HSBC 2010 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

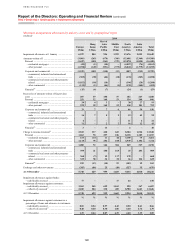

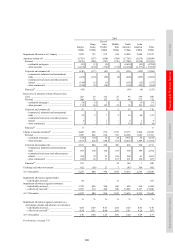

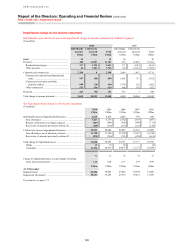

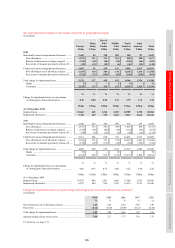

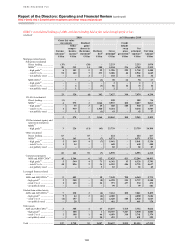

Risk > Credit risk > Securitisation exposures and other structured products

132

pools and models their projected future cash flows.

The estimated future cash flows of the securities

are assessed at the specific financial asset level to

determine whether any of them are unlikely to be

recovered as a result of loss events occurring on or

before the reporting date.

The principal assumptions and inputs to the

models are typically the delinquency status of the

underlying loans, the probability of delinquent

loans progressing to default, the prepayment

profiles of the underlying assets and the loss

severity in the event of default. However, the

models utilise other variables relevant to specific

classes of collateral to forecast future defaults

and recovery rates. Management uses externally

available data and applies judgement when

determining the appropriate assumptions in respect

of these factors. HSBC uses a modelling approach

which incorporates historically observed

progression rates to default, to determine if the

decline in aggregate projected cash flows from

the underlying collateral will lead to a shortfall in

contractual cash flows. In such cases the security

is considered to be impaired.

In respect of CDOs, expected future cash

flows for the underlying collateral are assessed to

determine whether there is likely to be a shortfall

in the contractual cash flows of the CDO.

When a security benefits from a contract

provided by a monoline insurer that insures

payments of principal and interest, the expected

recovery on the contract is assessed in determining

the total expected credit support available to the

ABS.

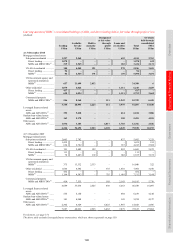

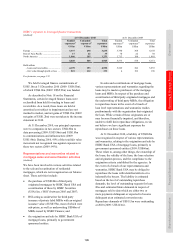

Impairment and cash loss projections

(Unaudited)

At 31 December 2009, management undertook

an analysis to estimate further potential

impairments and expected cash losses on the

available-for-sale ABS portfolio. This exercise

comprised a shift of projections of future loss

severities, default rates and prepayment rates.

The results of the analysis indicated that further

impairment charges of some US$1.1bn and

expected cash losses of some US$450m could

arise over the next two to three years.

At 31 December 2010, management

re-performed the stress test. After taking into

account the cash losses experienced during 2010,

the remaining cash loss projections of US$250m

were consistent with those as at 31 December 2009.

However, the impairment charge projections

showed an additional charge of US$300m arising

over the next two years in relation to the SICs, after

taking into account the impairments recognised in

2010, resulting in future impairment charges of

US$950m, including the US$300m relating to the

SICs. This additional charge reflects where the

accounting impairments will exceed the carrying

amount of the capital notes held by third parties.

For the purposes of identifying impairment at

the reporting date, the future projected cash flows

reflect the effect of loss events that have occurred

at or prior to the reporting date. For the purposes of

performing stress tests to estimate potential future

impairment charges, the projected future cash flows

reflect additional assumptions about future loss

events after the balance sheet date.

This analysis makes assumptions in respect

of the future behaviour of loss severities, default

rates and prepayment rates. Movements in the

parameters are not independent of each other. For

example, increased default rates and increased loss

severities, which would imply greater impairments,

generally arise under economic conditions that give

rise to reduced levels of prepayment, reducing the

potential for impairment charges. Conversely,

economic conditions which increase the rates of

prepayment are generally associated with reduced

default rates and decreased loss severities.

At 31 December 2010, the incurred and

projected impairment charges, measured in

accordance with accounting requirements,

significantly exceeded the expected cash losses on

the securities. Over the lives of the available-for-

sale ABSs the cumulative impairment charges will

converge towards the level of cash losses. In

respect of the SICs, in particular, the capital notes

held by third parties are expected to absorb the cash

losses arising in the vehicles.