HSBC 2010 Annual Report Download - page 252

Download and view the complete annual report

Please find page 252 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

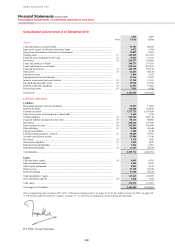

HSBC HOLDINGS PLC

Notes on the Financial Statements

1 – Basis of preparation

250

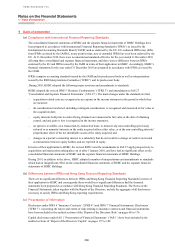

1 Basis of preparation

(a) Compliance with International Financial Reporting Standards

The consolidated financial statements of HSBC and the separate financial statements of HSBC Holdings have

been prepared in accordance with International Financial Reporting Standards (‘IFRSs’) as issued by the

International Accounting Standards Board (‘IASB’) and as endorsed by the EU. EU-endorsed IFRSs may differ

from IFRSs as issued by the IASB if, at any point in time, new or amended IFRSs have not been endorsed by the

EU. At 31 December 2010, there were no unendorsed standards effective for the year ended 31 December 2010

affecting these consolidated and separate financial statements, and there was no difference between IFRSs

endorsed by the EU and IFRSs issued by the IASB in terms of their application to HSBC. Accordingly, HSBC’s

financial statements for the year ended 31 December 2010 are prepared in accordance with IFRSs as issued by

the IASB.

IFRSs comprise accounting standards issued by the IASB and its predecessor body as well as interpretations

issued by the IFRS Interpretations Committee (‘IFRIC’) and its predecessor body.

During 2010, HSBC adopted the following major revisions and amendments to standards:

HSBC adopted the revised IFRS 3 ‘Business Combinations’ (‘IFRS 3’) and amendments to IAS 27

‘Consolidated and Separate Financial Statements’ (‘IAS 27’). The main changes under the standards are that:

– acquisition-related costs are recognised as an expense in the income statement in the period in which they

are incurred;

– all consideration transferred, including contingent consideration, is recognised and measured at fair value at

the acquisition date;

– equity interests held prior to control being obtained are remeasured to fair value at the date of obtaining

control, and any gain or loss is recognised in the income statement;

– an option is available, on a transaction-by-transaction basis, to measure any non-controlling (previously

referred to as minority) interests in the entity acquired either at fair value, or at the non-controlling interests’

proportionate share of the net identifiable assets of the entity acquired; and

– changes in a parent’s ownership interest in a subsidiary that do not result in a change of control are treated

as transactions between equity holders and are reported in equity.

In terms of their application to HSBC, the revised IFRS 3 and the amendments to IAS 27 apply prospectively to

acquisitions and transactions taking place on or after 1 January 2010, and have had no significant effect on the

consolidated financial statements of HSBC and the separate financial statements of HSBC Holdings.

During 2010, in addition to the above, HSBC adopted a number of interpretations and amendments to standards

which had an insignificant effect on the consolidated financial statements of HSBC and the separate financial

statements of HSBC Holdings.

(b) Differences between IFRSs and Hong Kong Financial Reporting Standards

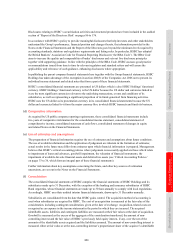

There are no significant differences between IFRSs and Hong Kong Financial Reporting Standards in terms of

their application to HSBC and consequently there would be no significant differences had the financial

statements been prepared in accordance with Hong Kong Financial Reporting Standards. The Notes on the

Financial Statements, taken together with the Report of the Directors, include the aggregate of all disclosures

necessary to satisfy IFRSs and Hong Kong reporting requirements.

(c) Presentation of information

Disclosures under IFRS 4 ‘Insurance Contracts’ (‘IFRS 4’) and IFRS 7 ‘Financial Instruments: Disclosures’

(‘IFRS 7’) concerning the nature and extent of risks relating to insurance contracts and financial instruments

have been included in the audited sections of the ‘Report of the Directors: Risk’ on pages 86 to 176.

Capital disclosures under IAS 1 ‘Presentation of Financial Statements’ (‘IAS 1’) have been included in the

audited sections of ‘Report of the Directors: Capital’ on pages 177 to 182.