HSBC 2010 Annual Report Download - page 172

Download and view the complete annual report

Please find page 172 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

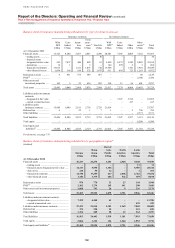

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Risk management of insurance operations > PVIF insurance business / Economic assumptions / Non-economic assumptions

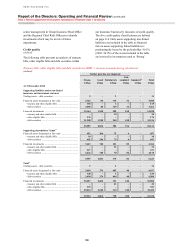

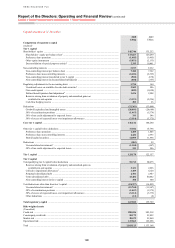

170

Present value of in-force long-term

insurance business

(Audited)

Our life insurance business is accounted for using

the embedded value approach which, inter alia,

provides a comprehensive risk and valuation

framework. The present value of our in-force long-

term (‘PVIF’) asset at 31 December 2010 was

US$3.4bn (2009: US$2.8bn), representing the

present value of the shareholders’ interest in the

profits expected to emerge from the book of in-force

policies at that date.

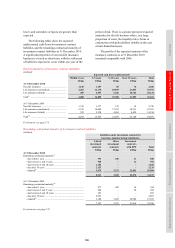

The following table shows the movements

recorded during the year in respect of total equity

and PVIF of insurance operations:

Movements in total equity and PVIF of insurance operations

(Audited)

2010 2009

Total

equity

PVIF

included in

total equity

Total

equity

PVIF

included in

total equity

US$m US$m US$m US$m

At 1 January .................................................................................. 8,580 2,780 7,577 2,033

Value of new business written during the year91 .......................... 737 737 600 600

Movements arising from in-force business:

– expected return ...................................................................... (85) (85) (123) (123)

– experience variances92 ........................................................... 20 20 (44) (44)

– change in operating assumptions .......................................... 58 58 48 48

Investment return variances .......................................................... 19 19 16 16

Changes in investment assumptions ............................................. (38) (38) 19 19

Return on net assets ...................................................................... 858 – 522 –

Exchange differences and other ................................................... (222) (51) (83) 231

Capital transactions ...................................................................... (149) – 48 –

At 31 December ............................................................................ 9,778 3,440 8,580 2,780

For footnotes, see page 174.

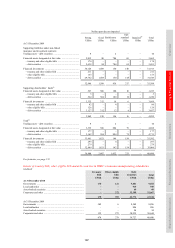

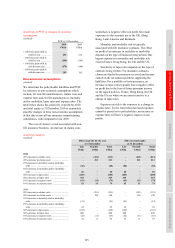

Key assumptions used in the computation of PVIF for main life insurance operations

2010 2009

UK Hong Kong France UK Hong Kong France

% % % % % %

Risk free rate .......................................................... 3.46 3.10 3.15 3.50 2.58 3.46

Risk discount rate .................................................. 7.00 11.00 8.00 7.00 11.00 8.00

Expenses inflation ................................................. 3.76 3.00 2.00 3.50 3.00 2.00

The calculation of the PVIF is based upon

assumptions that take into account risk and

uncertainty. To project these cash flows, a variety of

assumptions regarding future experience is made by

each insurance operation which reflects local market

conditions and management’s judgement of local

future trends. Some of the Group’s insurance

operations incorporate risk margins separately in the

projection assumptions for each product, while

others incorporate risk margins into the overall

discount rate. Both factors are reflected in the wide

range of risk discount rates applied.

Economic assumptions

(Audited)

The following table shows the effect on the PVIF of

reasonably possible changes in the main economic

assumptions, namely the risk-free and risk discount

rates, across all insurance manufacturing

subsidiaries.

Due to certain characteristics of the contracts,

the relationships may be non-linear and the results

of the stress-testing should not be extrapolated to

higher levels of stress. In calculating the various

scenarios, all assumptions are held stable except

when testing the effect of the shift in the risk-free

rate, when resultant changes to investment returns,

risk discount rates and bonus rates are also

incorporated. The sensitivities shown are before

actions that could be taken by management to

mitigate effects and before resultant changes in

policyholder behaviour.