HSBC 2011 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

HSBC HOLDINGS PLC

Report of the Directors: Operating and Financial Review (continued)

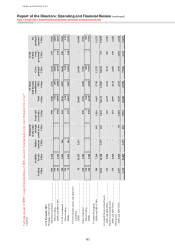

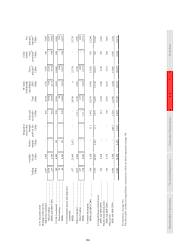

Risk > Credit risk > Collateral

144

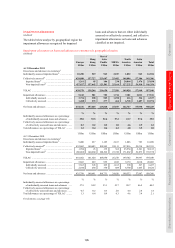

US$463m, largely reflecting an increase in the

volume of accounts that are delinquent.

For an analysis of loan impairment charges and

other credit risk provisions by global business, see

page 57.

Collateral

Collateral and other credit enhancements

held

(Audited)

Loans and advances held at amortised cost

Although collateral can be an important mitigant

of credit risk, it is the Group’s practice to lend on

the basis of the customer’s ability to meet their

obligations out of their cash flow resources rather

than rely on the value of security offered. Depending

on the customer’s standing and the type of product,

facilities may be provided unsecured. However, for

other lending a charge over collateral is obtained and

considered in determining the credit decision and

pricing. In the event of default the bank may utilise

the collateral as a source of repayment.

Depending on its form, collateral can have a

significant financial effect in mitigating our exposure

to credit risk.

The tables below provide a quantification of the

value of fixed charges we hold over a borrower’s

specific asset (or assets) where we have a history

of enforcing, and are able to enforce, the collateral in

satisfying a debt in the event of the borrower failing

to meet its contractual obligations, and where the

collateral is cash or can be realised by sale in an

established market. The collateral valuation in the

tables below exclude any adjustments for obtaining

and selling the collateral.

We may also manage our risk by employing

other types of collateral and credit risk

enhancements, such as second charges, other

liens and unsupported guarantees, but the valuation

of such mitigants is less certain and their financial

effect has not been quantified. In particular, loans

shown in the tables below as not collateralised may

benefit from such credit mitigants.

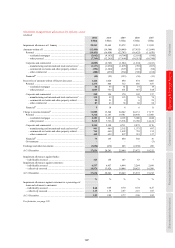

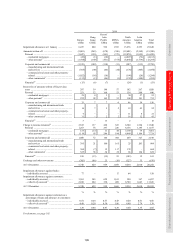

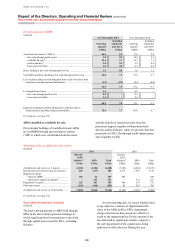

Personal lending

Residential mortgage loans including loan commitments by level of collateral

(Audited)

Europe

Hong

Kong

Rest of

Asia-Pacific MENA

North

America

Latin

America

Total

US$m US$m US$m US$m US$m US$m US$m

At 31 December 2011

Fully collateralised ..................... 125,702 46,532 38,381 1,761 60,794 4,891 278,061

Loan to Value (‘LTV’) ratio:

– less than 25% ....................... 9,898 5,364 2,383 58 3,576 282 21,561

– 25% to 50% ......................... 31,601 19,643 9,978 336 10,593 1,350 73,501

– 51% to 75% ......................... 52,656 17,748 18,006 895 25,138 2,221 116,664

– 76% to 90% ......................... 23,919 2,884 7,624 304 13,590 876 49,197

– 91% to 100% ....................... 7,628 893 390 168 7,897 162 17,138

Partially collateralised

– greater than 100% LTV ....... 3,275 484 295 174 12,503 102 16,833

– collateral value .................... 2,821 466 37 135 10,566 24 14,049

Total residential mortgages ......... 128,977 47,016 38,676 1,935 73,297 4,993 294,894

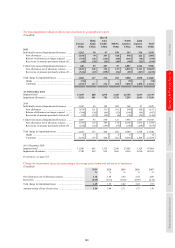

At 31 December 2010

Fully collateralised ..................... 115,700 43,948 34,674 1,490 66,542 5,086 267,440

LTV ratio:

– less than 25% ...................... 9,531 4,815 2,082 58 3,779 282 20,547

– 25% to 50% ......................... 27,740 15,984 8,733 235 10,973 1,272 64,937

– 51% to 75% ......................... 46,395 19,574 15,912 634 25,750 2,310 110,575

– 76% to 90% ......................... 23,044 2,569 7,661 409 16,091 1,003 50,777

– 91% to 100% ....................... 8,990 1,006 286 154 9,949 219 20,604

Partially collateralised

– greater than 100% LTV ....... 4,156 18 176 404 12,327 173 17,254

– collateral value .................... 3,705 15 45 152 10,539 88 14,544

Total residential mortgages ......... 119,856 43,966 34,850 1,894 78,869 5,259 284,694