HSBC 2011 Annual Report Download - page 218

Download and view the complete annual report

Please find page 218 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

Capital > Appendix to Capital > Capital measurement and allocation

216

Regulatory and accounting consolidations

The basis of consolidation for financial accounting purposes is described on page 292 and differs from that used for regulatory purposes.

Investments in banking associates are equity accounted in the financial accounting consolidation, whereas their exposures are

proportionally consolidated for regulatory purposes. Subsidiaries and associates engaged in insurance and non-financial activities are

excluded from the regulatory consolidation and are deducted from regulatory capital. The regulatory consolidation does not include SPEs

where significant risk has been transferred to third parties. Exposures to these SPEs are risk-weighted as securitisation positions for

regulatory purposes.

Basel II is structured around three ‘pillars’: minimum capital requirements, supervisory review process and market

discipline. The CRD implemented Basel II in the EU and the FSA then gave effect to the CRD by including the

latter’s requirements in its own rulebooks.

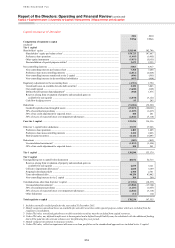

Regulatory capital

Our capital is divided into two tiers:

• tier 1 capital is divided into core tier 1 and other tier 1 capital. Core tier 1 capital comprises shareholders’ equity

and related non-controlling interests. The book values of goodwill and intangible assets are deducted from core

tier 1 capital and other regulatory adjustments are made for items reflected in shareholders’ equity which are

treated differently for the purposes of capital adequacy. Qualifying capital instruments such as non-cumulative

perpetual preference shares and hybrid capital securities are included in other tier 1 capital; and

• tier 2 capital comprises qualifying subordinated loan capital, related non-controlling interests, allowable

collective impairment allowances and unrealised gains arising on the fair valuation of equity instruments held as

available for sale. Tier 2 capital also includes reserves arising from the revaluation of properties.

To ensure the overall quality of the capital base, the FSA’s rules set limits on the amount of hybrid capital

instruments that can be included in tier 1 capital relative to core tier 1 capital, and also limits overall tier 2 capital to

no more than tier 1 capital.

Pillar 1 capital requirements

Pillar 1 covers the capital resources requirements for credit risk, market risk and operational risk. Credit risk includes

counterparty credit risk and securitisation requirements. These requirements are expressed in terms of RWAs.

Credit risk capital requirements

Basel II applies three approaches of increasing sophistication to the calculation of pillar 1 credit risk capital

requirements. The most basic level, the standardised approach, requires banks to use external credit ratings to

determine the risk weightings applied to rated counterparties and group other counterparties into broad categories and

apply standardised risk weightings to these categories. The next level, the internal ratings-based (‘IRB’) foundation

approach, allows banks to calculate their credit risk capital requirements on the basis of their internal assessment of

the probability that a counterparty will default (‘PD’), but subjects their quantified estimates of exposure at default

(‘EAD’) and loss given default (‘LGD’) to standard supervisory parameters. Finally, the IRB advanced approach

allows banks to use their own internal assessment in determining PD and quantifying EAD and LGD.

The capital resources requirement, which is intended to cover unexpected losses, is derived from a formula specified

in the regulatory rules, which incorporates PD, LGD, EAD and other variables such as maturity and correlation.

Expected losses under the IRB approaches are calculated by multiplying PD by EAD and LGD. Expected losses

are deducted from capital to the extent that they exceed total accounting impairment allowances.

For credit risk we have adopted the IRB advanced approach for the majority of our business, with the remainder on

either IRB foundation or standardised approaches.

Under our Basel II rollout plans, a number of our Group companies and portfolios are in transition to advanced IRB

approaches. At end of 2011, portfolios in much of Europe, Hong Kong, Rest of Asia-Pacific and North America were

on advanced IRB approaches. Others remain on the standardised or foundation approaches under Basel II, pending

definition of local regulations or model approval, or under exemptions from IRB treatment.

• Counterparty credit risk

Counterparty credit risk arises for OTC derivatives and securities financing transactions. It is calculated in both

the trading and non-trading books and is the risk that the counterparty to a transaction may default before