HSBC 2010 Annual Report Download - page 253

Download and view the complete annual report

Please find page 253 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

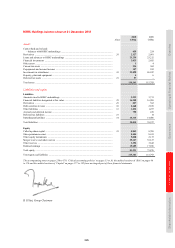

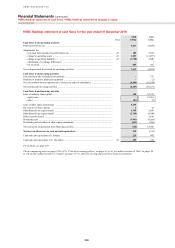

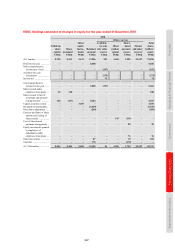

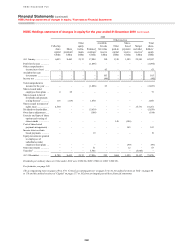

251

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

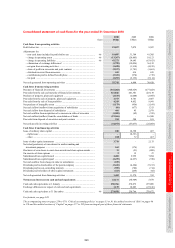

Disclosures relating to HSBC’s securitisation activities and structured products have been included in the audited

section of ‘Report of the Directors: Risk’ on pages 86 to 176.

In accordance with HSBC’s policy to provide meaningful disclosures that help investors and other stakeholders

understand the Group’s performance, financial position and changes thereto, the information provided in the

Notes on the Financial Statements and the Report of the Directors goes beyond the minimum levels required by

accounting standards, statutory and regulatory requirements and listing rules. In particular, HSBC has adopted

the British Bankers’ Association Code for Financial Reporting Disclosure (‘the BBA Code’). The BBA Code

aims to increase the quality and comparability of banks’ disclosures and sets out five disclosure principles

together with supporting guidance. In line with the principles of the BBA Code, HSBC assesses good practice

recommendations issued from time to time by relevant regulators and standard setters and will assess the

applicability and relevance of such guidance, enhancing disclosures where appropriate.

In publishing the parent company financial statements here together with the Group financial statements, HSBC

Holdings has taken advantage of the exemption in section 408(3) of the Companies Act 2006 not to present its

individual income statement and related notes that form a part of these financial statements.

HSBC’s consolidated financial statements are presented in US dollars which is also HSBC Holdings’ functional

currency. HSBC Holdings’ functional currency is the US dollar because the US dollar and currencies linked to

it are the most significant currencies relevant to the underlying transactions, events and conditions of its

subsidiaries, as well as representing a significant proportion of its funds generated from financing activities.

HSBC uses the US dollar as its presentation currency in its consolidated financial statements because the US

dollar and currencies linked to it form the major currency bloc in which HSBC transacts and funds its business.

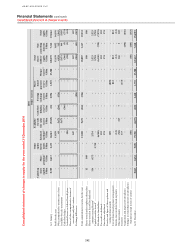

(d) Comparative information

As required by US public company reporting requirements, these consolidated financial statements include

two years of comparative information for the consolidated income statement, consolidated statement of

comprehensive income, consolidated statement of cash flows, consolidated statement of changes in equity

and related Notes on the Financial Statements.

(e) Use of estimates and assumptions

The preparation of financial information requires the use of estimates and assumptions about future conditions.

The use of available information and the application of judgement are inherent in the formation of estimates;

actual results in the future may differ from estimates upon which financial information is prepared. Management

believes that HSBC’s critical accounting policies where judgement is necessarily applied are those which relate

to impairment of loans and advances, goodwill impairment, the valuation of financial instruments, the

impairment of available-for-sale financial assets and deferred tax assets (see ‘Critical Accounting Policies’

on pages 33 to 36, which form an integral part of these financial statements).

Further information about key assumptions concerning the future, and other key sources of estimation

uncertainty, are set out in the Notes on the Financial Statements.

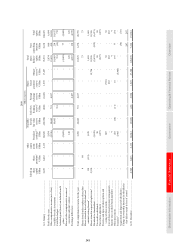

(f) Consolidation

The consolidated financial statements of HSBC comprise the financial statements of HSBC Holdings and its

subsidiaries made up to 31 December, with the exception of the banking and insurance subsidiaries of HSBC

Bank Argentina, whose financial statements are made up to 30 June annually to comply with local regulations.

Accordingly, HSBC uses their audited interim financial statements, drawn up to 31 December annually.

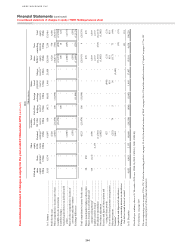

Subsidiaries are consolidated from the date that HSBC gains control. The acquisition method of accounting is

used when subsidiaries are acquired by HSBC. The cost of an acquisition is measured at the fair value of the

consideration, including contingent consideration, given at the date of exchange. Acquisition-related costs are

recognised as an expense in the income statement in the period in which they are incurred. The acquired

identifiable assets, liabilities and contingent liabilities are measured at their fair values at the date of acquisition.

Goodwill is measured as the excess of the aggregate of the consideration transferred, the amount of non-

controlling interest and the fair value of HSBC’s previously held equity interest, if any, over the net of the

amounts of the identifiable assets acquired and the liabilities assumed. The amount of non-controlling interest is

measured either at fair value or at the non-controlling interest’s proportionate share of the acquiree’s identifiable