HSBC 2010 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Geographical regions > Europe

52

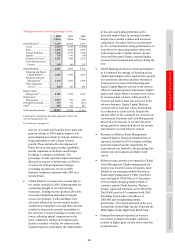

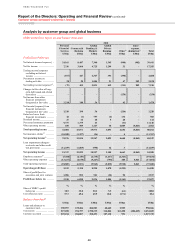

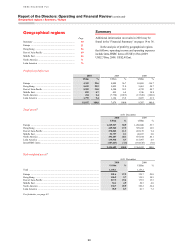

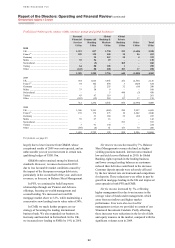

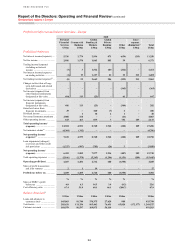

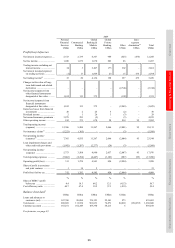

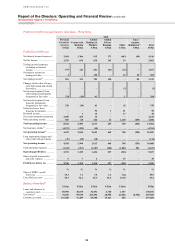

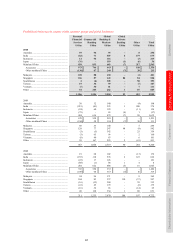

Profit/(loss) before tax by country within customer groups and global businesses

Personal

Financial

Services

US$m

Commercial

Banking

US$m

Global

Banking &

Markets

US$m

Global

Private

Banking

US$m

Other

US$m

Total

US$m

2010

UK ..................................................................... 1,223 827 1,730 223 (1,605) 2,398

France60 ............................................................. 109 135 405 18 26 693

Germany ........................................................... – 32 267 30 4 333

Malta ................................................................. 35 56 19 – – 110

Switzerland ....................................................... – (5) – 265 – 260

Turkey ............................................................... 64 80 105 1 – 250

Other ................................................................. (142) 80 200 103 17 258

1,289 1,205 2,726 640 (1,558) 4,302

2009

UK ..................................................................... 364 1,026 3,045 252 (2,561) 2,126

France60 ............................................................. 54 102 894 3 (429) 624

Germany ........................................................... – 21 255 32 (18) 290

Malta ................................................................. 33 58 9 – – 100

Switzerland ....................................................... – – 5 448 (3) 450

Turkey ............................................................... 43 97 119 2 – 261

Other ................................................................. (182) (12) 218 117 17 158

312 1,292 4,545 854 (2,994) 4,009

2008

UK ..................................................................... 1,546 2,361 (469) 250 2,997 6,685

France60 ............................................................. 139 176 273 10 2,242 2,840

Germany ........................................................... – 31 184 32 (22) 225

Malta ................................................................. 59 67 16 – – 142

Switzerland ....................................................... – – – 553 – 553

Turkey ............................................................... 3 91 130 – – 224

Other ................................................................. (89) (4) 61 153 79 200

1,658 2,722 195 998 5,296 10,869

For footnote, see page 83.

largely due to lower income from GB&M, whose

exceptional results of 2009 were not repeated, and an

unfavourable year on year movement in certain non-

qualifying hedges of US$1.1bn.

GB&M results remained strong by historical

standards. However, revenues decreased in 2010

due to less favourable market conditions caused by

the impact of the European sovereign debt crisis,

particularly in the second half of the year, and lower

revenues, as forecast, in Balance Sheet Management.

In PFS, we continued to build long-term

relationships through our Premier and Advance

offerings, focusing on wealth management and

secured lending. We increased our total UK

mortgage market share to 5.2%, while maintaining a

conservative new lending loan to value ratio of 54%.

In CMB, we made further progress on our

strategy of becoming the leading international

business bank. We also expanded our business in

Germany and launched in Switzerland. In the UK,

we increased new lending to SMEs by 19% in 2010.

Net interest income decreased by 7%. Balance

Sheet Management revenues declined, as higher-

yielding positions matured, interest rates remained

low and yield curves flattened in 2010. In Global

Banking, tighter spreads in the lending business

and lower average lending balances as customers

reduced their debt also contributed to the decrease.

Customer deposit spreads were adversely affected

by the low interest rate environment and competition

for deposits. These reductions were offset in part by

growth in mortgage lending in the UK and improved

asset spreads in both PFS and CMB.

Net fee income increased by 7%, reflecting

higher management fees due to an increase in the

average value of funds under management, which

arose from net inflows and higher market

performance. Fees were also received for

management services we provided to certain of our

Structured Investment Conduits. Partly offsetting

these increases were reductions in the levels of debt

and equity issuance in the market, compared with the

significant volumes seen in 2009.