HSBC 2010 Annual Report Download - page 173

Download and view the complete annual report

Please find page 173 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

171

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

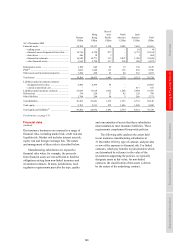

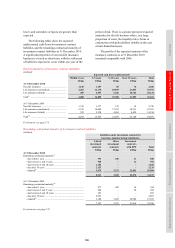

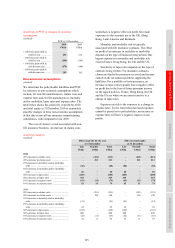

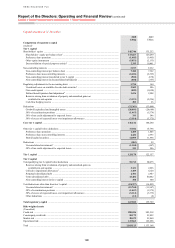

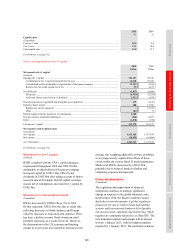

Sensitivity of PVIF to changes in economic

assumptions

(Audited)

PVIF at 31 December

2010 2009

US$m US$m

+ 100 basis point shift in

risk-free rate ................ 231 212

– 100 basis point shift in

risk-free rate ................ (190) (145)

+ 100 basis point shift in

risk discount rate ......... (179) (140)

– 100 basis point shift in

risk discount rate ......... 205 162

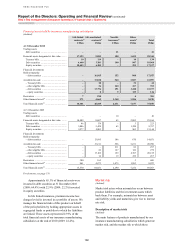

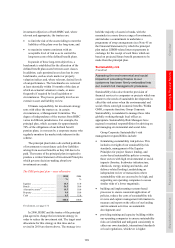

Non-economic assumptions

(Audited)

We determine the policyholder liabilities and PVIF

by reference to non-economic assumptions which

include, for non-life manufacturers, claims costs and

expense rates and, for life manufacturers, mortality

and/or morbidity, lapse rates and expense rates. The

table below shows the sensitivity of profit for 2010

and total equity at 31 December 2010 to reasonably

possible changes in these non-economic assumptions

at that date across all our insurance manufacturing

subsidiaries, with comparatives for 2009.

The cost of claims is a risk associated with non-

life insurance business. An increase in claims costs

would have a negative effect on profit. Our main

exposures to this scenario are in the UK, Hong

Kong, Latin America and Bermuda.

Mortality and morbidity risk is typically

associated with life insurance contracts. The effect

on profit of an increase in mortality or morbidity

depends on the type of business being written. Our

largest exposures to mortality and morbidity risk

exist in France, Hong Kong, the UK and the US.

Sensitivity to lapse rates depends on the type of

contracts being written. For insurance contracts,

claims are funded by premiums received and income

earned on the investment portfolio supporting the

liabilities. For a portfolio of term assurance, an

increase in lapse rates typically has a negative effect

on profit due to the loss of future premium income

on the lapsed policies. France, Hong Kong, the UK

and the US are where we are most sensitive to a

change in lapse rates.

Expense rate risk is the exposure to a change in

expense rates. To the extent that increased expenses

cannot be passed on to policyholders, an increase in

expense rates will have a negative impact on our

profits.

