HSBC 2010 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

163

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

features expose the subsidiaries, are discussed

below.

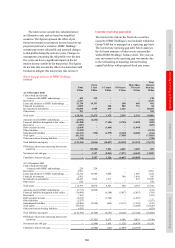

Long-term insurance or investment products

may incorporate benefits that are guaranteed. The

table below shows, in respect of each category of

guarantee, the total liabilities to policyholders

established for guaranteed products manufactured by

our insurance subsidiaries. The table also shows the

range of investment returns (net of operating costs)

on the assets supporting these products and the

implied investment returns that would enable the

business to meet the guarantees.

Categories of guaranteed benefits

• annuities in payment;

• deferred/immediate annuities: these consist of two phases –

the savings and investing phase and the retirement income

phase;

• annual return: the annual return is guaranteed to be no lower

than a specified rate. This may be the return credited to the

policyholder every year, or the average annual return

credited to the policyholder over the life of the policy,

which may occur on the maturity date or the surrender date

of the contract; and

• capital: policyholders are guaranteed to receive no less than

the premiums paid plus declared bonuses less expenses.

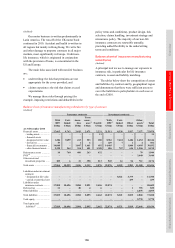

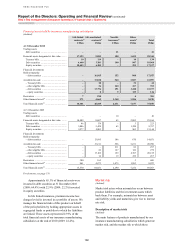

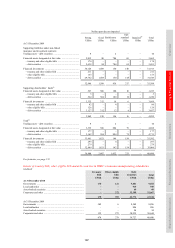

Liabilities to policyholders87

(Audited)

2010 2009

Amount of

reserve

Investment

returns

implied by

guarantee81

Current

yields

Amount of

reserve

Investment

returns

implied by

guarantee82

Current

yields

US$m % % US$m % %

Annuities in payment ............................... 1,491 0.0 – 8.5 1.5 – 16.2 1,299 0.0 – 7.5 1.3 – 16.7

Deferred annuities ................................... 642 0.0 – 6.0 2.1 – 16.8 569 0.0 – 6.0 0.9 – 15.1

Immediate annuities ................................. 532 6.0 -– 9.0 5.5 – 5.5 553 6.0 – 9.0 5.4 – 5.4

Annual return ........................................... 19,980 0.0 – 4.5 0.0 – 5.9 17,147 0.0 – 4.5 0.8 – 6.2

Annual return ........................................... 841 4.5 – 6.0 6.1 – 8.5 497 4.5 – 6.0 5.1 – 6.5

Capital ...................................................... 15,445

– 2.0 – 4.0 15,866 – 2.4 – 4.3

For footnotes, see page 174.

Interest rate risk arises to the extent that yields

on the assets are lower than the investment returns

implied by the guarantees payable to policyholders

by insurance manufacturing subsidiaries. When this

happens, we may discontinue products.

The proceeds from insurance and investment

products with DPF are primarily invested in bonds

with a proportion allocated to other asset classes in

order to provide customers with the potential for

enhanced returns. Subsidiaries with portfolios of

such products are exposed to the risk of falls in

market prices which cannot be fully reflected in

the discretionary bonuses. An increase in market

volatility could also result in an increase in the

value of the guarantee to the policyholder.

Long-term insurance and investment products

typically permit the policyholder to surrender the

policy or let it lapse at any time. When the surrender

value is not linked to the value realised from the sale

of the associated supporting assets, the subsidiary is

exposed to market risk. In particular, when customers

seek to surrender their policies when asset values are

falling, assets may have to be sold at a loss to fund

redemptions.

A subsidiary holding a portfolio of long-term

insurance and investment products, especially with

DPF, may attempt to reduce exposure to its local

market by investing in assets in countries other

than that in which it is based. These assets may

be denominated in currencies other than the

subsidiary’s local currency. It is often not cost

effective for the subsidiary to hedge the foreign

exchange exposure associated with these assets, and

this exposes it to the risk that its local currency will

strengthen against the currency of the related assets.

For unit-linked contracts, market risk is

substantially borne by the policyholder, but we

typically remain exposed to market risk as the

market value of the linked assets influences the

fees we earn for managing them.

Asset and liability matching

It may not always be possible to achieve a complete

matching of asset and liability durations, partly

because there is uncertainty over policyholder

behaviour, which introduces uncertainty over the

receipt of all future premiums and the timing of

claims, and partly because the duration of liabilities

may exceed the duration of the longest available

dated fixed interest investments.