HSBC 2011 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2011 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

|

|

19

Overview Operating & Financial Review Corporate Governance Financial Statements Shareholder Information

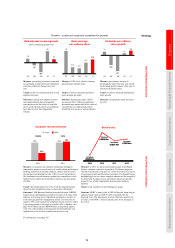

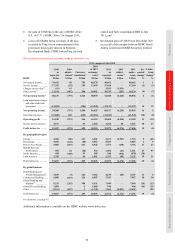

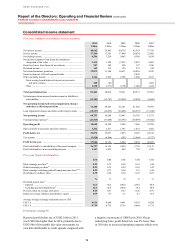

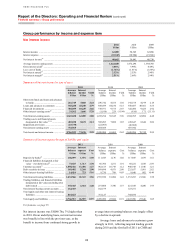

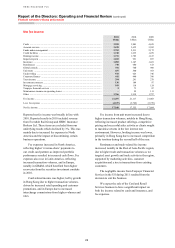

partly offset by lower loan impairment charges and other

credit risk provisions.

The results of the Group continued to be

adversely affected by the losses in the US consumer

finance business, which were US$2.4bn in 2011 and

US$2.2bn in 2010. We have agreed to sell the

profitable US Card and Retail Services portfolio,

with the remainder of the loss-making US consumer

finance business being run down. We expect the sale

of this business to have a significant impact on both

revenue and profitability in North America for the

foreseeable future.

The difference between reported and underlying

results is explained on page 16. Except where stated

otherwise, the commentaries in the Financial

Summary are on an underlying basis and references

to HSBC Finance Corporation (‘HSBC Finance’) and

HSBC Bank USA N.A. (‘HSBC Bank USA’) are on

a management basis, rather than a legal entity basis.

Net operating income before loan impairment

charges and other credit risk provisions (‘revenue’)

was broadly in line with 2010, due to the adverse

effect on GB&M revenue in Europe of the turmoil in

the eurozone sovereign debt market and a decline in

lending balances in RBWM in North America being

offset by revenue growth in faster-growing regions.

The eurozone turmoil resulted in lower trading

income from our Credit and Rates businesses as

problems escalated, particularly in the second half of

2011. Our GB&M performance was also affected by

lower revenues in Balance Sheet Management, as

higher yielding positions matured and interest rates

remained low, and in our legacy credit portfolio

(see page 23). In North America, we continued

to reposition our business and we remained focused

on managing down our run-off portfolios. As a

consequence, revenue fell, reflecting declining

customer loan balances in the run-off portfolios

and in the Card and Retail Services businesses.

These factors were broadly offset by increased

net interest income in CMB as a result of strong

balance sheet growth in 2010 which continued into

2011, albeit at a slower pace during the latter part of

the year. Revenue also benefited from balance sheet

growth in RBWM in Rest of Asia-Pacific and Latin

America. There were also strong performances in

over half of our business lines in GB&M, including

Global Banking, Foreign Exchange and Equities,

particularly in the faster growing regions of Rest of

Asia-Pacific and Latin America.

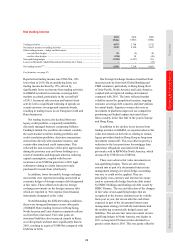

Loan impairment charges and other credit risk

provisions were considerably lower than in 2010,

with decreases across all regions except Latin

America and Hong Kong. The most significant

decline in loan impairment charges was in RBWM

in North America, reflecting lower balances in our

consumer finance portfolios and lower lending

balances and improved credit quality in Card and

Retail Services. There was also a notable decline in

loan impairment charges in Europe, due to successful

initiatives taken to mitigate risk within RBWM

which resulted in a reduction in delinquency rates in

personal lending in the UK. Loan impairment charges

and other credit risk provisions fell in the Middle

East in GB&M due to the non-recurrence of

restructuring activity for a small number of large

customers. In Latin America, loan impairment

charges and other credit risk provisions increased as a

result of strong lending growth in RBWM and CMB,

along with a rise in delinquency rates in Brazil during

the second half of 2011.

Operating expenses were higher than in 2010,

reflecting an increase in notable items and higher

staff costs in faster-growing regions. Notable items

included restructuring costs of US$1.1bn, a bank

levy introduced by the UK government of US$570m,

higher provisions relating to customer redress

programmes of US$898m and US mortgage

servicing costs of US$257m. The restructuring costs

were incurred as a result of actions taken following

the review of our capital deployment and operational

effectiveness. This led to a reduction of more than

7,600 FTEs during the second half of 2011 and

sustainable savings of US$0.9bn. These notable

items were partially offset by a credit of US$587m

resulting from a change in the inflation measure used

to calculate the defined benefit obligation of the

HSBC Bank plc (‘HSBC Bank’) UK defined benefit

plan for deferred pensions.

Income from associates increased, mainly driven

by strong results in our mainland China associates.

The contribution from Bank of Communications Co.,

Limited (‘BoCom’) rose due to loan growth, wider

deposit spreads and higher fee income. Our share of

profits from Industrial Bank Co. Limited (‘Industrial

Bank’) rose due to strong growth in customer lending

and an increase in fee-based revenue.

The reported profit after tax was US$3.8bn or

26% higher, due to the increase in taxable profits,

primarily from movements on the fair value of own

debt and a lower tax expense. This reflected the

inclusion in 2011 of a deferred tax benefit now

eligible to be recognised in respect of foreign tax

credits. In addition, the tax charge in 2010 included

US$1.2bn attributable to a taxable gain from an

internal reorganisation in North America. As a result

of these factors, the effective tax rate for 2011 was

18% compared with 25.5% in 2010.