HSBC 2010 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

173

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

investment objectives of both HSBC and, where

relevant and appropriate, the trustees are:

• to limit the risk of the assets failing to meet the

liabilities of the plans over the long-term; and

• to maximise returns consistent with an

acceptable level of risk so as to control the

long-term costs of the defined benefit plans.

In pursuit of these long-term objectives, a

benchmark is established for the allocation of the

defined benefit plan assets between asset classes.

In addition, each permitted asset class has its own

benchmarks, such as stock market or property

valuation indices and, where relevant, desired levels

of out-performance. The benchmarks are reviewed

at least triennially within 18 months of the date at

which an actuarial valuation is made, or more

frequently if required by local legislation or

circumstances. The process generally involves an

extensive asset and liability review.

Ultimate responsibility for investment strategy

rests with either the trustees or, in certain

circumstances, a Management Committee. The

degree of independence of the trustees from HSBC

varies in different jurisdictions. For example, the

principal plan, which accounts for approximately

70% of the obligations of our defined benefit

pension plans, is overseen by a corporate trustee who

regularly monitors the market risks inherent in the

scheme.

The principal plan holds a diversified portfolio

of investments to meet future cash flow liabilities

arising from accrued benefits as they fall due to be

paid. The trustee of the principal plan is required to

produce a written Statement of Investment Principles

which governs decision-making about how

investments are made.

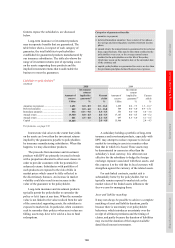

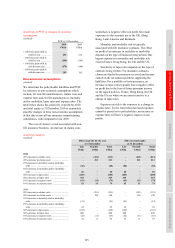

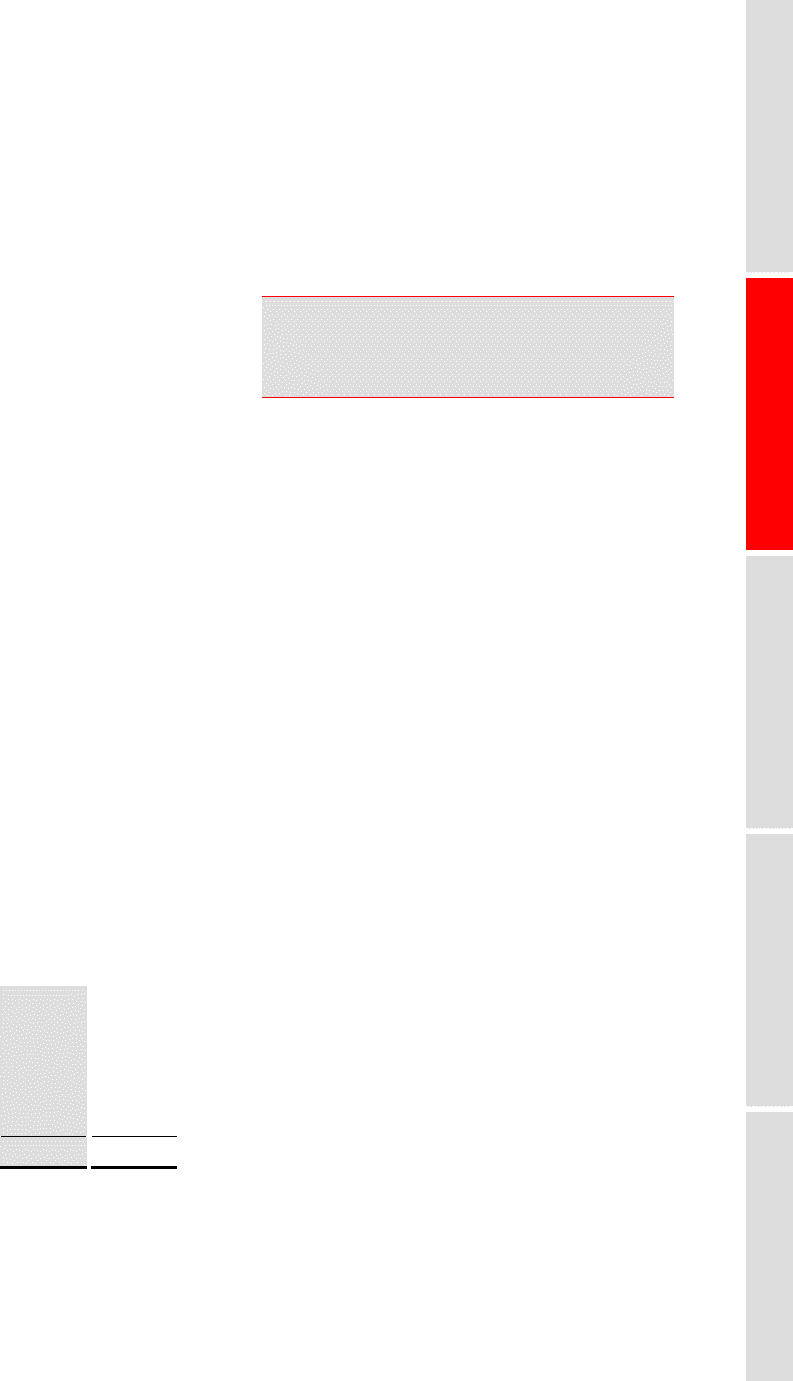

The DBS principal plan – asset allocation

2010 2006

% %

Equities ........................................ 15.5 15.0

Bonds ........................................... 56.5 50.0

Alternative assets93 ...................... 10.5 10.0

Property ........................................ 9.0 10.0

Cash ............................................. 8.5 15.0

100.0 100.0

For footnote, see page 174.

In 2006, HSBC and the trustee of the principal

plan agreed to change the investment strategy in

order to reduce the investment risk. The target asset

allocations for this strategy at that time and as

revised in 2010 are shown above. The strategy is to

hold the majority of assets in bonds, with the

remainder in a more diverse range of investments,

and includes a commitment to undertake a

programme of swap arrangements (see Note 45 on

the Financial Statements) by which the principal

plan makes LIBOR-related interest payments in

exchange for the receipt of cash flows which are

based on projected future benefit payments to be

made from the principal plan.

Sustainability risk

(Unaudited)

Assessing the environmental and social

impacts of providing finance to our

customers has been firmly embedded into

our overall risk management processes.

Sustainability risks arise from the provision of

financial services to companies or projects which run

counter to the needs of sustainable development; in

effect this risk arises when the environmental and

social effects outweigh economic benefits. Within

GMO, a separate function, Group Corporate

Sustainability, is mandated to manage these risks

globally working through local offices as

appropriate. Sustainability Risk Managers have

regional or national responsibilities for advising on

and managing environmental and social risks.

Group Corporate Sustainability’s risk

management responsibilities include:

• formulating sustainability risk policies. This

includes oversight of our sustainability risk

standards, management of the Equator

Principles for project finance lending, and

sector-based sustainability policies covering

those sectors with high environmental or social

impacts (forestry, freshwater infrastructure,

chemicals, energy, mining and metals, and

defence-related lending); undertaking an

independent review of transactions where

sustainability risks are assessed to be high, and

supporting our operating companies to assess

similar risks of a lower magnitude;

• building and implementing systems-based

processes to ensure consistent application of

policies, reduce the costs of sustainability risk

reviews and capture management information to

measure and report on the effect of our lending

and investment activities on sustainable

development; and

• providing training and capacity building within

our operating companies to ensure sustainability

risks are identified and mitigated consistently to

either our own standards, international standards

or local regulations, whichever is higher.