HSBC 2011 Annual Report Download - page 193

Download and view the complete annual report

Please find page 193 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

191

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

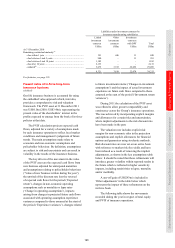

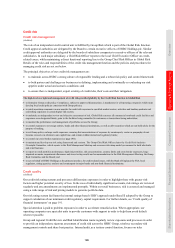

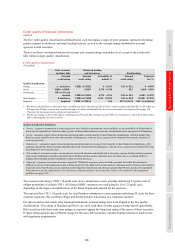

Credit quality of financial instruments

(Audited)

The five credit quality classifications defined below each encompass a range of more granular, internal credit rating

grades assigned to wholesale and retail lending business, as well as the external ratings attributed by external

agencies to debt securities.

There is no direct correlation between the internal and external ratings at granular level, except to the extent each

falls within a single quality classification.

Credit quality classification

(Unaudited)

Debt securities

and other bills Wholesale lending

and derivatives Retail lending

External

credit rating Internal

credit rating

Probability of

default %

Internal

credit rating1 Expected

loss %

Quality classification

Strong ........................... A– and above CRR1 to CRR2 0 – 0.169 EL1 to EL2 0 – 0.999

Good ............................ BBB+ to BBB– CRR3 0.170 – 0.740 EL3 1.000 – 4.999

Satisfactory .................. BB+ to B+ and

unrated

CRR4 to CRR5 0.741 – 4.914 EL4 to EL5 5.000 – 19.999

Sub-standard ................ B and below CRR6 to CRR8 4.915 – 99.999 EL6 to EL8 20.000 – 99.999

Impaired ....................... Impaired CRR9 to CRR10 100 EL9 to EL10 100+ or defaulted2

1 We observe the disclosure convention that, in addition to those classified as EL9 to EL10, retail accounts classified EL1 to EL8 that are

delinquent by 90 days or more are considered impaired, unless individually they have been assessed as not impaired (see page 128,

‘Past due but not impaired gross financial instruments’).

2 The EL percentage is derived through a combination of PD and LGD, and may exceed 100% in circumstances where the LGD is above

100% reflecting the cost of recoveries.

Quality classification definitions

• ‘Strong’: exposures demonstrate a strong capacity to meet financial commitments, with negligible or low probability of default and/or

low levels of expected loss. Retail accounts operate within product parameters and only exceptionally show any period of delinquency.

• ‘Good’: exposures require closer monitoring and demonstrate a good capacity to meet financial commitments, with low default risk.

Retail accounts typically show only short periods of delinquency, with any losses expected to be minimal following the adoption of

recovery processes.

• ‘Satisfactory’: exposures require closer monitoring and demonstrate an average to fair capacity to meet financial commitments, with

moderate default risk. Retail accounts typically show only short periods of delinquency, with any losses expected to be minor following

the adoption of recovery processes.

• ‘Sub-standard’: exposures require varying degrees of special attention and default risk is of greater concern. Retail portfolio segments

show longer delinquency periods of generally up to 90 days past due and/or expected losses are higher due to a reduced ability to

mitigate these through security realisation or other recovery processes.

• ‘Impaired’: exposures have been assessed as impaired. Wholesale exposures where the bank considers that either the customer is

unlikely to pay its credit obligations in full, without recourse by the bank to the actions such as realising security if held, or the customer

is past due more than 90 days on any material credit obligation. Retail loans and advances greater than 90 days past due. Renegotiated

loans that have met the requirements to be disclosed as impaired and have not yet met the criteria to be returned to the unimpaired

portfolio (see page 192).

The customer risk rating (‘CRR’) 10-grade scale above summarises a more granular underlying 23-grade scale of

obligor probability of default (‘PD’). All distinct HSBC customers are rated using the 10 or 23-grade scale,

depending on the degree of sophistication of the Basel II approach adopted for the exposure.

The expected loss (‘EL’) 10-grade scale for retail business summarises a more granular underlying EL scale for these

customer segments; this combines obligor and facility/product risk factors in a composite measure.

For debt securities and certain other financial instruments, external ratings have been aligned to the five quality

classifications. The ratings of Standard and Poor’s are cited, with those of other agencies being treated equivalently.

Debt securities with short-term issue ratings are reported against the long-term rating of the issuer of those securities.

If major rating agencies have different ratings for the same debt securities, a prudent rating selection is made in line

with regulatory requirements.