HSBC 2011 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

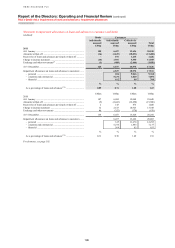

Risk > Credit risk > Credit quality > Renegotiated loans and forbearance

130

more stringent impaired loan disclosure convention

for portfolios with significant levels of forbearance

as described on page 133.

The following tables show the Group’s holdings

of renegotiated loans and advances to customers by

industry sector, geography and credit quality

classification.

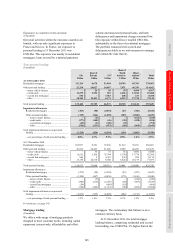

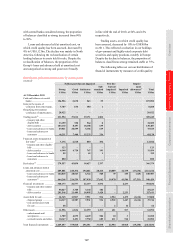

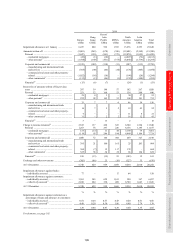

Renegotiated loans and advances to customers

(Audited)

At 31 December 2011 At 31 December 2010

Neither

past

due nor

impaired

Past due

but not

impaired Impaired Total

Neither

past

due nor

impaired

Past due

but not

impaired Impaired Total

US$m US$m US$m US$m US$m US$m US$m US$m

Retail .......................................... 8,133 4,401 19,125 31,659 7,690 4,339 23,406 35,435

Residential Mortgages............ 5,916 3,560 15,932 25,408 5,244 3,381 18,137 26,762

Other personal ....................... 2,217 841 3,193 6,251 2,446 958 5,269 8,673

Commercial real estate ............... 2,793 9 3,248 6,050 2,877 12 2,401 5,290

Corporate and commercial ......... 3,432 461 3,376 7,269 4,125 186 2,501 6,812

Financial .................................... 249 – 491 740 17 – 565 582

Governments .............................. 113 2 132 247 51 – 7 58

14,720 4,873 26,372 45,965 14,760 4,537 28,880 48,177

Total renegotiated loans and advances to customers as a percentage

of total gross loans and advances to customers .................................... 4.8% 5.0%

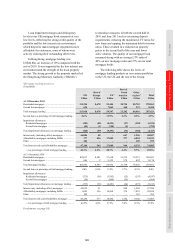

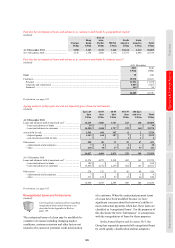

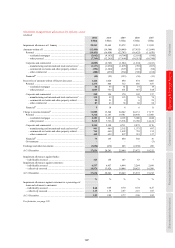

Renegotiated loans and advances to customers by geography

(Unaudited)

2011 2010

US$m US$m

Europe ........................................................................................................................................................................ 11,464 10,692

Hong Kong ................................................................................................................................................................ 447 420

Rest of Asia-Pacific ................................................................................................................................................... 448 679

Middle East and North Africa ................................................................................................................................... 2,655 1,866

North America ........................................................................................................................................................... 28,475 31,990

Latin America ............................................................................................................................................................ 2,476 2,530

Total ........................................................................................................................................................................... 45,965 48,177

Total impairment allowances on renegotiated loans ................................................................................................. 7,670 7,482

Individually assessed ............................................................................................................................................. 2,311 1,657

Collectively assessed ............................................................................................................................................. 5,359 5,825

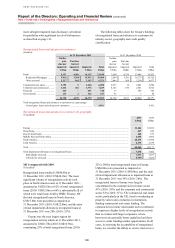

2011 compared with 2010

(Unaudited)

Renegotiated loans totalled US$46.0bn at

31 December 2011 (2010: US$48.1bn). The most

significant volume of renegotiation activity took

place in North America and, at 31 December 2011,

amounted to US$28.5bn or 62% of total renegotiated

loans (2010: US$32.0bn or 66%), substantially all of

which were retail loans held by HSBC Finance. Of

the total renegotiated loans in North America,

US$17.8bn were presented as impaired at

31 December 2011 (2010: US$22.0bn), and the ratio

of total impairment allowances to impaired loans at

31 December 2011 was 28% (2010: 25%).

Europe was the next largest region for

renegotiation activity which, at 31 December 2011,

amounted to US$11.5bn (2010: US$10.7bn),

constituting 25% of total renegotiated loans (2010:

22%). Of the total renegotiated loans in Europe,

US$6.0bn were presented as impaired at

31 December 2011 (2010: US$4.8bn), and the ratio

of total impairment allowances to impaired loans at

31 December 2011 was 30% (2010: 28%). The

renegotiated loans in Europe were largely

concentrated in the commercial real estate sector

41% (2010: 39%) and the corporate and commercial

sector 32% (2010: 31%). The commercial real estate

sector, particularly in the UK, faced a weakening in

property values and a reduction in institutions

funding commercial real estate lending. The

commercial real estate mid-market sector continued

to experience higher levels of renegotiation activity

than is evident with larger corporates, where

borrowers are generally better capitalised and have

access to wider funding market opportunities. In all

cases, in assessing the acceptability of renegotiated

loans, we consider the ability to service interest as a