HSBC 2010 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Market risk > Trading and non-trading portfolios / Structural FX exposures / Sensitivity of NII

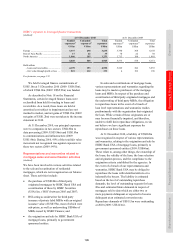

148

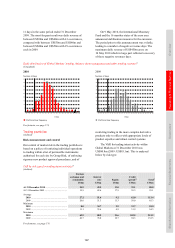

The VAR for overall trading intent activity as

at 31 December 2010 was lower than at the end of

2009, because of reduced volatility in various asset

classes. However, the wider band in VAR observed

in 2010 was driven by an increase in client-led

transactions and reduced portfolio diversification

benefit, which resulted in occasionally higher VAR

utilisation, as reflected in the above summary

statistics.

Credit spread risk

(Audited)

The risk associated with movements in credit

spreads is primarily managed through sensitivity

limits, stress testing and VAR for those portfolios

on which it is calculated.

At 31 December 2010, the Group credit spread

VAR was US$41.9m (2009: US$72.7m). The decrease

arose from the effect of volatile credit spread

scenarios rolling off from the VAR calculation.

Credit spread risk also arises on credit derivative

transactions entered into by Global Banking in

order to manage the risk concentrations within our

corporate loan portfolio and so enhance capital

efficiency. The mark-to-market of these transactions

is reflected in the income statement. At 31 December

2010, the credit VAR on the credit derivatives

transactions entered into by Global Banking was

US$12.3m (2009: US$13.8m).

Gap risk

Even for transactions that are structured to render

the risk to HSBC negligible under a wide range of

market conditions or events, there exists a remote

possibility that a significant gap event could lead

to loss. A gap event could arise from a significant

change in market price with no accompanying

trading opportunity, with the result that the threshold

is breached beyond which the risk profile changes

from no risk to full exposure to the underlying

structure. Such movements may occur, for example,

when, in reaction to an adverse event or unexpected

news announcement, the market for a specific

investment becomes illiquid, making hedging

impossible.

Given their characteristics, these transactions

make little or no contribution to VAR or to

traditional market risk sensitivity measures. We

capture their risks within our stress testing scenarios

and monitor gap risk on an ongoing basis. We

regularly consider the probability of gap loss, and

fair value adjustments are booked against this risk.

We did not incur any material gap loss in respect of

such transactions in 2010.

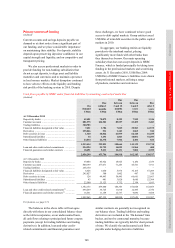

Non-trading portfolios

(Audited)

Risk measurement and control

The principal objective of market risk management

of non-trading portfolios is to optimise net interest

income. Interest rate risk in non-trading portfolios

arises principally from mismatches between the

future yield on assets and their funding cost, as a

result of interest rate changes. Analysis of this risk

is complicated by having to make assumptions on

embedded optionality within certain product areas

such as the incidence of mortgage prepayments,

and from behavioural assumptions regarding

the economic duration of liabilities which are

contractually repayable on demand such as current

accounts.

Our control of market risk in the non-trading

portfolios is based on transferring the risks to the

books managed by Global Markets or the local

ALCO. The net exposure is typically managed

through the use of interest rate swaps within agreed

limits. The VAR for these portfolios is included

within the Group VAR (see ‘Value at risk of the

trading and non-trading portfolios’ on page 146).

Credit spread risk

The risk associated with movements in credit

spreads is primarily managed through sensitivity

limits, stress testing, and VAR for those portfolios

where VAR is calculated. We have introduced credit

spread as a separate risk type within our VAR

models on a global basis. The VAR shows the effect

on income from a one-day movement in credit

spreads over a two-year period, calculated to a 99%

confidence interval.

At 31 December 2010, the sensitivity of equity

capital to the effect of movements in credit spreads,

based on credit spread VAR, on our available-

for-sale debt securities was US$264m (2009:

US$535m). After including the gross exposure for

the SICs consolidated within our balance sheet, this

exposure rose to US$299m (2009: US$549m). This

sensitivity is calculated before taking into account

losses which would have been absorbed by the

capital note holders. At 31 December 2010, the

capital note holders can absorb the first US$2.2bn

(2009: US$2.2bn) of any losses incurred by the SICs

before we incur any equity losses.

The decrease in this sensitivity at 31 December

2010 compared with 31 December 2009 can be

explained by the effect of lower volatility in credit

spread scenarios observed during 2010.