HSBC 2010 Annual Report Download - page 10

Download and view the complete annual report

Please find page 10 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Overview (continued)

Group Chief Executive’s Business Review

8

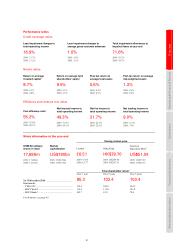

• Total loans and advances to customers increased

by 7% to US$958bn while deposits rose by 6%

to US$1.2 trillion.

Impact of the evolving regulatory

environment on the business

Much of the detail around the potential impact

of change for banks remains uncertain. However,

analysis of what we know confirms that our ability

to generate capital and manage our risk-weighted

assets positions HSBC strongly – and competitively

– within the industry as the pace of change

intensifies.

HSBC fully supports the rationale of the

Basel III proposals which require banks to hold more

capital. This is absolutely core to ensuring that

governments and taxpayers are better protected in

future than they have been in the past.

Certain aspects of the Basel III rules remain

uncertain as to interpretation and application by

national regulators. Notably, this includes any capital

requirements which may be imposed on the Group

over the implementation period in respect of the

countercyclical capital buffer and any additional

regulatory requirements for SIFIs. However, we

believe that ultimately the level for the common

equity tier 1 ratio of the Group may lie in the range

9.5 to 10.5%. This exceeds the minimum

requirement for common equity tier 1 capital plus

the capital conservation buffer.

We have estimated the pro forma common

equity tier 1 ratio of the Group based on our

interpretation of the new Basel III rules as they will

apply from 1 January 2019, based on the position of

the Group at year-end 2010. The rules will be phased

in from 2013 with a gradual impact and we have

estimated that their full application, on a proforma

basis, would result in a common equity tier 1 ratio

which is lower than the Basel II core tier 1 ratio by

some 250–300 basis points. The changes relate

to increased capital deductions, new regulatory

adjustments and increases in risk-weighted assets.

However, as the changes will progressively take

effect over six years leading up to 2019 and as

HSBC has a strong track record of capital generation

and actively manages its risk-weighted assets, we

are confident in our ability to mitigate the effect of

the new rules before they come into force.

Last year, HSBC committed to reviewing its

target shareholder return on equity once the effects

of new regulation became clearer. Now that we have

better visibility on the impact of increased capital

requirements, we believe that higher costs of the

evolving regulatory framework will, all other things

being equal, depress returns for shareholders of

banks. We will therefore target a return on average

shareholders’ equity of 12-15% in the future.

As Group Chief Executive, it is right that, in

managing the business and developing Group

strategy, my principal office should be in Hong

Kong – a global financial hub of growing importance

at the centre of HSBC’s strategically most important

region. However, the company is headquartered in

London and we hope to remain there. London’s pre-

eminence as an international financial services centre

is widely recognised and well-deserved and reflects

successful government policy over decades to build

that position. It is therefore important to us that the

UK’s competitive position is protected and

sustained. Appropriate supervision is an important

part of the larger equation. Policymakers should

continue to legislate and regulate, but they must not

destroy London’s competitive position in the

process.

As the Group Chairman has outlined, new

legislation is expected to be enacted in the UK,

effective from the start of 2011, one curious

consequence of which is an explicit incremental cost

of being headquartered in the UK for any global

bank. Had this been applied for 2010, this annual

charge would have amounted to approximately

US$0.6bn in HSBC’s case. Moreover, the overseas

balance sheet would account for the majority of the

annual charge, with the UK balance sheet accounting

for approximately one third of the total.

Outlook

We have been closely watching events unfold in

parts of the Middle East and North Africa. Our

primary concern is for the security of our 12,000

staff across the region and we continue to work to

ensure their safety. We have also activated robust

continuity plans so that we can also stay open for

business and support the needs of our customers. As

a strongly capitalised global bank, HSBC’s financial

performance has not been materially affected by

events to date. HSBC has been present in the Middle

East for more than 50 years and we remain

absolutely committed to its future. We also believe

that the region’s economies have a number of

structural strengths which leave us positive on the

longer-term outlook.

In the short term, risks to global growth remain,

not least from an elevated oil price. We therefore

expect cyclical volatility to continue – including in

emerging markets – and progress is unlikely to be

linear. In the longer term, we believe that growth