HSBC 2010 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

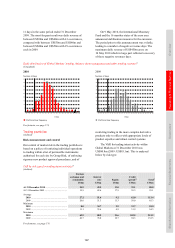

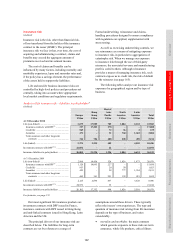

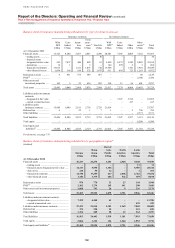

Risk > Market risk > Sensitivity of NII / Defined benefit pension schemes

150

Assuming no management actions, a sequence of

such rises would increase planned net interest

income for 2011 by US$882m (2010: US$695m),

while a sequence of such falls would decrease

planned net interest income by US$1,525m

(2010: US$1,563m). These figures incorporate the

effect of any option features in the underlying

exposures.

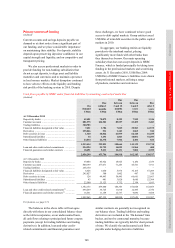

Sensitivity of projected net interest income73

(Unaudited)

US dollar

bloc

US$m

Rest of

Americas

bloc

US$m

Hong Kong

dollar

bloc

US$m

Rest of

Asia

bloc

US$m

Sterling

bloc

US$m

Euro

bloc

US$m

Total

US$m

Change in 2011 projected net

interest income arising from

a shift in yield curves of:

+25 basis points at the

beginning of each quarter ..... 164 72 191 245 292 (82) 882

–25 basis points at the

beginning of each quarter ..... (550) (68) (280) (143) (546) 62 (1,525)

Change in 2010 projected net

interest income arising from

a shift in yield curves of:

+25 basis points at the

beginning of each quarter ..... 13 92 416 112 363 (301) 695

–25 basis points at the

beginning of each quarter ..... (382) (46) (507) (133) (689) 194 (1,563)

For footnote, see page 174.

The interest rate sensitivities set out in the

table above are illustrative only and are based on

simplified scenarios.

The figures represent the effect of the pro forma

movements in net interest income based on the

projected yield curve scenarios and our current

interest rate risk profile. This effect, however, does

not incorporate actions that would be taken by

Balance Sheet Management within Global Markets

or in the business units to mitigate the impact of

this interest rate risk; in reality, Balance Sheet

Management seeks proactively to change the interest

rate risk profile to minimise losses and optimise net

revenues. The projections above also assume that

interest rates of all maturities move by the same

amount and, therefore, do not reflect the potential

effect on net interest income of some rates changing

while others remain unchanged. In addition, the

projections take account of the effect on net interest

income of anticipated differences in changes

between interbank interest rates and interest rates

linked to other bases (such as Central Bank rates or

product rates over which the entity has discretion in

terms of the timing and extent of rate changes). The

projections make other simplifying assumptions too,

including that all positions run to maturity.

Projecting the movement in net interest income

from prospective changes in interest rates is a

complex interaction of structural and managed

exposures. Our exposure to the effect of movements

in interest rates on our net interest income arises in

two main areas, core deposit franchises and Balance

Sheet Management:

• core deposit franchises are exposed to changes

in the cost of deposits raised and spreads on

wholesale funds. The net interest income benefit

of core deposits increases as interest rates rise

and decreases as interest rates fall. This risk

is asymmetrical in a very low interest rate

environment, however, as there is limited room

to lower deposit pricing in the event of interest

rate reductions; and

• residual interest rate risk is managed within

Balance Sheet Management, under our policy of

transferring interest rate risk to Balance Sheet

Management to be managed within defined

limits and with flexibility as to the instruments

used.

The table above reflects the fact that our deposit

taking businesses will generally benefit from rising

rates which will be partially offset by increased

funding costs in Balance Sheet Management given

our simplifying assumption of unchanged Balance

Sheet Management positioning. Additionally, the

benefit to deposit taking businesses of rising rates is

also offset by the increased funding cost of trading

assets, which is recorded in ‘Net interest income’

and therefore captured in the above table, whereas

the income from such assets is recorded in ‘Net

trading income’.