HSBC 2010 Annual Report Download - page 294

Download and view the complete annual report

Please find page 294 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

284 -

285

285 -

286

286 -

287

287 -

288

288 -

289

289 -

290

290 -

291

291 -

292

292 -

293

293 -

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

304 -

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Notes on the Financial Statements (continued)

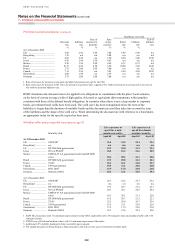

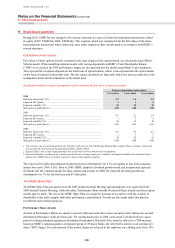

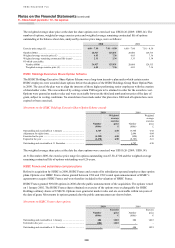

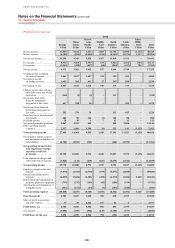

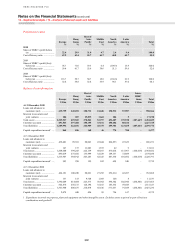

10 – Tax expense

292

The following table reconciles the tax expense which would apply if all profits had been taxed at the UK corporation

tax rate:

Analysis of tax expense

2010 2009 2008

US$m % US$m % US$m %

Taxation at UK corporation tax rate of 28%

(2009: 28%; 2008: 28.5%)1 ......................................... 5,330 28.0 1,982 28.0 2,652 28.5

Goodwill impairment ....................................................... – – – – 3,010 32.3

Non-deductible loss on foreign exchange swaps on

rights issue proceeds2 .................................................. – – 96 1.4 – –

Effect of taxing overseas profits in principal locations

at different rates ........................................................... (744) (3.9) (1,345) (19.0) (1,339) (14.4)

Gains not subject to tax ................................................... (275) (1.4) (238) (3.4) (1,016) (10.9)

Adjustments in respect of prior period liabilities ............ – – (39) (0.6) (67) (0.7)

Low income housing tax credits3 .................................... (86) (0.5) (98) (1.4) (103) (1.1)

Effect of profit in associates and joint ventures .............. (705) (3.7) (499) (7.1) (473) (5.1)

Tax impact of intra-group transfer of subsidiary4 ........... 1,216 6.4 – – – –

Impact of gains arising from dilution of interests

in associates ................................................................. (53) (0.3) – – – –

Deferred tax temporary differences not

provided/(previously not recognised)5 ........................ (6) – 360 5.1 157 1.7

Non taxable income ......................................................... (374) (2.0) (365) (5.2) (519) (5.6)

Permanent disallowables ................................................. 276 1.5 223 3.2 217 2.3

Additional provision for tax on overseas dividends ............ – – 341 4.8 294 3.2

Effect of bank payroll tax ................................................ 79 0.4 – – – –

Change in tax rates .......................................................... 31 0.2 (10) (0.1) (89) (0.9)

Local taxes and overseas withholding tax ....................... 61 0.3 12 0.1 122 1.3

Other items ....................................................................... 96 0.5 (35) (0.4) (37) (0.4)

Tax expense1 .................................................................... 4,846 25.5 385 5.4 2,809 30.2

1 The change in the UK corporation tax rate from 30% to 28% with effect from 1 April 2008 gave rise to a blended tax rate for 2008 of

28.5%.

2 In August 2009, the UK Government enacted legislation that gains or losses on transactions designated to hedge foreign exchange

exposures connected to rights issues should be disregarded for tax purposes.

3 Low income housing tax credits arise in the US and are designed to encourage the provision of rental housing for low income

households.

4 This relates to the transfer of HSBC Bank Canada, which was part of the sub-group headed by HSBC North America Holdings Inc, to

HSBC Overseas Holdings (UK) Limited. A taxable gain arises on this disposal but the crystallisation of deferred tax assets and

utilisation of current year foreign tax credits meant that no tax was paid on this transfer.

5 2009 and 2008 include the effect of previously unrecognised temporary differences principally related to the recognition of foreign tax

credits and trading losses, respectively.

On 22 June 2010, the UK Government announced its intention to reduce the main rate of corporation tax from 28% to

24%. It is proposed that the reduction will be phased in over a period of four years with a 1% decrease in the main

corporation tax rate for each year starting on 1 April 2011. As at 31 December 2010, only the initial phase to reduce

the main rate of UK corporation tax from 28% to 27% has been substantively enacted and therefore only this change

has been reflected in the amounts recognised as at that date. However, it is not expected that the future proposed rate

changes will have a significant effect on the net UK deferred tax asset recognised at 31 December 2010 of US$383m.

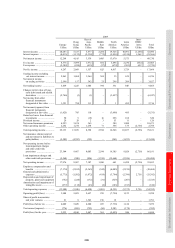

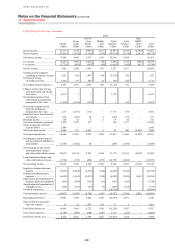

Deferred taxation

The following table shows the deferred tax assets and liabilities before offsetting balances within countries and the

related movements recognised in the income statement, other comprehensive income and directly in equity.