HSBC 2010 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

113

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

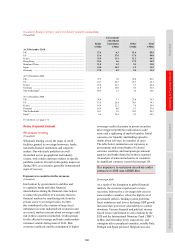

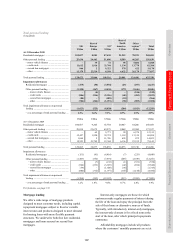

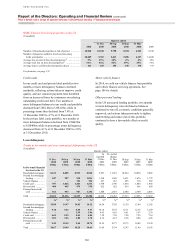

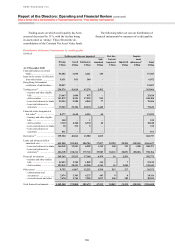

Quarter ended

31 Dec

2010

30 Sep

2010

30 Jun

2010

31 Mar

2010

As

reported

31 Dec

2009

Ex. period

change

31 Dec

2009

30 Sep

2009

30 Jun

2009

31 Mar

2009

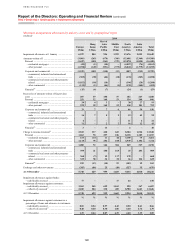

US$m US$m US$m US$m US$m US$m US$m US$m US$m Mortgage Services

and Consumer

Lending24

Mortgage Services: .... 3,002 3,117 3,067 3,236 3,477 4,456 4,250 4,257 4,535

– first lien ............... 2,757 2,850 2,788 2,928 3,093 3,900 3,688 3,642 3,824

– second lien .......... 245 267 279 308 384 556 562 615 711

Consumer Lending: ... 5,284 5,495 5,278 5,493 6,022 7,445 7,131 6,514 6,203

– first lien ............... 4,861 5,022 4,795 4,970 5,380 6,541 6,241 5,640 5,322

– second lien .......... 423 473 483 523 642 904 890 874 881

%23 %23 %23 %23 %

23 %

23 %

23 %23 %23

Mortgage Services:

– first lien ............... 18.02 17.73 16.50 16.38 16.53 20.00 18.09 17.13 17.24

– second lien .......... 10.80 10.93 10.63 10.87 12.57 17.25 16.36 16.35 17.44

– total ..................... 17.09 16.83 15.71 15.62 15.98 19.61 17.84 17.01 17.27

Consumer Lending:

– first lien ............... 16.23 16.16 14.85 14.79 15.41 18.15 16.75 14.72 13.52

– second lien .......... 12.72 13.16 12.44 12.25 13.98 18.64 17.49 16.17 15.43

– total ..................... 15.88 15.85 14.59 14.51 15.24 18.21 16.84 14.90 13.76

For footnotes, see page 174.

Forbearance strategies and renegotiated

loans

(Audited)

A range of forbearance strategies are employed in

order to improve the management of customer

relationships, maximise collection opportunities and,

if possible, avoid foreclosure or repossession. Our

policies and practices are based on criteria which, in

the judgement of local management, indicate that

repayment is likely to continue.

Forbearance arrangements include extended

payment terms, a reduction in interest or principal

repayments, approved external debt management

plans, the deferral of foreclosures, other

modifications, and loan restructures. These

management policies and practices typically provide

the customer with terms and conditions that are more

favourable than those provided initially. Such

arrangements could include cases where an account

is brought up-to-date without full repayment of all

the arrears.

Our most common forbearance arrangements

are loan restructures applied to real estate loans

within consumer finance portfolios in the US. Our

credit risk management policy sets out restrictions

on the number and frequency of restructures, the

minimum period an account must have been opened

before any restructure can be considered, and the

number of qualifying payments that must be

received before an account may be considered

restructured and up-to-date. The application of this

policy varies according to the nature of the market,

the product and the management of customer

relationships through the occurrence of exceptional

events.

Loans that are subject to restructuring may only

be classified as restructured and up-to-date once a

specified number and/or amount of qualifying

payments have been received. These qualifying

payments are set at a level appropriate to the nature

of the loan and the customer’s ability to make the

repayment going forward. Typically the receipt of

two or more qualifying payments is required within

a certain period, generally 60 days (in the case of

HSBC Finance, in certain circumstances, for

example where debt has been restructured in

bankruptcy proceedings, fewer or no payments may

be required). Loans that have been restructured and

would otherwise have been past due or impaired are

classified as renegotiated.

Renegotiated loans are segregated from other

parts of the loan portfolio for collective impairment

assessment, to reflect the higher rates of losses often

encountered in this segment of the portfolio. When

empirical evidence indicates an increased propensity

to default and higher losses on such accounts, the use

of roll rate methodology ensures these factors are

taken into account when calculating impairment

allowances. The carrying amount of loans that

have been classified as renegotiated retain this

classification until maturity or derecognition. Interest

is recorded on renegotiated loans on the basis of new

contractual terms following renegotiation.