HSBC 2010 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Risk > Credit risk > Securitisation exposures and other structured products

138

Credit risk adjustments for monolines

• For highly-rated monolines, the standard credit risk

adjustment methodology (as described on page 312) applies,

with the exception that the future exposure profile is

deemed to be constant (equal to the current market value)

over the weighted average life of the referenced security,

and the credit risk adjustment cannot fall below 10% of the

mark-to-market exposure.

• In respect of monolines, where default has either occurred

or there is a strong possibility of default in the near term,

the adjustment is determined based on the estimated

probabilities of various potential scenarios, and the

estimated recovery in each case.

• For other monoline exposures, the credit risk adjustment

follows the methodology for highly-rated monolines,

adjusted to include the probability of a claim arising in

respect of the referenced security, and applies implied

probabilities of default where the likelihood of a claim is

believed to be high.

As described above, HSBC’s monoline credit

risk adjustment calculation utilises a range of

approaches dependent upon the credit quality of

the monoline. The net impact of utilising the

methodology adopted for ‘highly-rated’ monolines

across all monolines would be a reduction in credit

risk adjustment of US$94m. The net impact of

utilising a methodology based on credit default swap

spreads would be an increase in credit risk

adjustment of US$8m.

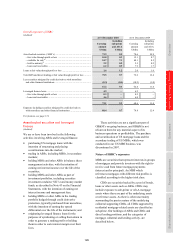

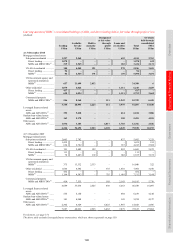

At 31 December 2010, US$1.4bn (2009:

US$2.6bn) notional value of securities referenced by

monoline CDS transactions with a market value of

US$1.0bn (2009: US$1.9bn) were held in the loans

and receivables category, having been included in

the reclassification of financial assets described in

Note 18 on the Financial Statements. At the date of

reclassification, the market value of the remaining

assets was US$1.2bn. The reclassification resulted in

an accounting asymmetry between the CDSs, which

continue to be held at fair value through profit and

loss, and the reclassified securities, which are

accounted for on an amortised cost basis. If the

reclassifications had not occurred, the impact on the

income statement for 2010 would have been

a decrease in profit of US$3m (2009: increase in

profit of US$5m). This amount represents the

difference between the increase in market value of

the securities during 2010 and the accretion

recognised under the amortised cost method in 2010.

HSBC’s exposure to direct lending and

irrevocable commitments to lend to monolines

HSBC had no liquidity facilities to monolines at

31 December 2010 (2009: minimal).

HSBC’s exposure to debt securities which benefit

from guarantees provided by monolines

Within both the trading and available-for-sale

portfolios, we hold bonds that are ‘wrapped’ with

a credit enhancement from a monoline. As the

bonds are traded explicitly with the benefit of this

enhancement, any deterioration in the credit profile

of the monoline is reflected in market prices and,

therefore, in the carrying amount of these securities

at 31 December 2010. For wrapped bonds held in

our trading portfolio, the mark-to-market movement

has been reflected through the income statement. For

wrapped bonds held in the available-for-sale portfolio,

the mark-to-market movement is reflected in equity

unless there is objective evidence of impairment, in

which case the impairment loss is reflected in the

income statement. No wrapped bonds were included

in the reclassification of financial assets described in

Note 18 on the Financial Statements.

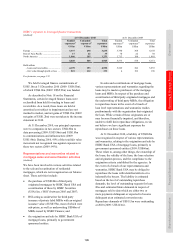

HSBC’s exposure to Credit Derivative

Product Companies

(Audited)

Credit Derivative Product Companies (‘CDPC’s)

are independent companies that specialise in selling

credit default protection on corporate exposures.

OTC derivative exposure to CDPCs became a focus

during the second half of 2008 as the spreads

widened, but these exposures reduced during 2009

as the spreads tightened again. At 31 December

2010, HSBC had purchased from CDPCs credit

protection with a notional value of US$4.9bn (2009:

US$5.0bn) which had a fair value of US$0.2bn

(2009: US$0.3bn), against which a credit risk

adjustment (a provision) of US$0.1bn (2009:

US$0.1bn) was held. At 31 December 2010, none of

the exposure was to CDPCs with investment grade

ratings (2009: 83%). The deterioration reflects rating

downgrades and withdrawals during 2010.

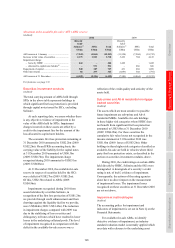

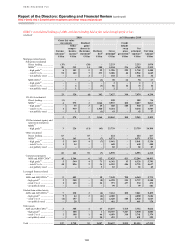

Leveraged finance transactions

(Audited)

Leveraged finance transactions include sub-

investment grade acquisition or event-driven

financing. The following table shows our exposure

to leveraged finance transactions arising from

primary transactions. Our additional exposure to

leveraged finance loans through holdings of ABSs

from our trading and investment activities is shown

in the table on page 133.