HSBC 2011 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

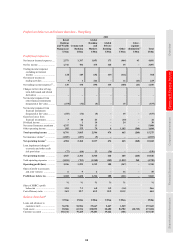

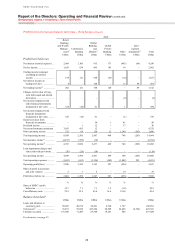

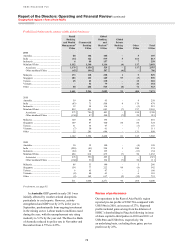

Geographical regions > Europe

62

In Continental Europe, we experienced strong

demand in term lending and significant growth in

our deposit base in both RBWM and CMB,

reflecting marketing and pricing initiatives. Our

Trade and Supply Chain business performed strongly

across the region, following the launch of our export

initiative during 2011. In Europe we now have 18

countries with full renminbi functionality with the

ability to settle trade transactions via either Shanghai

or Hong Kong.

We won several awards in GB&M including

‘Best Debt House’ in Western Europe and the UK

from Euromoney Awards for Excellence in 2011.

We continued to invest in technology platforms

including Equities and Prime Services and are

therefore well positioned to capture medium-term

opportunities in the region. We also continued to

focus on cross-border initiatives to position

ourselves to take advantage of trade flows. In

Payments & Cash Management, enhanced network

capabilities together with innovative liquidity,

channel and payables solutions allowed us to win

substantial business across the corporate and

financial institution business segments.

In GPB, revenue growth was driven by increased

client activity as we leveraged our global businesses’

strengths and connectivity. GPB continues to build

on its expertise in alternative investments, emerging

markets and foreign exchange.

The pace of regulatory reform is expected to gain

momentum. This will include forthcoming

legislation arising from the UK Independent

Commission on Banking which is likely to require us

to make significant changes to our corporate

structure and business activities conducted through

our UK banking subsidiary, HSBC Bank (see

page 101).

Net interest income decreased by 6%, reflecting

the decline in Balance Sheet Management revenues

as higher-yielding positions matured and

opportunities for reinvestment at similar yields were

limited by the prevailing low interest rate

environment. This was coupled with a fall in Credit

and Lending net interest income as a result of lower

balances, coupled with a decrease in effective yields

and lower asset holdings in our legacy credit

portfolio as a result of maturities and disposals

aimed at reducing capital consumption. The above

factors were partly offset by higher net interest

income in CMB, driven by an increase in term

lending balances in the UK and Continental Europe

as a result of targeted campaigns during 2010 and

2011. Net interest income also benefited from strong

mortgage balance growth in the UK along with

strong deposit growth across the region, mainly

driven by marketing campaigns, although offset in

part by strong competition for deposits resulting in

lower deposit spreads, notably in RBWM in the UK.

Net fee income declined by 4% as management

services income generated from the securities

investment conduits within our legacy credit

portfolio was lower, along with higher intercompany

fees payable on intra-group referrals. In addition,

overdraft fees declined due to reduced customer

appetite for debt in the current market conditions.

This was partly offset by higher levels of client

activity in GPB due to an increase in transaction

volumes related to higher market volatility.

Net trading income decreased by 33%, due to

significantly lower trading revenues in Credit and

Rates as turmoil in eurozone sovereign debt markets

escalated in the second half of 2011. Increased risk

aversion and limited client activity led to a

significant widening of spreads on certain eurozone

sovereign and corporate bonds, resulting in losses

in our Credit and Rates businesses. In addition,

legacy credit revenues fell due to the non-recurrence

of the price appreciation on legacy assets in 2010.

Lower favourable foreign exchange movements

were also reported on trading assets held as

economic hedges of foreign currency debt

designated at fair value. These offset lower adverse

foreign exchange movements on the foreign

currency debt which are reported in ‘Net expense

from financial instruments designated at fair value’.

Trading income included a favourable fair value

movement of US$391m from structured liabilities,

mainly in Rates, as credit spreads widened compared

with adverse fair value movements of US$29m in

2010. In our Equities business, revenues rose as

investment in platforms improved our competitive

positioning and helped capture increased client

flows. This was coupled with lower losses on

portfolio hedges in Global Banking compared with

the previous year.

Net expense from financial instruments

designated at fair value was US$479m, reflecting

net investment losses during 2011 on assets held by

our insurance business to meet liabilities under

insurance and investment contracts as equity markets

fell, notably in the second half of 2011, compared

with gains reported in 2010. To the extent that these

losses were attributable to policyholders holding

unit-linked insurance policies and insurance or

investment contracts with DPF, there was a

corresponding decrease in ‘Net insurance claims

incurred and movement in liabilities to

policyholders’. These losses were partly offset by