HSBC 2010 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

115

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

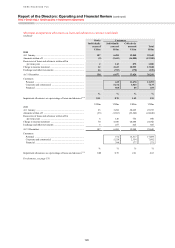

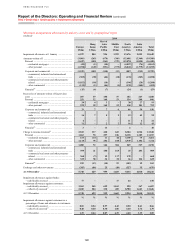

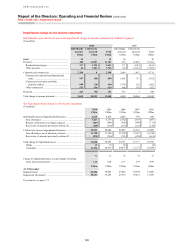

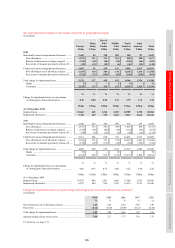

Quality classification definitions

• ‘Strong’: exposures demonstrate a strong capacity to meet

financial commitments, with negligible or low probability of

default and/or low levels of expected loss. Retail accounts

operate within product parameters and only exceptionally

show any period of delinquency.

• ‘Good’: exposures require closer monitoring and demonstrate

a good capacity to meet financial commitments, with low

default risk. Retail accounts typically show only short periods

of delinquency, with any losses expected to be minimal

following the adoption of recovery processes.

• ‘Satisfactory’: exposures require closer monitoring and

demonstrate an average to fair capacity to meet financial

commitments, with moderate default risk. Retail accounts

typically show only short periods of delinquency, with any

losses expected to be minor following the adoption of recovery

processes.

• ‘Sub-standard’: exposures require varying degrees of special

attention and default risk is of greater concern. Retail portfolio

segments show longer delinquency periods of generally up to

90 days past due and/or expected losses are higher due to a

reduced ability to mitigate these through security realisation or

other recovery processes.

• ‘Impaired’: exposures have been assessed, individually or

collectively, as impaired.

The Customer Risk Rating (‘CRR’) 10-grade scale

above summarises a more granular underlying

23-grade scale (2009: 22-grade scale) of obligor

probability of default (‘PD’). The 23-grade scale was

introduced in September 2010 following the

harmonisation of PDs for three asset classes (banks,

sovereigns and corporates) into one scale which

required an additional PD band. All distinct HSBC

customers are rated using the 10 or 23-grade scale,

depending on the degree of sophistication of the

Basel II approach adopted for the exposure.

The Expected Loss (‘EL’) 10-grade scale for

retail business summarises a more granular

underlying EL scale for these customer segments;

this combines obligor and facility/product risk

factors in a composite measure.

For debt securities and certain other financial

instruments, external ratings have been aligned to the

five quality classifications. The ratings of Standard

and Poor’s are cited, with those of other agencies

being treated equivalently. Debt securities with

short-term issue ratings are reported against the

long-term rating of the issuer of those securities. If

major rating agencies have different ratings for the

same debt securities, a prudent rating selection is

made in line with regulatory requirements.

Additional credit quality information in respect

of our consolidated holdings of ABSs is provided on

pages 134 and 135.

For the purpose of the following disclosure,

retail loans which are past due up to 89 days and are

not otherwise classified as EL9 or EL10, are not

disclosed within the EL grade to which they relate,

but are separately classified as past due but not

impaired.

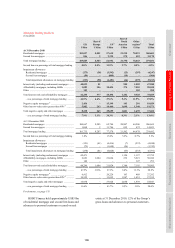

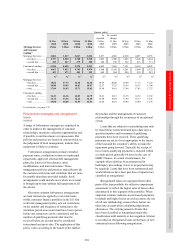

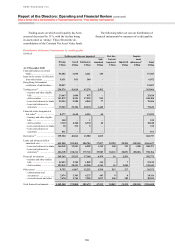

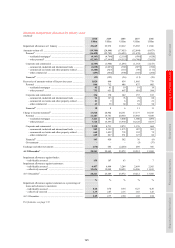

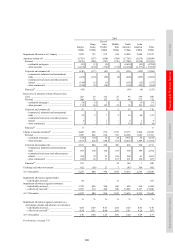

Financial instruments by credit quality

2010 compared with 2009

Financial instruments on which credit quality has

been assessed increased by 4% to US$2,297bn due

to strong growth in lending, mainly in Asia.

At December 2010, US$1,550bn or 67% was

classified as ‘strong’ in line with the end of 2009,

reflecting the continued actions by management to

mitigate the Group’s exposure to credit risk. The

proportion of financial instruments classified as

‘good’ and ‘satisfactory’ were broadly unchanged at

16% and 12% respectively. The proportion of ‘sub-

standard’ financial instruments was 2%.

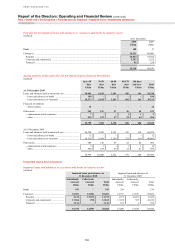

Loans and advances on which credit quality has

been assessed increased by 8% to US$1,167bn,

driven by growth in commercial and personal

lending in Asia as generally economic conditions

improved, while loans and advances to banks also

rose. The growth was in balances classified as

‘strong’ and ‘good’, while balances classified as

‘sub-standard’ and ‘past due but not impaired’

declined.

Derivative assets on which credit quality has

been assessed grew by 4% to US$261bn from

31 December 2009, with growth in balances being

classified as ‘strong’. The increase was mainly in

interest rate derivatives, reflecting a downward shift

in yield curves.

At 31 December 2010, financial investments

on which credit quality has been assessed increased

by 9% compared with the end of 2009, to

US$393bn. Substantially all this growth was in

assets classified as ‘strong’, reflecting increased

investment of excess liquidity into low-risk

government issued or government guaranteed bonds.