HSBC 2010 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2010 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

|

|

35

Overview Operating & Financial Review Governance Financial Statements Shareholder Information

• selecting an appropriate discount rate for

the instrument. The determination of this rate

is based on an assessment of what a market

participant would regard as the appropriate

spread of the rate for the instrument over the

appropriate risk-free rate; and

• judgement to determine what model to use to

calculate fair value in areas where the choice of

valuation model is particularly subjective, for

example, when valuing complex derivative

products.

When applying a model with unobservable

inputs, estimates are made to reflect uncertainties

in fair values resulting from a lack of market data

inputs, for example, as a result of illiquidity in

the market. For these instruments, the fair value

measurement is less reliable. Inputs into valuations

based on unobservable data are inherently uncertain

because there is little or no current market data

available from which to determine the level at which

an arm’s length transaction would occur under

normal business conditions. However, in most cases

there is some market data available on which to base

a determination of fair value, for example historical

data, and the fair values of most financial

instruments are based on some market observable

inputs even when unobservable inputs are

significant.

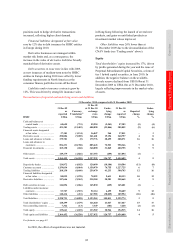

The value of financial assets and liabilities

measured at fair value using a valuation technique

was US$599bn (2009: US$599bn) and US$499bn

(2009: US$447bn), respectively or 56% (2009: 56%)

of total financial assets and 77% (2009: 75%) of

total financial liabilities measured at fair value.

Disclosures of the types and amounts of

adjustments made in determining the fair value of

financial instruments measured at fair value using

valuation techniques, and a sensitivity analysis of

fair values for financial instruments with significant

unobservable inputs to reasonably possible

alternative assumptions can be found in Note 16 on

the Financial Statements. Given the uncertainty and

subjective nature of valuing financial instruments at

fair value, it is possible that the outcomes in the next

financial year could differ from the assumptions

used, and this could result in a material adjustment

to the carrying amount of financial instruments

measured at fair value.

Impairment of available-for-sale financial

assets

Our accounting policy for impairment of available-

for-sale financial assets is described in Note 2j on

the Financial Statements.

At 31 December 2010, our total available-for-

sale financial assets amounted to US$381bn (2009:

US$352bn), of which US$373bn or 98% (2009:

US$342bn; 97%) were debt securities. The

available-for-sale fair value reserve relating to

debt securities amounted to a deficit of US$6.2bn

(2009: deficit of US$11.4bn). A deficit in the

available-for-sale fair value reserve occurs on debt

securities when the fair value of a relevant security

is less than its acquisition cost (net of any principal

repayments and amortisation) after deducting any

previous impairment loss recognised in the income

statement, but where there is no evidence of any

impairment or, if an impairment was previously

recognised, any subsequent impairment.

Management is required to exercise judgement

in determining whether there is objective evidence

that an impairment loss has occurred. Once an

impairment has been identified, the amount of

impairment loss is measured with reference to the

fair value of the asset. More information on

assumptions and estimates requiring management

judgement relating to the determination of fair

values of financial instruments is provided above

in ‘Valuation of financial instruments’.

Deciding whether an available-for-sale debt

security is impaired requires objective evidence of

both the occurrence of a loss event and a related

decrease in estimated future cash flows. The degree

of judgement involved is less when cash flows

are readily determinable, but increases when

estimating future cash flows requires consideration

of a number of variables, some of which may be

unobservable in current market conditions.

There is no single factor to which the Group’s

charge for impairment of available-for-sale debt

securities is particularly sensitive, because of the

various types of securities we hold, the range of

geographical areas in which those securities are held,

and the wide range of factors which can affect the

occurrence of loss events and the cash flows of

securities, including different types of collateral.

The most significant judgements concern more

complex instruments, such as ABSs, where it is

necessary to consider factors such as the estimated

future cash flows on underlying pools of collateral

including prepayment speeds, the extent and depth of

market price declines and changes in credit ratings.

The review of estimated future cash flows on

underlying collateral is subject to uncertainties when

the assessment is based on historical information on

pools of assets, and judgement is required to

determine whether historical performance remains