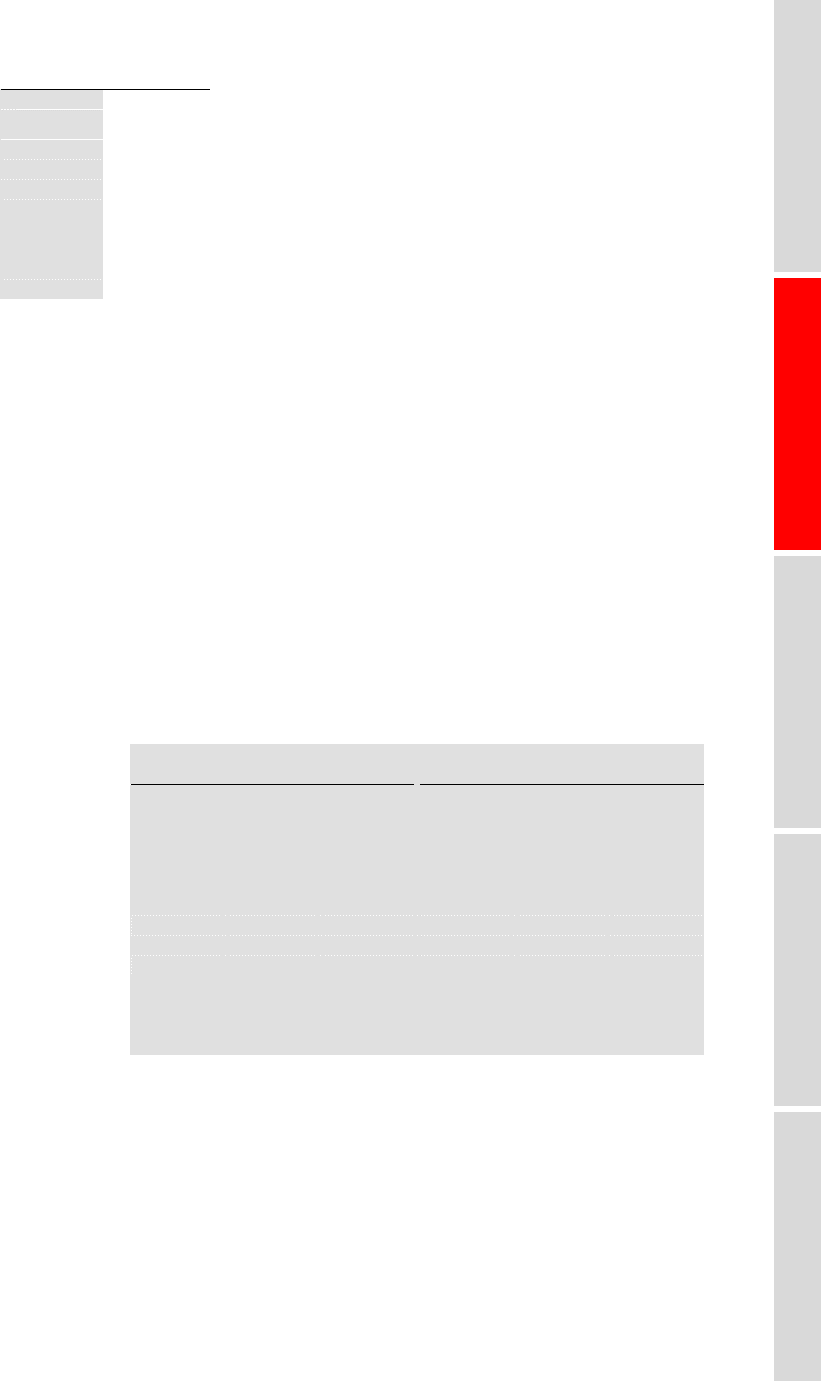

Sensitivity analysis

(Audited)

Effect on profit for the year

to 31 December

Effect on total equity

at 31 December

Life Non-life Total Life Non-life Total

US$m US$m US$m US$m US$m US$m

2010

20% increase in claims costs .............................. – (211) (211) – (211) (211)

20% decrease in claims costs ............................. – 211 211 – 211 211

10% increase in mortality and/or morbidity

rates ................................................................. (55) – (55) (55) – (55)

10% decrease in mortality and/or morbidity

rates ................................................................. 66 – 66 66 – 66

50% increase in lapse rates ................................. (203) – (203) (203) – (203)

50% decrease in lapse rates ................................ 363 – 363 363 – 363

10% increase in expense rates ............................ (63) (11) (74) (63) (11) (74)

10% decrease in expense rates ........................... 63 11 74 63 11 74

2009

20% increase in claims costs .............................. – (191) (191) – (191) (191)

20% decrease in claims costs ............................. – 190 190 – 190 190

10% increase in mortality and/or morbidity

rates ................................................................. (51) – (51) (51) – (51)

10% decrease in mortality and/or morbidity

rates ................................................................. 62 – 62 62 – 62

50% increase in lapse rates ................................. (162) – (162) (162) – (162)

50% decrease in lapse rates ................................ 408 – 408 408 – 408

10% increase in expense rates ............................ (52) (11) (63) (52) (11) (63)

10% decrease in expense rates ........................... 52 11 63 52 11 63