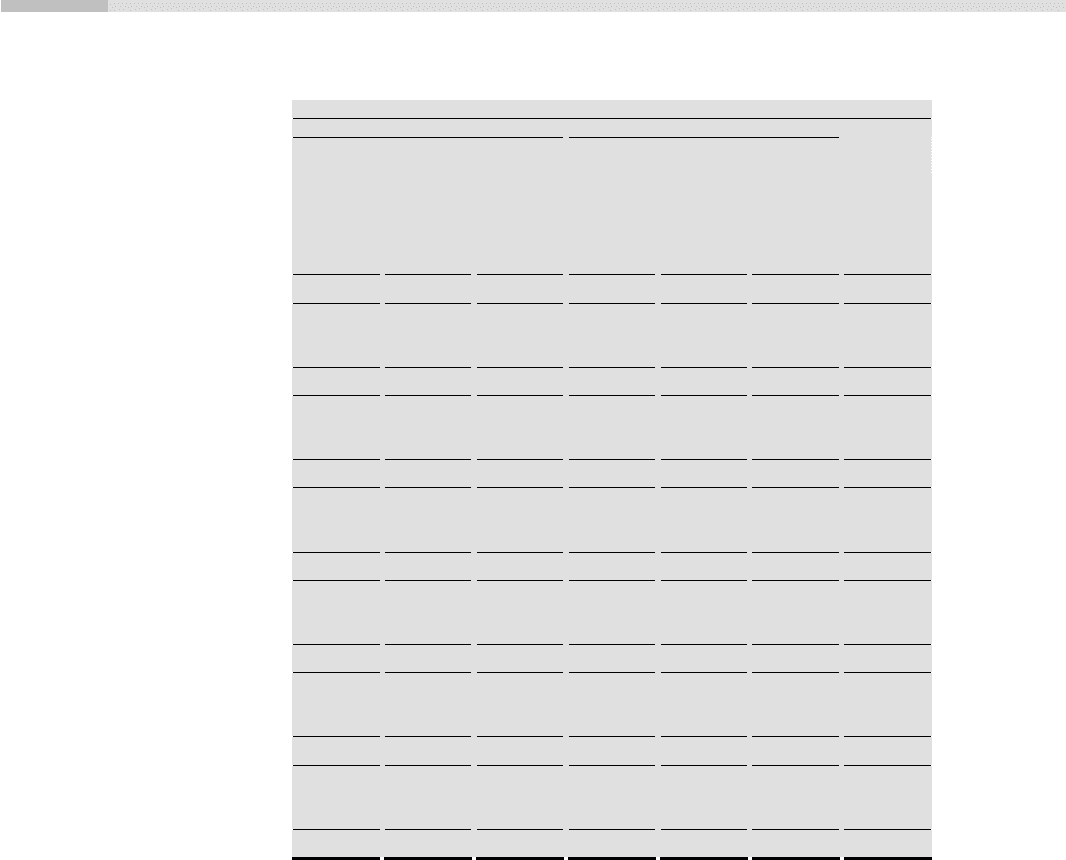

Risk > Credit risk > Areas of special interest > Wholesale lending

104

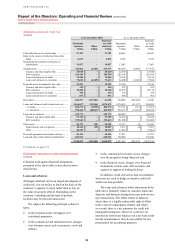

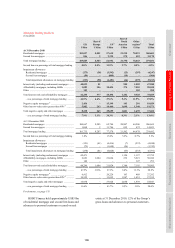

Exposures to selected eurozone countries10

(Unaudited)

At 31 December 2010

Not held for trading Held for trading

Cash and

lending to

banks11

Financial

investments

Total

balances

Net debt

securities

and loans Derivatives12

Total

balances

Total

US$bn US$bn US$bn US$bn US$bn US$bn US$bn

Belgium

Sovereign and agencies ................... 0.2 0.7 0.9 0.6 – 0.6 1.5

Banks ............................................... 5.8 0.3 6.1 1.5 1.2 2.7 8.8

6.0 1.0 7.0 2.1 1.2 3.3 10.3

Greece

Sovereign and agencies ................... – 0.3 0.3 0.8 – 0.8 1.1

Banks ............................................... – – – 0.6 – 0.6 0.6

– 0.3 0.3 1.4 – 1.4 1.7

Ireland

Sovereign and agencies ................... – 0.2 0.2 0.1 0.1 0.2 0.4

Banks ............................................... 0.2 0.5 0.7 1.1 0.4 1.5 2.2

0.2 0.7 0.9 1.2 0.5 1.7 2.6

Italy

Sovereign and agencies ................... – 1.7 1.7 1.8 – 1.8 3.5

Banks ............................................... 1.9 0.4 2.3 0.2 – 0.2 2.5

1.9 2.1 4.0 2.0 – 2.0 6.0

Portugal

Sovereign and agencies ................... – 0.1 0.1 –– – 0.1

Banks ............................................... 0.3 0.1 0.4 0.1 – 0.1 0.5

0.3 0.2 0.5 0.1 – 0.1 0.6

Spain

Sovereign and agencies ................... 0.1 0.9 1.0 0.7 0.1 0.8 1.8

Banks ............................................... 0.8 0.2 1.0 1.4 – 1.4 2.4

0.9 1.1 2.0 2.1 0.1 2.2 4.2

Total

Sovereign and agencies ................... 0.3 3.9 4.2 4.0 0.2 4.2 8.4

Banks ............................................... 9.0 1.5 10.5 4.9 1.6 6.5 17.0

9.3 5.4 14.7 8.9 1.8 10.7 25.4

For footnotes, see page 174.

under pressure, but for its specific political situation.

Rating agencies downgraded the debt of a number

of eurozone countries during 2010 and put some

on review for possible downgrades. While the

ECB continues to provide broad access to liquidity

support for eurozone sovereign borrowers and banks,

the availability of longer-term fiscal support from

the EU for sovereigns is less certain and may lead

to debt restructuring and increased private sector

participation.

The eurozone as a whole retained substantial

economic and financial strength despite the stresses

from the financial crisis. However, concerns

remained over the refinancing risks for sovereign

borrowers and banks posed by the problems with

market liquidity and the uncertainty surrounding

support arrangements in the longer term. Eurozone

policymakers have created two major facilities to

counter short-term financing problems, the European

Financial Stability Facility and the European

Financial Stability Mechanism. This has been

viewed as a positive development by the market

and rating agencies, though implementation awaits

disclosure of further details by the policymakers.

We expect the ECB and eurozone countries will

focus in 2011 on resolving intra-eurozone

imbalances, rebuilding public finances, improving

fiscal discipline, strengthening the banking system

and managing cross-border risk.

We have closely managed our exposure to

sovereign debt during 2010. At the end of the year,

our exposure to the sovereign debt of Belgium,

Greece, Ireland, Italy, Portugal and Spain was

US$8.4bn and the overall quality of the portfolio was

strong with most in-country and cross-border limits

extended to countries with high-grade internal credit

risk ratings. We regularly update our assessment of

higher risk countries and adjust our risk appetite to

reflect such changes.